Global| Apr 10 2019

Global| Apr 10 2019U.K. IP Shows Mixed Trends

Summary

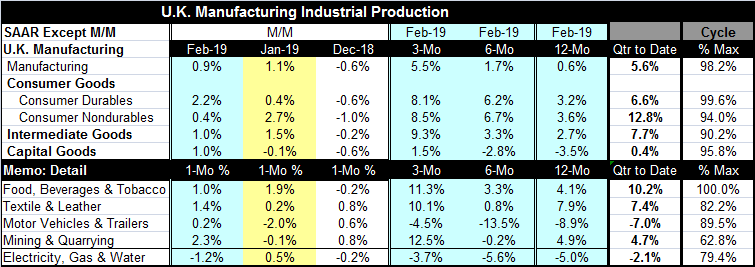

U.K. manufacturing industrial output rose in February by 0.9%, marking back-to-back increases averaging 1% per month for two months in a row. Headline manufacturing growth shows acceleration in progress from 12-months (0.6%) to six- [...]

U.K. manufacturing industrial output rose in February by 0.9%, marking back-to-back increases averaging 1% per month for two months in a row. Headline manufacturing growth shows acceleration in progress from 12-months (0.6%) to six-months (1.7%) to three-months (5.5%).

U.K. manufacturing industrial output rose in February by 0.9%, marking back-to-back increases averaging 1% per month for two months in a row. Headline manufacturing growth shows acceleration in progress from 12-months (0.6%) to six-months (1.7%) to three-months (5.5%).

This is a robust pick up in the output trends of one year and less for IP expansion. But the year-on-year trend has showed declines in seven of the eight previous months. With the February report, the year-on-year change is positive at 0.6%; it is also modest. The question here is whether the year-on-year trends turn and whether the under-one-year trends are authentic trends that can last and reverse nearly three quarters of a year of declining output. Consumer durable goods, nondurable goods, intermediate goods and capital goods all show accelerating trends in IP for one year and under.

The graph plots year-on-year rates of growth; it shows trends slipping for capital goods and for consumer durables, but there is some stabilization for consumer nondurables. Since nondurables are the less cyclical than durables, the stability in nondurables is a hopeful sign for a more even-keeling future.

Another encouraging sign is that with two months into the first quarter, the quarter-to-date growth rates for all of these sectors are positive and all show substantial strength except capital goods.

That brings to the big question about the United Kingdom. GDP is estimated to have risen by 0.5% in January and slowed to a 0.2% gain in February by the Office for National Statistics. And as growth slows down, industrial output is showing signs of speeding up. The problem, of course, is Brexit. And the weakness in capital goods output is one of the real red flags since firms do not generally want to invest until they know the lay of the land in the future. And with Brexit and concerns about what kind of severance there will be – a Brexit with a deal or a Brexit with no deal- keeps investments on the sidelines. Weakness in capital goods output is the poster-child for that problem.

There is future uncertainty about what current trends may mean since Brexit uncertainty has also spurred some activity as some firms have stockpiled goods, owing to uncertainty of access to them in the post-Brexit environment. Ironically, Brexit is retarding investment and then selectively boosting or hurting other underlying industries depending on how they see the future and what actions they have decided to take to protect their own interests.

With Brexit undecided, the U.K. economy is simply too difficult to analyze. In the IMF outlook released yesterday, there was considerable space devoted to Brexit and its uncertainty and what the aftermath of the U.K. leaving the EU might do to growth under several different assumptions (here, download pdf file and see page 28, "Scenario Box 1.1. A No-Deal Brexit"). Needless to say, the IMF remains concerned.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief