Global| Sep 26 2018

Global| Sep 26 2018U.K. Distributive Trades Survey Shows Mixed-to-Firm Conditions

Summary

The U.K. distributive trades survey shows mixed performance in September within retailing and within wholesaling as well as between the two sectors. Analysis of this dual-sector two-horizon report is somewhat complicated. U.K. [...]

The U.K. distributive trades survey shows mixed performance in September within retailing and within wholesaling as well as between the two sectors. Analysis of this dual-sector two-horizon report is somewhat complicated. U.K. economic performance has become less certain as inflation has surprisingly flared. The Bank of England is now trying to come to grips with what is the right policy as Britain faces a Brexit transition in six months that is increasingly looking as though it may be a hard-Brexit coupled with what is so far a one month flaring of inflation.

The U.K. distributive trades survey shows mixed performance in September within retailing and within wholesaling as well as between the two sectors. Analysis of this dual-sector two-horizon report is somewhat complicated. U.K. economic performance has become less certain as inflation has surprisingly flared. The Bank of England is now trying to come to grips with what is the right policy as Britain faces a Brexit transition in six months that is increasingly looking as though it may be a hard-Brexit coupled with what is so far a one month flaring of inflation.

Some Brexit issues

Yesterday Theresa May said that no deal would be preferable to what the EU was offering for Brexit. Today we hear that U.K. firms are beginning to implement hard Brexit protocols to try and arrange for the acceptance of their goods in the EU market if there is no orderly Brexit deal. Every man/woman for himself/herself!

A Reuters’ survey claims that as few as 630 U.K.-based finance jobs may have been shifted abroad, a sum much lower than the numbers that had previously been booted about. Still, finance jobs are good jobs and high-paying jobs. Clearly, Brexit effects are increasingly on the minds of the policy-makers as well as the public and shop keepers who wonder what the economy will look and act like in a post-Brexit world.

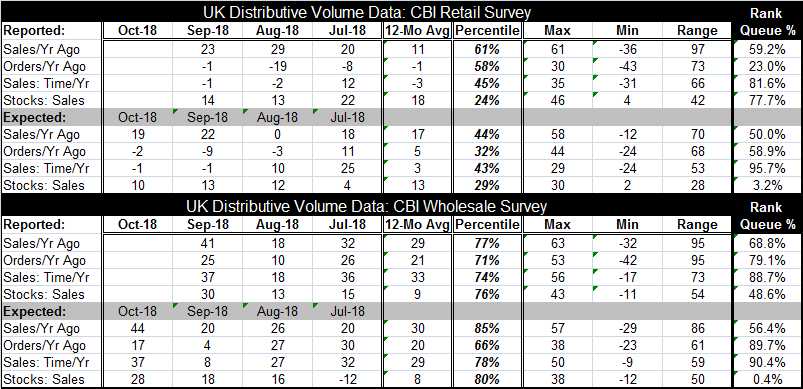

The distributive trades survey for retailers and wholesalers provides current assessments as well as expectations for a range of concepts in each sector. As the Brexit deadline approaches, the expected variables generally are not getting any weaker and generally are somewhat stronger than the current assessments (reported data). I come to that conclusion by comparing for each module (retailing and wholesaling) the reported results with the expected results using the queue standings in the right-hand column of the table. To refresh you understanding of these, queue standings assess each component relative to its own history and create a metric that evaluates the current performance on a percentage scale compared to historic performance. On such a scale, expected metrics are generally (but not completely) outperforming the current or reported metrics. From that, we can draw a tentative conclusion that Brexit has not become a huge drag on the outlook. But the allegation now is that a hard Brexit is likely, more likely –and perhaps preferable to the offer on the table. This turn of events is still quite new so we should keep an eye on these surveys to see what merchants and industrialists think about the future as the Brexit’s day of reckoning draws nearer.

Survey results

Away from Brexit concerns, the reported retail conditions in September worsened month-to-month for sales compared to one year ago, but conditions improved a great deal for orders compared to one year ago and showed a very slight improvement for sales evaluated relative to the time of year. Expected conditions for September compared to August were supposed to show a large step up in sales, a worsened decline in orders and weaker sales for the time of year. However, none of those conditions evolved in September compared to August. For October, retailing sales held onto most of the gain expectations made in September, expected orders remain negative but cut their loses compared to September (rising to -2 from -9) and sales for the time of year are unchanged at the September reading of -1.

The queue rankings tell us that the September conditions in retailing compared to the October expectations show that sales compared to a year ago will weaken in October (meaning a lower ranking in October than the current standing in September). But orders compared to a year ago have a much stronger standing and sales for the time of year are expected to become relatively stronger despite an already high standing for the current response. So there is mixed and somewhat minor evidence here of decay in the future.

A few words about interpreting this survey

I know some of this discussion gets a bit hard to follow in no small part because the CBI metrics (up minus down diffusion responses) do not bridge in a very straight forward way to their queue standings. For example, reported sales year-over-year have a +23 raw diffusion score and that has only a 59th percentile standing while reported orders at -1 have a 23rd percentile standing, but then reported sales for this time of year have an identical -1 diffusion reading and that pairs with a lofty 81.6 percentile standing! There is no intuition about how raw diffusion scores map into percentile queue standings. Basic comparisons can be made on anything on the same line in the table. But comparisons of raw values in one line to the raw value in another line are simply out of line. As for expectations vs. reported data, I think it is fair to look at how changes compare between lines for analogous current vs. expected values as I have done above. But we should stay away from comparing raw diffusion values across lines even for analogous reports and for reported vs. expected treatments for the same concepts.

Distributive trades

In the distributive trades note that conditions uniformly picked up in September compared to August. However, the change in expectations from August to September had expected step downs in all but the stock-sales rating. For October, all expectations components have higher diffusion values than for expectations in September. And the October rank standings are above the standings for reported values in September for all components except for sales compared to one year ago. That marks expectations as mostly stronger.

Summing up

On balance, the expectations series may have more validity when viewed as a trend rather than as an indicator of the month ahead. In retailing sales expectations are steady and firm while orders expectations show some decay after a long period (back to early 2016) of trending to higher readings. Wholesaling current and expected trends appear to be holding up better that retail trends. For retailing sales for this time of year viewed as a reported result or as an expectation, both show a pronounced tendency to hug the zero line. Since early 2017, with the exception of a few random fluctuations, this has been the behavior. Retailing in the U.K. is looking slightly more challenged than wholesaling. But the potential for a real negative Brexit shock is still something not to be dismissed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief