Global| Jan 28 2020

Global| Jan 28 2020U.K. Distributive Trades Survey Points to Weakness

Summary

The retail CBI survey has solid signaling power for U.K. retail sales The small table below extracts the percentile standing metrics from the large table below to feature their message. The message is clearly that current retailing [...]

The retail CBI survey has solid signaling power for U.K. retail sales

The retail CBI survey has solid signaling power for U.K. retail sales

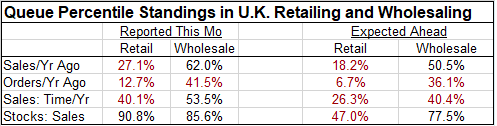

The small table below extracts the percentile standing metrics from the large table below to feature their message. The message is clearly that current retailing metrics have standings below their medians (below 50%) except for stocks – and that actually makes the evaluation even worse news. For wholesaling current orders are below their median with the two sales series are barely or mildly above their 50% or median marks. Wholesalers also have much stronger inventories rankings than sales or orders rankings replicating the signal that inventories are fat not lean. Such a development says that sales are weaker than inventories. That suggests that firms will be looking to get inventories back into alignment with sales either by cutting prices to generate sales and reduce inventories or by cutting orders.

Expectations are weaker in each case for wholesaling and retailing compared to current response standings. So as weak as conditions are they are expected to weaken further and this is expected to bring inventories more into balance as expected inventories have lower standings than their current rank for both retailing and for wholesaling. Retailers expect to get stocks back below their median while wholesalers see the excess inventory conditions lingering even in the period ahead.

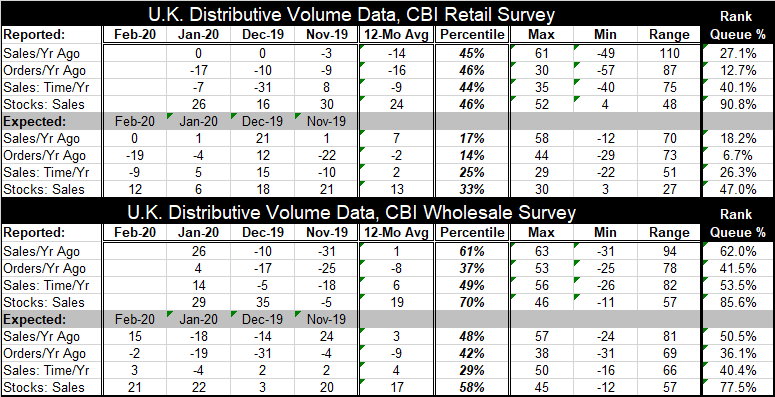

The distributive trade survey with both retail and wholesaling components presents net readings for four variables in real time and the same four again as expectations. In PMI data we glorify the level of 50 on diffusion indexes or point attention to values above zero for net readings (up minus down; better less worse, etc.) and those latter responses are comparable to the data as presented from the CBI survey. But there is more to the statistics than their relationship to zero. The table below ranks the net readings in their respective historic queues of data on observations back to 1996. In this presentation 100% is high or strong and 0% is low or weak. The percentages tell how often a reading is ‘this weak or weaker.’

Retailing

The raw (net) diffusion entries show a continued flat reading for retail sales (compared to a year ago) in January, the same as in December. Sales for ‘the time of year’ show less weakness in January at -7 compared to -31 in December. Inventories are even higher in January than in December. Compared to 12-month averages current standings show an improvement of sales evaluated year-over-year, a slight worsening for orders and a slight improvement for sales evaluated relative to the time of year. Retailing expectations are for February. They show month-to-month deterioration for both sales metrics and for orders with the inventory imbalance worsening. Retail activity has about the same net value or slightly improved (for time of year) in January relative to the indicators’ respective 12-month averages. Expectations are weaker in February than their 12-month averages across the board. Those conditions make the sector ripe for close attention. The percentile standing levels are uniformly weak and considerably weak at that.

Wholesaling

In January, the wholesaling activity gauges all are improved, moving up to positive net readings from negative net readings in December. Even the inventory variable has ‘improved’ falling slightly from its higher December value but to a still-high level. A wholesaling metrics for current conditions are above their 12-month averages. And referring back to the percentile standings data, wholesaling reports in January show readings that mostly are above their respective 50 percentile standings (exception: orders). Expectations offer a similar picture. Expectations do improve across the board in February, compared to the January level. Expectations in February also are improved relative to their 12-month averages (one small exception: sales for time of year). However, recall that expectations standings are still barely at or are below their medians for their activity measures of sales and orders. So while conditions are improving for current wholesaling and expectations, the overall situation remains sub-par. And the deterioration in retailing expectations could yet pose an issue for wholesaling.

Summing up

U.K. distributive trades survey continues to tell a cautionary tale of developments in retailing and wholesaling. Both sectors are still caught with one foot this side of Brexit and the other foot on the other side- wherever that is. By that, I mean that firms are doing business in a pre-Brexit environment but are very much planning for a doing business in a post-Brexit environment and that may account for why inventory levels are still being held so high as a hedge against any potential Brexit-induced interruptions to the supply chain of goods. Brexit uncertainty of some sorts has been reduced, but for the particulars of a business there remains a high degree of uncertainty about what the future will look like.

Coronavirus

Europe is not on the front lines of fighting the coronavirus. But Asia is important to global growth and Asian economics – especially China - are being hard hit. Beyond the global slowdown dimension which should not be underplayed especially given the impact it has already had on stocks, bonds and oil prices, and other commodities, there are also local concerns. A German has contracted the coronavirus even though he never left Germany, as he had a Chinese visitor. The issue of the transmission of this virus is under study and all I know about it so far is that it spreads asymptomatically- before symptoms display themselves. That makes stopping contagion tricky business. Heathrow airport, a vital international transportation hub, has already put special policies in play to try to contain any spread of the virus. Europe will find itself at risk to these ancillary factors. Still, these risks are palpable; the less vigilant Europe is the more at risk it will be. For now the coronavirus looks like it spreads easily. As of today, it has killed 106. It is hard to handicap its potential, but now clearly is the time to contain it. A number of countries are planning to fly their own citizens out of the Wuhan danger zone. Hong Kong has shut its border to visitors from the infected province. While these are all laudable actions to contain the virus which should be viewed as ‘Job One’ there will be adverse knock-on effects for the global economy. That is one clear message from markets.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief