Global| Mar 23 2015

Global| Mar 23 2015U.K. CBI Index Shows Mixed Trends

Summary

The U.K. economy is showing mixed evidence of a slipping industrial sector as industrial sector overall orders have dropped to a five-month low and to their first neutral reading in that span. Export orders are at their weakest over [...]

The U.K. economy is showing mixed evidence of a slipping industrial sector as industrial sector overall orders have dropped to a five-month low and to their first neutral reading in that span. Export orders are at their weakest over two years (26 months). With the EMU kick-starting its program of QE and the U.K.'s own program of QE having been staged a long time ago, the pound sterling's period of being undervalued (and stimulative to industry) is coming to an end.

The U.K. economy is showing mixed evidence of a slipping industrial sector as industrial sector overall orders have dropped to a five-month low and to their first neutral reading in that span. Export orders are at their weakest over two years (26 months). With the EMU kick-starting its program of QE and the U.K.'s own program of QE having been staged a long time ago, the pound sterling's period of being undervalued (and stimulative to industry) is coming to an end.

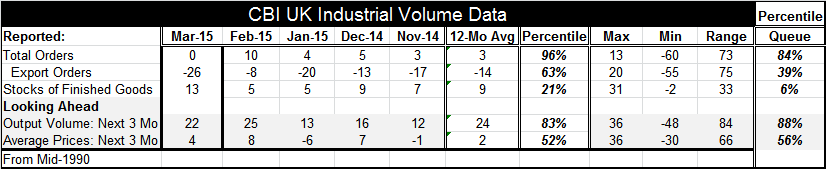

Still, these readings for orders are not as weak as they may seem. The current reading placed in historic context finds a standing at a position that is in the 84th percentile of its data queue, hardly weak! By this relative ranking, overall orders have been stronger only 16% of the time. Export orders, however, are about as weak as they seem. Their -26 net reading has a queue standing in its 39th percentile (weaker only 39% of the time).

The dropping euro exchange rate is playing a role by pushing sterling higher and reducing the U.K.'s competitive advantage for U.K. exporters vs. EMU single-currency members. Sterling on a broad basis is now nearly back to parity after having been undervalued since early-2008.

However, looking ahead the outlook for volume has slipped only to 22 in March from 25 in February. This reading (apart from its February value, of course) is the strongest since September of last year, standing in the 88th percentile of its historic queue of values (stronger only 12% of the time). The outlook for prices has fallen month-to-month to 4 from 8 and that net value stands in the 56th percentile of its historic queue. There is no evidence of inflation being expected. But the output outlook is still quite strong.

What we have is a U.K. economy where the outlook for output is still relatively strong. Orders on hand, have slipped, but are at about the same relative historic standing as the outlook for volume expansion. The volume outlook and orders readings are compatible in percentile standing terms. But what has slipped month-to-month and is a matter of concern is the reading for export orders; that lower 39th percentile standing should raise flags. U.K. exports are approximately 29% of GDP while imports are 32% of GDP. The U.K. is importantly plugged into the world trading system and any loss in competitiveness will impact the economy significantly.

So far it appears that the U.K. economy is prepared to run at a decently firm pace on home grown fuel (domestic demand and orders). But the slippage in foreign orders has to be a problem from the stand point of a more lasting outlook. The U.K. outlook reading in the CBI survey is only for three months ahead. We know that exchange rate changes take more time than that to filer though the economic system.

For now the CBI survey can be called mixed. But with the slippage in export orders there is reason to doubt the overall competitive state of British industry and to raise a question mark about performance in the future. For now the domestic economy has enough strength to keep forward-looking metrics in line, but there should be some skepticism about performance farther down the line.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief