Global| Mar 23 2021

Global| Mar 23 2021U.K. CBI Survey Shows Improving Industrial Sector...Will Virus Politics Interfere?

Summary

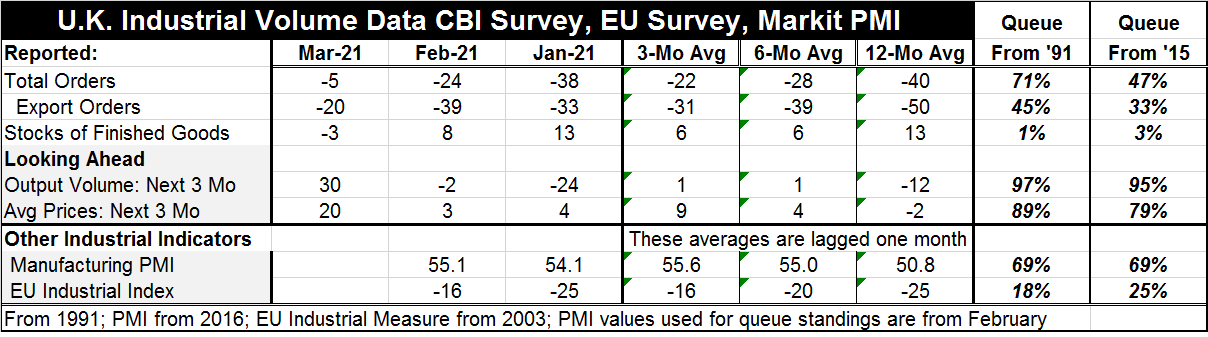

The U.K. CBI industrial trends survey shows a sharp improvement in orders in March. The total order reading jumped to -5 from February’s -24 as its sequential averages echoed the ongoing improvement in the sector. With that jump in [...]

The U.K. CBI industrial trends survey shows a sharp improvement in orders in March. The total order reading jumped to -5 from February’s -24 as its sequential averages echoed the ongoing improvement in the sector. With that jump in March, the reading now has a 71st percentile standing in its queue of data from 1991, a relatively firm and solid performance reading. The improvement of overall orders was helped by export orders which also moved sharply higher. Export orders jumped to -20 in Mach from -39 in February to post a 45th percentile standing in its queue of data back to 1991. Total orders have improved to a stronger position than export orders, but both are contributing to an upswing. Export orders are undoubtedly being held back by the new post-Brexit U.K. trade relations with the EU. This is a massive one-month jump. On data stretching back to 1988, this month’s month-to-month jump in expected output over the next three months is the second highest change in this month-to-month reading.

The U.K. CBI industrial trends survey shows a sharp improvement in orders in March. The total order reading jumped to -5 from February’s -24 as its sequential averages echoed the ongoing improvement in the sector. With that jump in March, the reading now has a 71st percentile standing in its queue of data from 1991, a relatively firm and solid performance reading. The improvement of overall orders was helped by export orders which also moved sharply higher. Export orders jumped to -20 in Mach from -39 in February to post a 45th percentile standing in its queue of data back to 1991. Total orders have improved to a stronger position than export orders, but both are contributing to an upswing. Export orders are undoubtedly being held back by the new post-Brexit U.K. trade relations with the EU. This is a massive one-month jump. On data stretching back to 1988, this month’s month-to-month jump in expected output over the next three months is the second highest change in this month-to-month reading.

Stocks of finished goods are quite low and in the lower one percentile of their range back to 1991. With the virus impacting supply chains, and with a new Brexit trade relationship with the EU members, inventories are weak.

Looking ahead, expected output volume has surge to 30 in March from -2 in February. The sequential averages (three-month, six-month and 12-month) have been very weak; this month’s jump is a spurt out of the blue. The reading was last this strong in April 2017. The change in expected output as well as the change in orders month-to-month are each the second highest month-to-month changes posted since at least May 2000. The CBI index recorded this month is quite impressive, not so much for the level of the reading it has obtained but for the sharp break with past readings.

Clouds on the Horizon

However, there are still clouds on the horizon. The U.K. on its own is making outstanding progress vs. the virus. Deaths and infections are dropping sharply and to much more moderate levels despite the more lethal and contagious strain that is circulating. But the U.K. is under threat from the EU that some of its promised shipments of vaccine out of the EU area may not be forthcoming. The EU was slower to order vaccine and production difficulties have hampered supply. Since the U.K. progress is so advanced, the EU wants to retain vaccines made in the EU for use in the EU. That could put U.K. progress into reverse with all sorts of adverse consequences

Milestone as millstone?

"Britain has hit a Covid-19 vaccination milestone with more than half of all adults having had at least one injection, health secretary Matt Hancock said on Saturday, making it the world’s first major economy to achieve that level of inoculation" (Source).

WWII: over. Brexit: concluded. Vaccine wars? Off… but then, on again?

Health experts breathed a sigh of relief after the EU and U.K. avoided a vaccine war earlier this year when the bloc backed down on plans to restrict Covid jab exports. But now hostilities have flared up again in the wake of a fresh threat to block doses bound for Britain while Brussels struggles to meet the EU’s shortfall (Source).

The reinfections in Europe are still an issue and Germany is going to keep a tight lockdown in place even through Easter. The EU has fallen behind other developed countries in obtaining and administering vaccinations.

Rule of law or the rules of the most desperate… laws-be damned?

"…an EU official told Reuters that while "the Brits are insisting that the Halix plant in the Netherlands must deliver the drug substance produced there to them", the stockpile "produced in Halix has to go to the EU". The Leiden-based plant is listed as a supplier of vaccines "in both the contracts that AstraZeneca has signed with Britain and with the European Union", the news agency reports. Despite being named one of the EU’s main sources of production in a deal signed last August, the factory does not have regulatory approval to supply the bloc, the Financial Times (FT) reports" (Source).

Since growth depends on vaccination, this dispute is very important. The EU’s desire to trump what appears to be a superior U.K. claims rests on its observation that the U.K. is doing better than the EU and should therefore stand back and let the EU move up in the queue to obtain vaccines. But the U.K. is fighting a nasty strain of the virus and does not want it to reinvigorate. Plus it seems to have had the better foresight and preparedness in signing contracts.

This is not real warfare and I really do not know what consequences a heavy hand by the EU might mean. It does have leverage to do what it wants since that one plant in question is located in the Netherlands. But documentation (as reported above) seems to validate the U.K. prior claim. In the wake of the U.K.-EU dispute over Brexit, this is just more bad blood. The EU was careful to employ the ‘rule of law’ at every turn in the Brexit negotiations with the U.K., but now that law does not favor the EU position the EU viewpoint has changed. This cannot be good for any European relations. I will let the discussion rest here. It is now a political and legal situation, but it does have real economic consequences as does anything that significantly impacts the virus and vaccination progress. For now U.K. industrial trends are very encouraging.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief