Global| Jan 22 2020

Global| Jan 22 2020U.K. Industrial Optimism Makes a U-Turn for the Better

Summary

It is as though the CBI conducted its survey in Q4 and in Q1 in two different countries. The R-square linking the percentile standings in Q1 2020 to Q4 2019 has a value of 0.026, indicating that one quarter can explain about 2.5 [...]

It is as though the CBI conducted its survey in Q4 and in Q1 in two different countries. The R-square linking the percentile standings in Q1 2020 to Q4 2019 has a value of 0.026, indicating that one quarter can explain about 2.5 percentage points of rank standing in the next quarter- a miniscule correlation. In fact, on data back to 1984, these two adjacent quarters have the lowest correlations between any two adjacent quarterly correlations in the last 36 years! That, of course, includes all the unraveling that occurred during the financial crisis and in the great recession as well.

It is as though the CBI conducted its survey in Q4 and in Q1 in two different countries. The R-square linking the percentile standings in Q1 2020 to Q4 2019 has a value of 0.026, indicating that one quarter can explain about 2.5 percentage points of rank standing in the next quarter- a miniscule correlation. In fact, on data back to 1984, these two adjacent quarters have the lowest correlations between any two adjacent quarterly correlations in the last 36 years! That, of course, includes all the unraveling that occurred during the financial crisis and in the great recession as well.

Politics matter!

To U.K., businesses having a common front and method to approach Brexit- even though they do not know exactly what that will mean has had a massive impact on the way business looks at business prospects. Business optimism logged its last (previous) positive value Q1 2018 at +13. It deteriorated to -4 and -3 in Q2 and Q3 of 2018 then dropped to -15 in Q4 2018. From there on, the readings fell quarterly to -23. -13, -32, and finally to -44 in Q4 2019. These readings and this progression compare to a -5 reading in Q2 2016 ahead of the Brexit referendum that 'no one' thought would be accepted. It was followed by a shocked net optimism reading of -47 in the wake of the unexpected vote. But that weak Q3 reading of -47 quickly improved to -8 and moved up to +15 by Q4 2016 and Q1 2017, respectively. In contrast, the deterioration in 2019 was a reaction less to the reality of Brexit and much more to the inability to form a common ground to deal with it. The election of Boris Johnson and demise of the Labor party and of Brexit opposition has changed all that. This is a powerful set of facts about how much the political environment matters to economics.

What the survey says

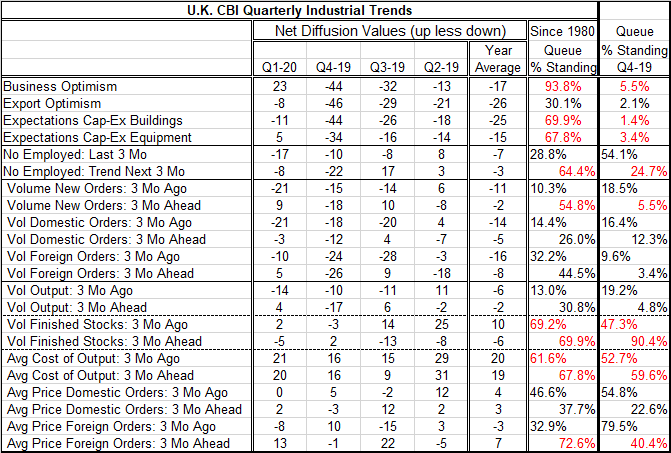

In Q1 2020 business optimism is strong, rising to +23 from -44 in Q4 2019, with a rank standing at its 93.8 percentile; this reading is this high or higher less than 7% of the time over the last 36 years. Not only is this a big change in optimism, it is a strong level of optimism. Export optimism is less negative but still has a low standing at its 30th rank percentile. Business is worried about its ability to export under the new and as yet unformulated Brexit situation. Expectations for investment in buildings and equipment both swing sharply higher in the quarter to a roughly a two-thirds standing in their respective quarterly rankings.

Employment

The swing higher in optimism is more impressive as it comes during a period when hiring has slowed. The assessment of the number employed fell to -17 in Q1 2020 from -10 in Q4 2019 while expectations for hiring rose to -8 in Q1 from -22 in Q4. Expectations are dominating actual past trend results- that is powerful.

Orders

Next there are a series of entries concerning overall orders, domestic orders and foreign orders comparing the trend over the last three months to expected trend in the next three months. Except for foreign orders, all the three-month ago trends worsened from Q4 to Q1. However, expected orders over the next three months broke ranks with those changes and are substantially higher in Q1 compared to Q4. In Q4 the three-month trends have higher percentile standings than the three-month ahead expected trends, but in Q1 2020 that flips and the three-month expected trends for the three orders series all are stronger for the expectations than for the past trends. Again these are surprising and powerful results. But even with these 'powerful results' Brexit is hardly being lauded as a success for business. Both domestic and foreign new orders still have standings that linger below their historic medians. Many readings are not even firm. For total orders, there is a slight premium to its historic median (a rank standing above 50% indicates a premium to the median) at a modest 54.8% ranking in this case. It is hard to square that with a business optimism standing in its 93rd percentile.

Output

The volume of output showed a weaker three-month trend in Q1 2020 but a much stronger expected trend in Q1 2020. Still, the expected trend for output has a low standing in its 30.8 percentile – hardly robust. In fact, the low standings for the components responses apart from the top four categories in the table are for the most part poor and make those strong headline readings a bit hard to fathom.

Inventories

The responses on stock-holding (inventory levels) are not particularly illuminating. In Q4, expected stock holding was exceptional because of the uncertainty of Brexit.

Costs and prices

The last six entries concern costs and prices, some domestic, some foreign and for the three months past as well as the three months ahead. The three-month trend in prices fell from Q4 to Q1 although costs rose on that comparison. Looking ahead, costs and prices are expected to be higher as the U.K. has traded a lot with Europe and under Brexit businesses expect to lose some tariff privileges and for costs to rise, at least initially.

The changes

Overall there are 22 survey line items with only six of them worsening in Q1 compared to Q4. Apart from the factors in the table, there is a survey that explores factors that might limit output in the three months ahead to limit export orders or Cap-Ex. The boxes that businesses tick the most among 'factors that could limit output' are for skilled labor then for other labor. There are some concerns also about the availability of materials. Factors likely to limit export orders flag 'political or economic conditions abroad' the most followed by 'delivery dates' as Brexit will lengthen delivery lags. The next highest standing concern is 'quota or export license restrictions.' As to Cap-Ex plans, the highest ranking concerns are once again the shortage of labor followed by some concerns over financing.

On balance

I suspect that the high reading on business optimism this quarter is overstated but represents a sigh of relief over the concerns businesses were harboring. The responses to the various line items in the survey do not seem to justify such a strong headline and I expect it to pull back are firms begin to focus more on their business prospects ahead rather than on their worst nightmares avoided.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief