Global| Nov 20 2018

Global| Nov 20 2018U.K. Industrial Trends Rebound in November But Remain Soft

Summary

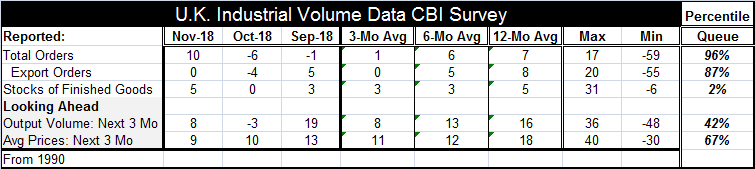

The U.K. industrial survey from the Confederation of British Industry (CBI) showed total orders rebound to log a gain at a reading of 10 in November after a negative balance of responses at -6 in October. Export orders ‘turned around’ [...]

The U.K. industrial survey from the Confederation of British Industry (CBI) showed total orders rebound to log a gain at a reading of 10 in November after a negative balance of responses at -6 in October. Export orders ‘turned around’ to post a flat November reading after an October response of -4.

The U.K. industrial survey from the Confederation of British Industry (CBI) showed total orders rebound to log a gain at a reading of 10 in November after a negative balance of responses at -6 in October. Export orders ‘turned around’ to post a flat November reading after an October response of -4.

Looking ahead, output volume expectations rose to 8 in November from -3 in October, while average price expectations softened to 9 from 10.

The survey showed rebounds and resilience across the board. But the values struck are still part of a declining profile.

Separately, the German finance minister, Olaf Scholz, was making his annual pilgrimage to give good advice to those with less will-power than himself. Today he urged Italy to get control over its debt problem. That’s a little like telling a patient in intensive care to heal himself. Italy has been under the yoke of austerity and its economy under this German-inspired plan has not been able to return the Italian economy to its prerecession/financial crisis level of GDP of one decade ago. I would think after all this focus on stopping spending and slowing debt and trying to make Italy ‘Germany’ the better plan for Italy would be to grow. But no one in the EMU has reached that conclusion yet, except the Italians.

Mr. Scholz has also said that of all the things he worries about, from Italian debt and its euro-intransigence to Donald Trump’s trade wars, it is Brexit that worried him the most. One can view Italy’s stance as an outcropping of the U.K. EU defiance and ultimately its choice to leave. Catalonia in Spain has undoubtedly been emboldened to seek independence. It is well known that the people of the EU and EMU have a lot of concerns about how the region has operated and some of the policies that have been adopted although most polls show that the euro-population wants to stay rather than leave despite their misgivings. Of course polls of the U.K. referendum told us that the people would vote to stay- and they didn’t. Polls should give politicians precious little comfort these days.

In addition, Spain is now making noises to the effect that the current language over Gibraltar is unacceptable to it and that unless that language is changed it will not be voting to approve the U.K. Brexit plan as it stands.

France and Germany have made it clear that in the post Brexit world trade without friction would be pure science fiction. The U.K. will pay a price in trade accessibility for leaving. Why this is so unclear since these countries have had close trading relationships for an extremely long time. But what seems likely is that this deal is a communication to Italy and anyone else that might seek to leave that once you leave the EU your special relationships of the past counts for naught.

Turning back to the CBI survey, it is clear that the trend readings are showing decay despite the one month rebound. The table features 12-month, six-month and three-month averages in addition to presenting the queue standings for the current observation to assist in understanding what this report is telling us. The queue standing tells us that this month’s total order reading is rarely stronger with a 96th percentile standing. However, the sequential averages for orders show weakening from 12-months to six-months to three-months. November created a 16-point switch. This month-to-month change is the third greatest monthly swing in this reading since January 1998, marking it as an event this strong or stronger that happens only 0.2% of the time - quite rarely. It is not a good idea to build an outlook on this swing. In fact, monthly swings on the order of +10 points or more are overwhelmingly followed by a substantially weaker reading, often a negative one.

For this reason, I place much more emphasis on the declining sequential averages. The moving averages in contrast tend to move in large cycles and they are now coming off a rebound and signaling a slower future. Sequential export orders also show sequential erosion as do expected output volume and expected prices.

Total and export orders still brandish strong queue standings on their November levels. But expected output volume is below its median with a queue standing at its 42nd percentile. Expected prices show sequential easing but still have a queue standing at their 67th percentile.

In the game of Thrones, winter is coming. In the U.K., Brexit is coming. Everybody fears something. The German financial minster fears Brexit more than anything else probably not for the bilateral U.K.-EU impact but for the repercussions it could have on the rest of the euro area especially as parties sit down for their final meeting. All the analysis has said that the EU holds all the cards. But the British have the strongest military force in Europe at a time that the U.S. has been pressuring Europe to pick up its own end of the bargain. Europeans have talked about a European army, but good luck with that when Germany, a nation of engineers, can’t even get its motor pool vehicles to start. And by what future date could Europe assemble a viable force? Right now Europe has its deepest disagreements with the U.K. and the U.S., the two countries that most protect it from a continental incursion. Is Theresa May waiting to pull the defense card out at the last minute or not? The U.K. is not without a card to play, but the one it has to play would put it all-in.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief