Global| Aug 18 2016

Global| Aug 18 2016U.K. Retail No Post Brexit Breakdown...Yet

Summary

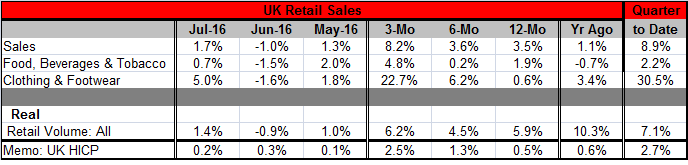

U.K. retail sales rebounded strongly in July after a 1% decline in June. Sales are up very strongly in three of the last four months. U.K. retail sales have been oscillating in this higher range since 2014. And they continue to grow [...]

U.K. retail sales rebounded strongly in July after a 1% decline in June. Sales are up very strongly in three of the last four months. U.K. retail sales have been oscillating in this higher range since 2014. And they continue to grow strongly in July as sales show some tendency to accelerate as well.

U.K. retail sales rebounded strongly in July after a 1% decline in June. Sales are up very strongly in three of the last four months. U.K. retail sales have been oscillating in this higher range since 2014. And they continue to grow strongly in July as sales show some tendency to accelerate as well.

Nominal retail sales show acceleration with three-month sales up at an 8.2% annualized pace and year-over-year sales up at a 3.5% pace. Real Sales volumes are up at a 6.2% annual rate over three months with 12-month sales up at a 5.9% pace. Sales volume growth is relatively strong and steady with a pace near 6% over three months, six months and 12 months.

In the quarter to date, nominal sales are flying at an 8.9% pace while real sales are up at a solid/strong 7.1% pace. These calculations are obviously fragile this early in the quarter. They serve to highlight how things are starting out in the new quarter, but with two more months to average in to the performance, there should be little doubt that the final growth rates will differ from these early numbers.

However, retail sales are not the only word on the subject of retail performance.

Early in the month, retail sales survey from the CBI (reproduced the chart above) showed a much less upbeat view on expectations for retail sales. Of course, actual retail sales trump a survey of what retail sales are expected to be. But the CBI survey shows that the volume growth of sales and orders is slipping and has been slipping in this survey for several months. Both retail sales and the CBI survey are up-to-date through July, so there is no difference in the tenor of the data. The CBI result suggests that we should be open-minded about the future and for the potential that adverse Brexit effects could show their hand. The tandem weakness in net orders and net sales is a dual signal that is probably worth not dismissing despite the current apparent ebullience of the U.K. consumer. Brexit will still have its day of reckoning.

Early in the month, retail sales survey from the CBI (reproduced the chart above) showed a much less upbeat view on expectations for retail sales. Of course, actual retail sales trump a survey of what retail sales are expected to be. But the CBI survey shows that the volume growth of sales and orders is slipping and has been slipping in this survey for several months. Both retail sales and the CBI survey are up-to-date through July, so there is no difference in the tenor of the data. The CBI result suggests that we should be open-minded about the future and for the potential that adverse Brexit effects could show their hand. The tandem weakness in net orders and net sales is a dual signal that is probably worth not dismissing despite the current apparent ebullience of the U.K. consumer. Brexit will still have its day of reckoning.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief