Global| Sep 22 2015

Global| Sep 22 2015U.K. Industry Weakens in September

Summary

The U.K. industrial sector is showing signs of a slowdown. U.K. industry total orders fell to -7 in September from -1 in August. The reading is substantially weaker than its 12-month average which is also -1. In the historic sweep of [...]

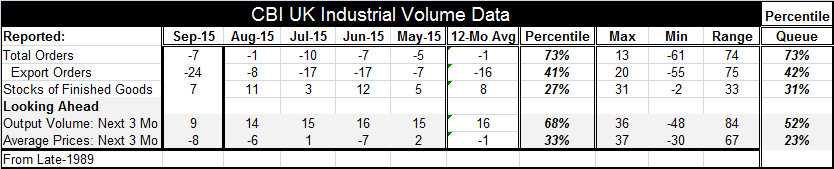

The U.K. industrial sector is showing signs of a slowdown. U.K. industry total orders fell to -7 in September from -1 in August. The reading is substantially weaker than its 12-month average which is also -1. In the historic sweep of data, the -7 reading still is not weak. It sits in the 73rd percentile (top 27%) of its historic queue of data taken back over 21 years. Still, it is clear that over the past four months or so the industrial reading has slipped substantially from what it had been in 2013 and 2014. The level of orders is not as vexing as the new pattern of momentum.

The U.K. industrial sector is showing signs of a slowdown. U.K. industry total orders fell to -7 in September from -1 in August. The reading is substantially weaker than its 12-month average which is also -1. In the historic sweep of data, the -7 reading still is not weak. It sits in the 73rd percentile (top 27%) of its historic queue of data taken back over 21 years. Still, it is clear that over the past four months or so the industrial reading has slipped substantially from what it had been in 2013 and 2014. The level of orders is not as vexing as the new pattern of momentum.

Export orders have similarly weakened and they sit much lower at the 42nd percentile of their historic queue. They are below their median and well below their 12-month average, which stands at -16.

Stocks of finished goods are relatively lean at 7 in September, down from 11 in August. They stand in the 31st percentile of their historic queue; this is a bottom one-third standing. Inventories do not appear to have any excess nor does an inventory cycle seem in gear or likely.

Expected output volume over the next three months sagged to 9 from 14. It stands below its 12-month average of 16. It is positioned in the 52nd percentile of its historic queue of data, leaving it barely above its historic median value (which occurs at a rank at the 50th percentile).

Despite the fact that central banks are trying to reflate, the Bank of England has had an accommodative policy in place for a very long time. Expectations for prices over the next three months have slipped to a reading of -8 in September from -6 in August. The reading sits below its 12-month average of -1 and stands in the 23rd percentile of its historic queue, a weak reading. Inflation expectations are falling.

The U.K. industrial sector seems to be losing momentum. All the key components of this survey are substantially weaker than their respective 12-month averages and declining month-to-month. The absolute percentile standings of the industrial survey measures are far from firm except for orders. And momentum clearly is pointing lower across the board.

Perhaps the weakness in Europe is catching up to the U.K. That could explain the difference in the percentile standing of total orders vs. export orders. Today the ADB cut its outlook for growth in Asia largely because of weaker performance expected from China. Global weakness continues to be an important and difficult phenomenon. Increasingly, monetary policy looks like the wrong tool to fight it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.