Global| Jan 27 2015

Global| Jan 27 2015U.K. GDP Slows in Q4 but Finishes a Strong Year

Summary

U.K. GDP slowed in Q4 2014, rising by 0.5% after having gained 0.7% in the previous quarter. The U.K. office for National Statistics reports gains of 0.8% in services and of 1.3% in agriculture, against a slippage of 1.8% in [...]

U.K. GDP slowed in Q4 2014, rising by 0.5% after having gained 0.7% in the previous quarter. The U.K. office for National Statistics reports gains of 0.8% in services and of 1.3% in agriculture, against a slippage of 1.8% in construction and of 0.1% in production. Services, the largest of these four GDP sectors, continue to be the driver of growth while production has become a small detractor.

U.K. GDP slowed in Q4 2014, rising by 0.5% after having gained 0.7% in the previous quarter. The U.K. office for National Statistics reports gains of 0.8% in services and of 1.3% in agriculture, against a slippage of 1.8% in construction and of 0.1% in production. Services, the largest of these four GDP sectors, continue to be the driver of growth while production has become a small detractor.

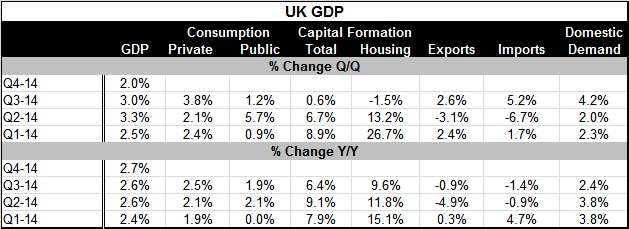

Year over year GDP is higher by 2.7% vs. the same quarter of one year ago; this marks a small acceleration over Q3 when its four-quarter gain stood at 2.6%. GDP for the year as a whole rose by 2.6%. Assessed against its prerecession peak of 2008, Q1 GDP is 3.4% higher. The 2.6% full-year pace is the highest since 2007.

The U.K. is the earliest reporter among G-10 countries of GDP growth. We plot its result vs. the data up to Q3 for the U.S. and Germany, two well-known strong economies. The U.K. has been consistently splitting the difference, with growth faster than Germany but trailing the U.S. pace since 2011. The U.K. growth profile has a steady gradient, too. Germany has been struggling recently.

Leading up to Q4 U.K. growth trends had favored the private sector. Capital formation and housing have been two of the leading growth components in GDP. But four quarter growth trends show that both exports and imports have begun to sputter. Quarter-to-quarter export and import flows show some tendency to recovery, but the Q2 dip is still not surmounted in their four-quarter rates of growth. However, U.K. domestic demand whether measured by quarterly or by four-quarter growth rates continues to be quite solid through Q3.

The U.K. is not befitting from its proximity to the EMU's single currency arrangement where growth continues to struggle and Germany which grows well does so by feeding off its export sector. The problems in Europe are well known especially the dropping exchange rate which is making EMU members more voracious competitors for international trade.

The U.K. of course sits astride the oil shock with an oil sector that is being adversely affected by dropping output price developments and a consumer sector that will welcome lower energy prices.

The slightly slower growth in Q4 is matter of some controversy. Economists are not sure if it is a sign of weaker growth ahead or just part of the quarterly volatility of GDP. To a large extent the analysis lines along party lines. Of course, the early reports on GDP are executed with a lot of holes in the underlying data series with estimates taking the place of actual data series. But on the whole it was a good year for the U.K.; although growth is ending on a withering note, it is not a decisive one and it is still a number that is the envy of much of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief