Global| Jul 25 2003

Global| Jul 25 2003U.K. Q1 GDP Lower than Expected

Summary

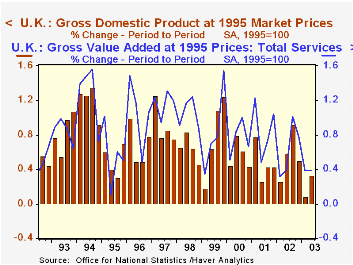

After Thursdays report of strong retail sales in the UK for June, tepid growth in second quarter GDP was disappointing. The Preliminary estimate showed only a 0.3% increase from the first quarter (1.8% from a year ago). The early GDP [...]

After Thursday’s report of strong retail sales in the UK for June, tepid growth in second quarter GDP was disappointing. The Preliminary estimate showed only a 0.3% increase from the first quarter (1.8% from a year ago).

The early GDP tabulation represents estimates of industrial value added. It indicates that oil, gas and other mineral extraction declined, and manufacturing production was probably flat. Service sector output gained about 0.4% on the quarter. Thus, while retail sales suggest that consumer demand improved, other segments of the UK economy were sluggish.

| UK: Constant GDP (1995=100) | Q2 2003 Q1 20032002 | 2001 | 2000 | ||||

|---|---|---|---|---|---|---|---|

| Q/Q%Chg | Y/Y%Chg | Q/Q%Chg | Y/Y%Chg | ||||

| Total | 0.3 | 1.8 | 0.1 | 2.1 | 1.9 | 2.1 | 3.1 |

| Service Industries | 0.4 | 2.6 | 0.4 | 2.6 | 2.6 | 3.5 | 3.6 |

by Carol Stone July 25, 2003

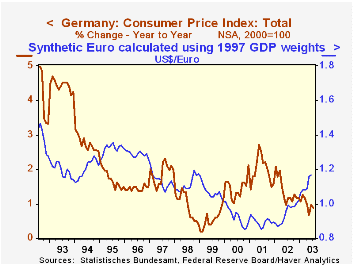

German consumer prices are drifting ever so slightly lower, according to the preliminary July CPI data for the six “Laender” (states). Their individual states’ price indexes rose 0.2% to 0.3% each, averaged by the Federal Statistics Office to 0.2%, which yields a 0.1% decline after seasonal adjustment. This monthly performance produced year-on-year inflation in July at just under 1% for a fourth consecutive month. Details on the sources of the moderation in July will not be reported until the final data are issued in mid-August. But a quick glance at the trend in the euro suggests that its recent strength has been a factor in the current slow pace of inflation in Germany.

| German CPI | July 2003, NSA | July 2003, SA | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| 2000=100 | 0.19% | -0.10% | 0.87% | 1.37% | 1.97% | 1.47% |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief