Global| Jul 23 2019

Global| Jul 23 2019U.K. CBI Survey-Weaker with Improved Outlook at Least on Paper; Reality May Be Grimmer Than It Seems

Summary

A plunge in orders vs. a slight uptick in expected output ahead Note that sustained divergences between these two series simply do not exist. Boris 'Hard-Brexit' Johnson, the new leader of the Conservative Party, will be the new Prime [...]

A plunge in orders vs. a slight uptick in expected output ahead

A plunge in orders vs. a slight uptick in expected output ahead

Note that sustained divergences between these two series simply do not exist.

Boris 'Hard-Brexit' Johnson, the new leader of the Conservative Party, will be the new Prime Minister replacing Theresa May. He seems to be inheriting an economy that is beginning to show some wear and tear. The EU has welcomed him by reminding him that they will not renegotiate the Brexit conditions. It is not clear what Johnson can do other take the U.K. off the cliff of hard Brexit and have his own personal 'Thelma and Louise' moment as he has promised.

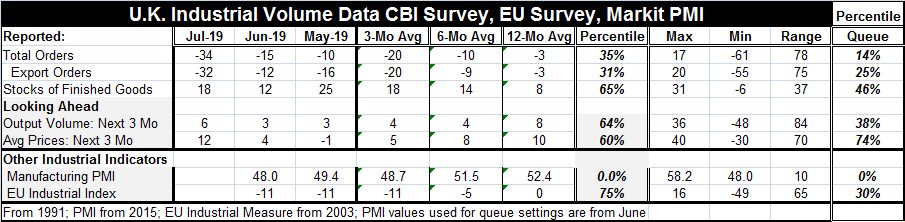

Meanwhile, the CBI report on the state of British industry shows sharp erosion in July as total orders have fallen from a June reading of -15 to a July reading of -34. That drops the orders response to the lower 14th percentile of its queue of readings since 1991.

Export orders also weakened in July, dropping to a -32 reading from June's -12. The 12-month, six-month and three-month averages show that the progression of total and export orders has been toward greater weakness for some time. However, the current reading for export orders of -32 is still a very weak 25th percentile reading. In ranking terms, it is not quite as weak as total orders, but it is quite weak- a bottom one fourth of rank-standing.

The sequential averages for the stock of finished goods on hand are not so easy to interpret. They have been moving up and that is often a sign of a growing excess that precedes the need for reduction that often leads to industrial cutbacks and layoffs. In this case, it may be that stocks were built up and overbuilt as a buffer against unknown Brexit exigencies. Stocks have a middle of the road reading, a 46th percentile standing. The percentile standing is much higher than for orders, but it is still below its historic median (medians for rankings are at 50).

The outlook shows an improvement on the month for the volume of output expected to be created over the next three months- a surprise result given the order weakness. The sequential averages for output expectations have been declining then stabilized over three months. This month output expectations have risen above their most recent three-month and six-month averages. Still, the ranking for the outlook metric is only in its 38th percentile- below its historic median. Despite a positive reading, it is not impressive when compared to the outlook that industrialists normally have.

Price expectations that had been losing momentum in terms of their moving average shot up suddenly in July. They have a relatively high 74th percentile standing. The price reading had been more in this range in February of this year and earlier.

Other industrial indicators show weakness. The Markit manufacturing PMI is up-to-date through June. It shows the lowest reading since January 2015 and longer. The EU industrial index, also available through June, shows a weak, 30th percentile standing.

On balance, there is not much in this report that is upbeat despite the turn higher for the outlook readings. On close inspection, that is not such a positive development since it still projects output below its historic median expectation by a good measure. The CBI survey and other industrial assessments of the current state of British industry are weak and slipping. Yesterday the NIESR wondered if the U.K. economy had not already slipped into a downturn. The U.K. economy does appear to be slipping into a more challenging environment with the huge economic/political challenge of Brexit still ahead of it. The U.K. had better say its prayers that Mr. Johnson and his love of Brexit and lack of fear over a hard one is the right man to lead it through this challenging period: here he comes and here it comes.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief