Global| Aug 18 2015

Global| Aug 18 2015U.K. Inflation Perks Up

Summary

U.K. inflation has begun to show some pressure. The long-term chart of U.K. inflation trends still looks tranquil. The monthly gains on the HICP and the RPI (and RPIx) all are at a modest 0.2%. However, the progression of inflation [...]

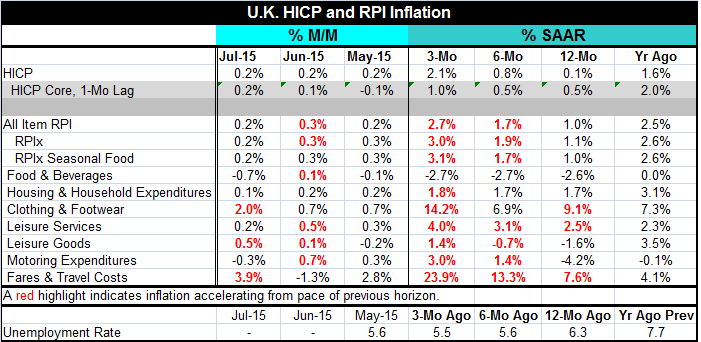

U.K. inflation has begun to show some pressure. The long-term chart of U.K. inflation trends still looks tranquil. The monthly gains on the HICP and the RPI (and RPIx) all are at a modest 0.2%. However, the progression of inflation over 12 months, six months and three months is building a head of steam. HICP inflation has progressed from 0.1% to 0.8% to 2.1%. On that same sequence of horizons, the RPI has progressed steadily from 1% to 1.7% to 2.7%, an ominous progression to a clearly unacceptable three-month pace. The Bank of England shoots for 2% inflation. Is rising inflation really a threat?

U.K. inflation has begun to show some pressure. The long-term chart of U.K. inflation trends still looks tranquil. The monthly gains on the HICP and the RPI (and RPIx) all are at a modest 0.2%. However, the progression of inflation over 12 months, six months and three months is building a head of steam. HICP inflation has progressed from 0.1% to 0.8% to 2.1%. On that same sequence of horizons, the RPI has progressed steadily from 1% to 1.7% to 2.7%, an ominous progression to a clearly unacceptable three-month pace. The Bank of England shoots for 2% inflation. Is rising inflation really a threat?

Of course, central banks tend to stress year-over-year inflation. Three-month inflation rates can go up and down and are unreliable as gauges of where inflation is. On the year-over-year gauge, inflation is still quite low. The HICP is at 0.1% and the RPI is at 1%. From 2009 - 2010, the BOE missed its inflation target as inflation soared and ran at a 4% pace for a while. More recently inflation has been undershooting. What is a central bank to do?

In the table, the RPI is accelerating in six of seven components. Inflation seems to have found some purchase. However, the pace of inflation is not a touchstone level yet. Annual inflation is far from raising any eyebrows except the most hawkish of the hawks. And the BOE expects inflation to return to target (2%) in two years. That surely gives policy plenty of time to react - if it is right.

Moreover, the British government is still phasing in further austerity and that is likely to keep inflation from picking up at a worrisome pace. The U.K., of course, lives in the same global environment with everyone else and global growth and prices remain weak. The pound sterling has been firm and rising, providing another barrier to inflation and another reason not to worry about inflation. The U.K. still finds that inflation faces headwinds.

The Federal Reserve in the U.S. and the Bank of England in the U.K. are the only two major central banks grappling with the timing of a rate hike. The weakness of the environment likely raises the hurdle for a rate hike to be executed in each of those countries. Elsewhere, the European Central Bank is staying its course of ease. Recent GDP weakness may put the Bank of Japan back on a more aggressive easing course. The Fed is said to be on track for a September rate hike, but U.S. inflation, like U.K. inflation, remains far too low to be a justification for a rate hike.

Globally, policy continues to be characterized by fiscal tightness and monetary ease in Western countries. In Asia, China has pulled out the stops on both fiscal and monetary policy with no effect. So it has turned to currency debauchery. Japan has lost control of fiscal policy due to past excesses. Its monetary policy is the most stimulative of all, still getting little traction.

Of course, the U.K. will be affected too by the success of the ECB and the success of Europe in dealing with Greece. The U.K. trades a great deal with Europe, but for now the most pressing issue for the U.K. will be the development of domestic growth in the face of new rounds of fiscal austerity. The downside of a firming currency is that it also stifles domestic growth unless domestic inflation falls to offset the currency's rise. Despite appearances this month, the U.K. would seem to have inflation more in a bottle than it has growth on the right track.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief