Global| Oct 21 2020

Global| Oct 21 2020U.K. Inflation Fluctuates in a Low Band

Summary

Sequential U.K. inflation (from 12-months to six-months to three-months) has no clear trends, but its profile remains in a low band of outcomes ranging between a pace of 1% and 0.1%. Core inflation (also excluding tobacco and alcohol) [...]

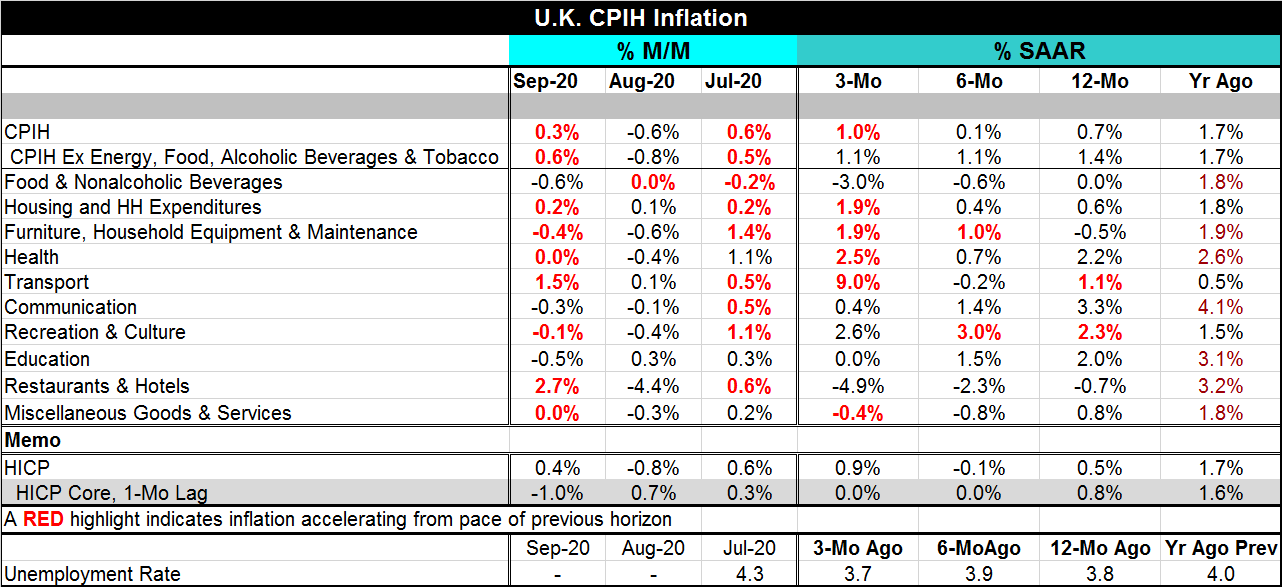

Sequential U.K. inflation (from 12-months to six-months to three-months) has no clear trends, but its profile remains in a low band of outcomes ranging between a pace of 1% and 0.1%. Core inflation (also excluding tobacco and alcohol) ranges from 1.1% to 1.4%, a higher profile but still a low band of outcomes.

Sequential U.K. inflation (from 12-months to six-months to three-months) has no clear trends, but its profile remains in a low band of outcomes ranging between a pace of 1% and 0.1%. Core inflation (also excluding tobacco and alcohol) ranges from 1.1% to 1.4%, a higher profile but still a low band of outcomes.

Inflation is still mostly tame and low

However, of the 10 CPIH categories, seven of them show inflation acceleration on a month-to-month basis. But that follows a month with only one monthly acceleration and a sharp drop in the headline and pace; both of which logged negative outcomes (in fact, six components logged negative results for August and one other was flat on the month). All in all, it is not surprising that, over three months inflation is rising in only 5 of 10 categories compared to its pace over six months. Over six months inflation rises compared to its pace over 12 months in only of 2 of 10 categories. Over 12 months inflation rises compared to inflation of 12-months ago in only two categories. These multi-month time segments only show any hint at acceleration from six-months to three-months and that cannot be very surprising since the headline pace over six months was an annual rate gain of only 0.1%. Over three months the ‘acceleration' is only in half of the pricing components and it only takes the pace of headline inflation up to an annualized 1% and that after rising by just 0.1% over six months. It is hard to paint any of this as a serious inflation picture.

Also modest using the EU method of measurement

U.K. inflation has been low stable and in a narrow range. The HICP measure that is compiled on the same definition used to assess inflation in EMU member countries is also low with a sequential band that ranges from -0.1% to 0.9%. On a lagged relationship, the HICP core is in range of 0% to 0.8%, below the core pace for the CPIH (a definition which also excludes alcohol and tobacco).

Some clear eco-slowing

British unemployment whose tally lags that of inflation is up-to-date only through July. Its measure has risen to 4.3%, its highest mark since November 2017 (it was last higher in May 2017).

Trouble brewing?

Bank of England Deputy Governor Dave Ramsden says that pushing British rates below zero would be the wrong thing to do now (Citation here). However, the U.K. economy remains in a tight spot with uneven growth, still very low unemployment, and low inflation, but with Brexit negotiations apparently stuck in a loop of disagreements and a virus outbreak of growing intensity. It's a lot to balance.

The Covid-19 risk grows

The U.K. infection rate began to escalate in August. By late-September, the daily outbreaks exceeded the peaks of April. In early-October, that hit a peak infection pace of 22,961 that briefly receded, but as of October 20 was back up to 21,330. This is a significant risk to the economy since the U.K., despite the outcome, is trying to avoid the spread and has not adopted a Sweden-style hunt for herd immunity. Hospital admissions are up to 6,431 as of October 20 and the number on ventilators is rising as well (Source here).

Covid-19 policies are applying the brake

A number of Covid-19 alerts of various degrees of severity are already in place for localities as this recent wave is being fought off. This tactic is also adversely impacting growth. The impact on inflation is uneven as economic weakness generally reduces price pressures, but Covid-19 also tends to put price pressures on certain items that go into short supply. The U.K. is clearly in the middle of a severe Coivd-19 event and at the same time there are significant issues being negotiated for its end game with the EU on Brexit and some real conflicts persist in those negotiations. Boris Johnson and the U.K. seem to have too many balls in the air to think that they can continue to juggle them effectively without dropping any.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief