Global| Jan 12 2016

Global| Jan 12 2016U.K. IP Contracts in November, Marking an Extended Period of Weakness

Summary

U.K. manufacturing industrial production fell by 0.4% in November, falling for the second straight month. Manufacturing output is falling by 1.3% over 12 months and falling by 0.4% over six months. Over three months, output is still [...]

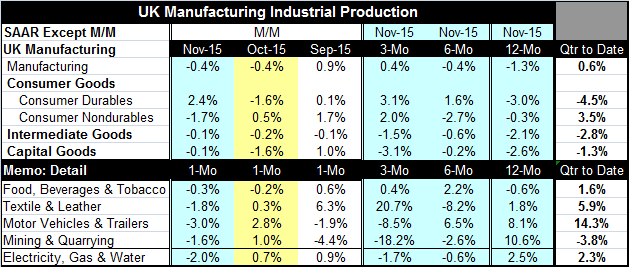

U.K. manufacturing industrial production fell by 0.4% in November, falling for the second straight month. Manufacturing output is falling by 1.3% over 12 months and falling by 0.4% over six months. Over three months, output is still expanding at a 0.4% annualized rate.

U.K. manufacturing industrial production fell by 0.4% in November, falling for the second straight month. Manufacturing output is falling by 1.3% over 12 months and falling by 0.4% over six months. Over three months, output is still expanding at a 0.4% annualized rate.

In November, output fell for consumer nondurables, intermediate goods, and capital goods. Consumer durable goods output continued strong in November, rising by 2.4% month-to-month.

Sequential growth rates from 12-month to six-month to three-month show that consumer durable goods output is accelerating, the only sector to do so. Consumer nondurable goods output is rising over three months, but that is after contracting sharply over six months. Intermediate goods output is declining on all horizons as is capital goods output.

Industry results show declines in output for all the industries listed in the table. Mining and quarrying is showing an ongoing sharp and accelerating contraction. BP just announced today that it is going to be shedding even more workers as the global energy glut continues to take a toll on sector investment and operations. Sequential growth rates for other sectors continue to show a great deal of weakens albeit food and drink continue to expand in recent sequential periods.

In the quarter-to-date, with one month's data left to post, manufacturing output is rising at a 0.6% annualized rate. Output is falling in all sectors, except consumer nondurables output, which is boosting headline growth all on its own. Industry detail shows gains in all the listed industries in the quarter-to-date except for mining and quarrying.

The year-over-year drop in manufacturing output is the largest for manufacturing output in the U.K. since July 2013. Output now has four months of year-over-year declines in a row and a stretch of six months without an increase in manufacturing output. Output last fell for four months in a row in February-May of 2013. At that time, the declines were even stronger than they are now and the string of declines had gone on for much longer. Nonetheless, this episode is a significant weak patch for the U.K. manufacturing sector. It is coming at a time of weak global demand and ongoing downward pressure on extractive industries. Manufacturing worldwide is under pressure from excess capacity and weak demand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief