Global| Dec 19 2014

Global| Dec 19 2014U.K. Confidence Dips; Will the Slip Be Ongoing?

Summary

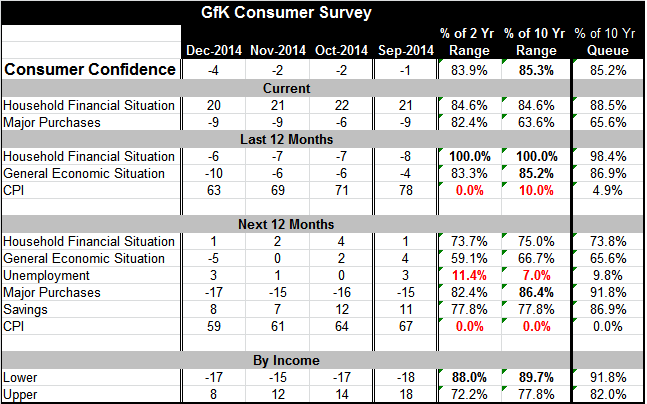

The GfK reading for U.K. consumer confidence fell to -4 in December from -2 in November. The -4 reading is the weakest reading in nine months, since March's reading of -5. Since May, the index had been in a range of +1 to -3. The [...]

The GfK reading for U.K. consumer confidence fell to -4 in December from -2 in November. The -4 reading is the weakest reading in nine months, since March's reading of -5. Since May, the index had been in a range of +1 to -3. The December reading takes the index to a new local low.

The GfK reading for U.K. consumer confidence fell to -4 in December from -2 in November. The -4 reading is the weakest reading in nine months, since March's reading of -5. Since May, the index had been in a range of +1 to -3. The December reading takes the index to a new local low.

Consumer sentiment stands at the 85th percentile of its historic queue of values in December, a still-strong reading that is better only 15% of the time. The household financial situation slipped to 20 from 21 but still has an 88th percentile standing. However, the environment for making major purchases, while steady in December, stands only in the 65th percentile of its historic range, a middling standing.

Over the last 12 months, the economy was rated quite solidly. The household situation improved to post a 98th percentile standing. The general economic situation, however, saw its assessment fall sharply to -10 in December from -6 in November but still posted a strong 86th percentile standing. Inflation was low rated with a 4th percentile standing.

Over the next 12 months, assessments are somewhat mixed and most of the metrics have deteriorated compared to their November values, but the standings are generally still quite good. The expected household financial situation has a 73rd percentile standing; that is still firm but is down considerably from its current and last 12-month assessments. The general economic situation slips to its 65th percentile standing well below its 86th percentile standing currently. Unemployment expectations have ticked up in December but still have only a 9th percentile standing that is still reasonably low. The expected environment for major purchases has a strong 91st percentile standing, well above its current value. The environment for saving is good with an 86th percentile standing. The standing for expected inflation is at zero; there is no fear of inflation whatsoever.

By income classifications, the environment for both the bottom and top income cohorts saw some setback in December, but both still have strong historic standings with lower income cohort reporting a 91st percentile standing and upper income cohort reporting an 82nd percentile standing.

On balance, the slippage in the GfK index is revealed to be mostly in peoples' expectations for the 12 months ahead. The current situation is solid. The past 12 months were generally quite good. But for the period ahead there is some slippage expected and it is more or less across the board.

In some sense, the slippage is not surprising because an index cannot attain such a high standing and keep it for too long for arithmetic reasons. An economy cannot operate in the top 85% of its data queue for more than 15% of the time! The U.K. has seen a period of great recovery from some poor economic circumstances. Consumer sentiment hit its cycle low in July 2008. It then had a sharp recovery to October 2009 and then slipped with confidence making a slightly higher cyclical low in December 2011. From that point on, the recovery in confidence has been gathering pace and the uptrend only began to falter in June 2014 and has only recently turned lower. It has been quite a period of recovery for confidence.

What we cannot tell is whether confidence will now stay on this plateau or if consumers are going to continue to cut their expectations for the future. The U.K. economy is doing well. Recent retail sales results and surveys have been quite upbeat and as consumer recognizes that the Bank of England has inflation under control. But the world environment is still quite weak and there is no escaping the U.K. proximity to the troubles in the euro area. At some point, it becomes progressively harder for the U.K. economy to perform well and swim against the current that it being set in EMU and throughout the rest of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief