Global| Mar 15 2017

Global| Mar 15 2017U.K. Claimant Count Drops As U.K. Unemployment Rate Hits Lowest Mark Since 1975

Summary

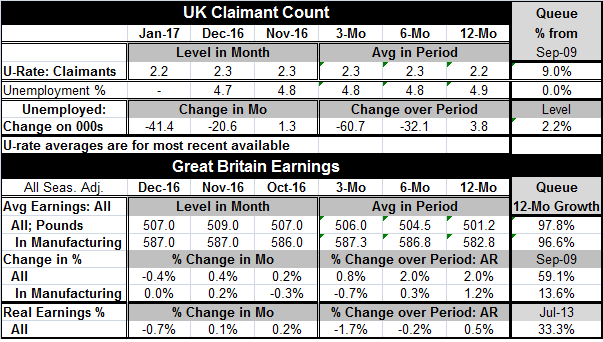

The U.K. claimant count continues to drift lower from already low readings. The U.K. ILO unemployment rate has fallen to 4.7% (as of December), marking its lowest sojourn since 1975 a better than 40-year low and besting the Germans [...]

The U.K. claimant count continues to drift lower from already low readings. The U.K. ILO unemployment rate has fallen to 4.7% (as of December), marking its lowest sojourn since 1975 a better than 40-year low and besting the Germans whose rate is only the lowest since German reunification.

The U.K. claimant count continues to drift lower from already low readings. The U.K. ILO unemployment rate has fallen to 4.7% (as of December), marking its lowest sojourn since 1975 a better than 40-year low and besting the Germans whose rate is only the lowest since German reunification.

While the U.S., Germany, the U.K., and (as always) Japan have very low unemployment rates, most of the rest of Europe does not. And despite the fact that the U.S. and U.K. have some pressure on inflation, from rising oil prices and a weak currency in the case of the U.K., wages really are not off to the races in either of the two countries. U.S. wage inflation for the economies preferred economic measure without supervisory workers is dead flat at a 2.5% pace. In the U.K., earnings are up at a 2% pace year-on-year and at a 2% pace over six months but at a weaker 0.8% pace over three months. Despite somewhat elevated national inflation, a weak pound and a low overall unemployment rate, British wages are not under pressure. That should interest the Keynesians in the land of Keynes and give them something to think about. Why are low unemployment rates not stoking inflation in either the U.S. or the U.K.?

The U.K., of course, faces special circumstances. In a survey by the Royal Institution of Chartered Surveyors released Wednesday, the group found that Britain could lose about 200,000 construction jobs in the wake of Brexit. That's about 8% of the workforce. So while conditions in the British job market may seem cozy now, there is a future that may be much less cozy and less inviting. And British workers may already be bracing for it.

For the time being (a rather too common preamble to saying anything about the U.K. economy these days), the U.K. economy is doing anywhere from just fine to showing real strength. But that strength is not percolating to wages.

In the wake of the U.K. Brexit vote, even the Scotts are talking more loudly and plainly about another Scottish independence vote. I guess having the U.K. out of the EU matters a bit more to them and of course no one had expected a Brexit 'out vote' at the time the Scotts voted to stay 'in.'

All of this is rarified stuff. What is demonstrated is that there are still global pressures holding wages in place. The U.K.'s upcoming Brexit discussions- with results wholly unknown - are nonetheless impacting activity and conditions in the U.K. now. This demonstrates the clear linkage between economics and political decisions. And it is a reminder of our own inability to see the future clearly and to plan ahead. No one saw a Brexit 'out vote' coming. No one saw Donald Trump elected in the United States. And now there are other important elections percolating in Europe. The future is unknown and it always will be. We can plan for it, but even the best laid plans will go awry and that about sums up where we are today in Europe, the U.S., and Asia.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief