Global| Feb 18 2015

Global| Feb 18 2015U.K. Claimants Continue to Drop

Summary

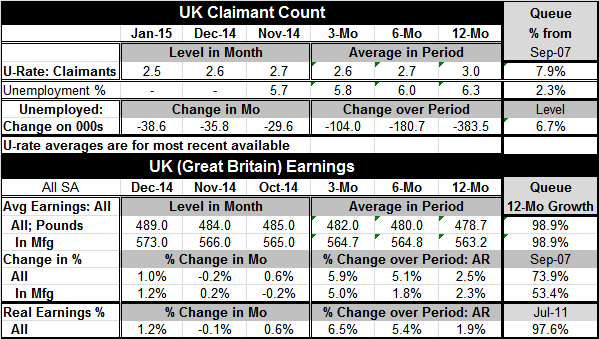

U.K. claimant count paints a wonderful ongoing recovery picture of the economy. The number of claimants and their associated rate of unemployment surged higher in the financial crisis/recession and have since swooped lower to register [...]

U.K. claimant count paints a wonderful ongoing recovery picture of the economy. The number of claimants and their associated rate of unemployment surged higher in the financial crisis/recession and have since swooped lower to register readings very much in step with pre-crisis levels.

U.K. claimant count paints a wonderful ongoing recovery picture of the economy. The number of claimants and their associated rate of unemployment surged higher in the financial crisis/recession and have since swooped lower to register readings very much in step with pre-crisis levels.

The level of unemployed and the claimant unemployment rate each are in the lower 10% of their respective historic queue of values going back to late 2007. Levels of compensation have been advancing as the current compensation (in levels: pounds sterling) stand in the top 1.1% of their respective historic rankings for overall compensation as well as for compensation in manufacturing alone. Measured as year-over-year percentage changes, these metrics step back a good deal but still show some life. Manufacturing compensation's growth stands only in its 53rd queue percentile since late 2007 while overall compensation stands in its 73rd percentile.

Of course, inflation has slowed and deflation is the new enemy. When overall inflation is lower, we expect wage and compensation gains to be somewhat in step. And we see that when we evaluate real earnings. U.K. real earnings growth trends are in their top 3% historically. In the U.K., labor is maintaining, or even advancing, its compensation relative to inflation much better than in the U.S. where wage trends- however measured- have been unable to mount a head of steam. The recent U.K. data are up-to-date though December when the compensation trends experienced a pop.

In the BoE recent decision, all MPC members looked over the U.K. data and decided that the right thing to do was to hold policy steady. However, there is MPC divergence over the notion of where policy will go next. It is clear from looking at the data that there is room for divergence in views. U.K. inflation is carving out new lows. But economic performance is holding up and improving. On top of that the U.K. is plugged by trade flows into the U.S. that had been showing better growth and has mounted persistently strong job growth. In Europe, another strong growth influence through trade on the U.K., a massive ECB program of QE is being geared up. Meanwhile, the German economy is simply doing better.

Will the U.K. be helped by EMU improvement? Does the U.S. growth reach stretch across the pond strongly enough? Is the financial sector healed and able to absorb rate hikes or less QE? All of these questions require some degree of weighing and balancing. The U.K. MPC members, while on the same page for now, are prepared to turn those pages at different speeds in the future. It is not a surprising revelation but one to keep an eye on. With growth holding up or doing better while inflation undershoots, the basic monetary policy message remains mixed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief