Global| Nov 16 2016

Global| Nov 16 2016U.K. Claimant Count Ticks Higher As Slow Erosion Begins to Kick In

Summary

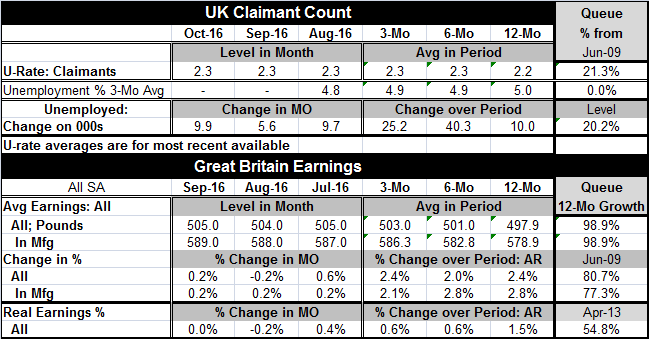

The U.K. claimant count ticked higher as the claimant rate of unemployment remained stuck at 2.3%. The change in the number unemployed crept slightly higher in October. The net increase in claimants over three months was 25.2K [...]

The U.K. claimant count ticked higher as the claimant rate of unemployment remained stuck at 2.3%. The change in the number unemployed crept slightly higher in October. The net increase in claimants over three months was 25.2K compared to 40.3K over six months, implying a slightly higher pace of displacement. Still, the total number unemployed has been lower only 20% of the time since mid-2009. The claimant unemployment rate has been lower about 21% of the time. The overall labor force survey rate of unemployment at 4.8% in August is its lowest on this time span.

The U.K. claimant count ticked higher as the claimant rate of unemployment remained stuck at 2.3%. The change in the number unemployed crept slightly higher in October. The net increase in claimants over three months was 25.2K compared to 40.3K over six months, implying a slightly higher pace of displacement. Still, the total number unemployed has been lower only 20% of the time since mid-2009. The claimant unemployment rate has been lower about 21% of the time. The overall labor force survey rate of unemployment at 4.8% in August is its lowest on this time span.

Average earnings, while ticking higher, are less impressive in real terms. The level of nominal earnings is this high or higher only 1.1% of the time; that standing designates this as the high reading on this period. Nominal wages tend to grow over time so this is a normal reading. The percentage standing of the 12-month growth in earnings has been higher only about 20% of the time or 23% of the time for manufacturing. Earnings growth is solid by historic standards but not impressively strong. Deflated and expressed in real terms, real earnings were flat in September after falling in August and their 12-month gain of 1.5% has a 54th percentile standing in its historic queue of data marking this as an exceptionally moderate pace of real earnings growth, barely above its period median (the median reading occurs at its 50th percentile).

These are unremarkable earnings for an economy with weakening exchange rate. Real earnings peaked in this recent cycle at a 3.8% year-on-year gain in March 2015 and that pace has eroded steadily to the 1.5% pace we see today. Sterling is weakening again on a leaked report (yesterday) that the government does not have a Brexit plan and that factions are still hammering out details. Beyond that, Eurogroup president Jeroen Dijsselbloem said that Brexit negotiations are going to be complex and that the process could take longer than the scheduled two years to conclude. All this seems to imply that the U.K. will be a zone of uncertainty for a very extended period of time, leaving businesses unsure of what they are going to be able to do in the future and likely impairing their willingness to invest in projects that involve EU commerce during the period until the final result is resolved. This could, of course, send further disturbances through the labor market.

The fact that Brexit has not hit the U.K. economy especially hard is unsurprising in the wake of these details. It should be clear that one of the main impacts over the next three years or so as the U.K. prepares for Brexit and Parliament has its say will be this extended period of reduced investment and uncertainty. Business as usual will be able to go on, but businesses will be reluctant to expand and U.K. competitors may be able to move aggressively to exploit the uncertainty about the future relations. Some U.K. firms may opt to invest inside the EU to preserve markets they currently have and to protect themselves in the event of an adverse ruling that could impact some critical phase of their business. If that happens, the impact of Brexit will shift forward.

In the end, when Brexit details are decided, there may be more of a jolt to markets as the reality and details become clear. By that time, however, U.K. firms may already have made their peace with the coming changes and already adjusted their business in view of the changed circumstance if those changes are well enough telegraphed in the negotiation process. It is not clear how transparent that process will be. All this explains why Brexit will be stretched out and why it will be hard to get a grip on the timing and magnitude of the actual impact.

For now the BOE stimulus and weakness in the pound sterling have helped to provide buffers against deteriorated expectations. But these mechanisms will have limited utility moving forward as firms will be reluctant to respond to even monetary or exchange rate stimulus until the conditions of their commercial future are clarified. In short, Brexit has created a mess that the U.K. will be mired in for quite a long time unless firms leave the U.K. before they know their fate in an effort to eliminate uncertainty. Given the parliamentary form of government, the Brexit negotiations could well outlast the current government. If that were to happen, the negotiations process might have to be restarted in mid-stream. We might regard that as the horror story of possibilities.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief