Global| May 22 2018

Global| May 22 2018U.K. Industrial Survey Backs Down But Still Shows Firm Responses

Summary

U.K. orders backed off from their recent high levels but continue to offer up a relatively strong outlook. The rest of the survey remains substantially upbeat from a business standpoint. The Confederation of British Industry (CBI) [...]

U.K. orders backed off from their recent high levels but continue to offer up a relatively strong outlook. The rest of the survey remains substantially upbeat from a business standpoint.

U.K. orders backed off from their recent high levels but continue to offer up a relatively strong outlook. The rest of the survey remains substantially upbeat from a business standpoint.

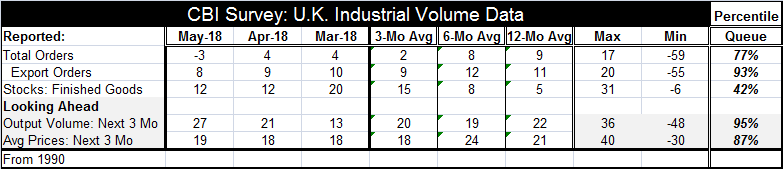

The Confederation of British Industry (CBI) Industrial survey found a -3 diffusion response on new orders for May, a weaker result than April’s +4 reading. In May there is a small net balance of respondents looking for orders to recede. The May reading of -3 compares to a three-month average of +2 and a six-month average of +8. However, the clear trend in order responses has been to lower figures judging from the sequential average values from 12-months and in. The May order reading, nonetheless, is relatively solid with a queue standing in the 77th percentile of all responses since 1990.

Export orders follow the same general pattern of overall orders but with readings corresponding much higher standings and only the hint of weakness shown in total orders. Export orders inched down to a reading of +8 in May from +9 in April. Its sequential average shows only a very mild backing off from its recent high readings. Its current +8 reading has been higher since 1990 only about 7% of the time, marking this as a very strong monthly result. Export orders remain a bright spot in the profile for U.K. industrial firms, despite decay in orders overall.

Inventory responses are more circumspect with a current reading for May unchanged at April’s mark but substantially below its reading for March, the inventory response has retrenched and stabilized. The 42nd percentile standing for inventories (below its historic median) given its recent declines suggests that some sort of inventory cycle has been run and that stocks may now be in better balance with sales. This is more likely now with such a buoyant outlook.

Unlike orders, the outlook for three months ahead is quite upbeat and improving. The reading for May jumped to +27 from +21 in April and +13 in March. The outlook has been improving steadily and sharply. The readings for 12-months, six-months and three-months show consistently strong results. The queue standing for the outlook is in the top five percentile of all such readings since 1990. U.K. firms remain quite upbeat on the outlook despite the order decay.

As for prices, the outlook for the next three months remains very steady and has ticked higher in May. The three-month average for the outlook is below the six-month and 12-month readings, but the slippage, while noticeable, is relatively small and does not appear to be ongoing. However, recall that there is ‘companion weakness’ in total orders on this timeline. At its current level, the outlook for average prices has an 87th percentile standing. Since the Bank of England has been fighting excessive inflation based mostly on higher import prices, the still-high reading for prices suggests that the BOE may still have more work to do. But the steady readings over the last three months also suggest that the situation is not worsening.

Summing up

On balance, the U.K. industrial sector appears to be still strong. It is clearly advancing and while there is evidence of weaker orders the continued strength in foreign orders is reassuring. The stability in inventory readings also is a mark of reasonable business confidence. The look remains extremely positive and it has logged its strongest reading in seven months. The price expectation readings are reassuring from the standpoint of business opportunities and yet a bit ‘hot’ from the standpoint of what the BOE is trying to achieve. Overall there is very little evidence of any significant slowing, business confidence seems to be quite good, judging from their expectations for sales volumes, while the price environment seems a bit hot.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief