Global| Sep 22 2016

Global| Sep 22 2016U.K. CBI Survey Turns Upbeat: Temper Your Enthusiasm

Summary

Conflicting numbers and expectations stalk the U.K. outlook. In the wake of Brexit, the early `Big News' is that few economic reports seem to show much impact from the vote. The Office for National Statistics (ONS) just issued a [...]

Conflicting numbers and expectations stalk the U.K. outlook. In the wake of Brexit, the early `Big News' is that few economic reports seem to show much impact from the vote. The Office for National Statistics (ONS) just issued a report that found little evidence of weakness related to Brexit. Of course, Brexit is still an unknown beast. And it is not until EU-UK negotiations get into full swing that anyone can reasonably handicap what it is that the U.K. may stand to lose. The bargaining process here is complicated because the EU can't be too harsh on the U.K. for leaving its fold without suffering serious blow back from that itself. As a result, handicapping the prospects under Brexit is difficult. So far, markets are not all that much affected, but the BOE has been playing it safe by stuffing loads of stimulus in the pipeline like it's a Christmas stocking.

Conflicting numbers and expectations stalk the U.K. outlook. In the wake of Brexit, the early `Big News' is that few economic reports seem to show much impact from the vote. The Office for National Statistics (ONS) just issued a report that found little evidence of weakness related to Brexit. Of course, Brexit is still an unknown beast. And it is not until EU-UK negotiations get into full swing that anyone can reasonably handicap what it is that the U.K. may stand to lose. The bargaining process here is complicated because the EU can't be too harsh on the U.K. for leaving its fold without suffering serious blow back from that itself. As a result, handicapping the prospects under Brexit is difficult. So far, markets are not all that much affected, but the BOE has been playing it safe by stuffing loads of stimulus in the pipeline like it's a Christmas stocking.

For its part, the Bank of England still sees a challenging period for financial stability. It wants to keep rules for banks tight as it prepares for the Brexit negotiations. "The United Kingdom faces a challenging period of uncertainty and adjustment," the Bank of England's Financial Policy Committee said in a quarterly statement. The Financial Policy Committee did not make any new policy initiatives, however.

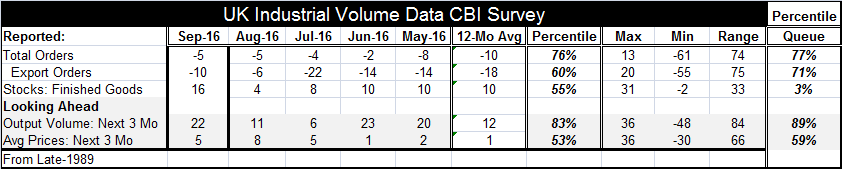

It is to the BOE stimulus that the CBI's September survey seems to be reacting with a strong reading. The change in output expected in three-months jumped to a net reading of 22 in September from 11 in August. This brings the reading up into the top 11% of all historic readings since late-1989. The gain is aided by export orders which did backtrack on the month but at a reading of -10 sit above their 12-month average of -18 and stand in the 71st percentile of their historic queue of data (top 29%).

While the survey by the Confederation of British industry (CBI) is strong for manufacturing, it stands in marked contrast to a new survey of small and medium-sized businesses in the U.K. that are concerned about the outlook. A study by the Federation of Small Businesses (FSB), the first survey since the Brexit vote, shows the second largest fall in confidence in the index's history. The survey has now weakened for three consecutive quarters. It is the first negative reading for confidence on the part of small business since 2012.

Clearly, there are different points of view on the U.K. economy and its prospects and Brexit will loom as an important aspect in most of them. Small business owners may feel at risk to the whim of the economy, while larger corporations may be operating on a much larger scale and across various geographical regions with much better access to capital should new investment be required. Also in the CBI survey the outlook portion is not vaguely `about confidence' but about a specific expected measure of performance over the coming three-months, a very well-defined period. That is a relatively near-term window with BOE stimulus still hot in the pipeline.

Certainly, the strong and timely action by the BOE and its impact in driving the exchange rate lower go a long way to explaining why the CBI survey is doing better. But the lingering uncertainty over the actual negotiations is still an issue for shop owners who will face many real-world decisions before the Brexit negotiations are started and concluded, like whether to sign a new lease where they are doing business or whether to move their location. Brexit will have consequences and large firms are better-paced to roll with the punches while smaller firms are simply at risk to what may seem to them to be capricious forces.

On balance, there will continue to be a waiting game played in the U.K. over the Brexit impact and some will play it better than others. There will eventually be decisions made and they will impact some businesses hard and maybe leave others nearly unscathed. As we get closer to the date of serious Brexit negotiations, a period that may still be a year in the future, we can expect rumors to fly and market impacts to emerge. The process will have to start with a formal announcement by the U.K. to leave, but that will only initiate the proceedings; the actual negotiations will come later. For once, U.K. negotiations will be easy since the U.K. will only have to represent itself and its own interests. The EU side will find a welter of conflicting interests vying for attention. We already know that Paris would greatly like to take on the role of the financial sector location, but that is clearly impossible given how expensive Paris is. The prospect of negotiating international loans and the process of their adjudication under French law seems highly unlikely to be favorably viewed. Countries in the EU may have a wish list, but certain pieces of these negotiations will simply fall into place and will be resolved. But the process will not necessarily be smooth. And EMU members will have conflicting agendas among themselves in the process. I would urge caution over the complacency that so far there are few signs of any effect from Brexit. It's a bit like noting that a fighter remains undamaged by his opponent who has swung at him while knowing that the fist is still in full flight. The impact of Brexit is coming.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief