Global| Oct 18 2016

Global| Oct 18 2016U.K. Braces for Waves of Inflation; Are There Lessons for Others?

Summary

The U.K. is bracing for inflation since the pound sterling has been in a tailspin in the wake of the U.K. Brexit vote. Sterling is down from its peak this year by about 16% vs. the dollar and about the same amount vs. the euro. When a [...]

The U.K. is bracing for inflation since the pound sterling has been in a tailspin in the wake of the U.K. Brexit vote. Sterling is down from its peak this year by about 16% vs. the dollar and about the same amount vs. the euro. When a currency falls in value, a country generally sees import prices rise and there are knock-on effects for the domestic price level as the higher cost of imports filters through the economy. As the lesser degree of competition from abroad becomes known, domestic producers gain some scope to raise their prices as well. The Bank of England is bracing for some sort of an inflation overshoot.

The U.K. is bracing for inflation since the pound sterling has been in a tailspin in the wake of the U.K. Brexit vote. Sterling is down from its peak this year by about 16% vs. the dollar and about the same amount vs. the euro. When a currency falls in value, a country generally sees import prices rise and there are knock-on effects for the domestic price level as the higher cost of imports filters through the economy. As the lesser degree of competition from abroad becomes known, domestic producers gain some scope to raise their prices as well. The Bank of England is bracing for some sort of an inflation overshoot.

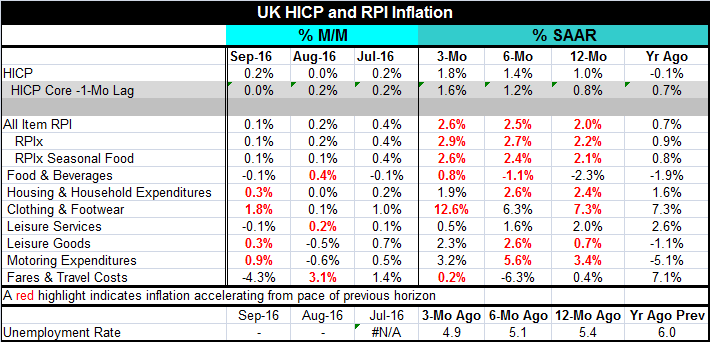

The charts show that inflation already is curving higher in the U.K. on both the HICP and the RPI measures. And the U.K. unemployment rate is relatively low, having fallen by 0.7 percentage points over the past year alone and from about 8% over the last four years to 4.9% currently.

Now for the U.K. the uncertainty of Brexit lies ahead. The BOE has been shoveling in stimulus, but the greatest hit in the short run will be a more gradual and subtle loss from the drying up of investment as firms wait to see what the new financial and economic relationships with Europe will be before firms commit new monies to investment. Thereafter there will be a new sorting out once the post-Brexit relationships and incentives are established. There will be a new set of incentives for U.K. producers in 'that new world' and possibly for foreign firms that had previously located in the U.K. using it as a base from which to export to the rest of the EU. This will be a hard transition to manage. For now there is little to do but wait for the negotiations to conclude and establish new guidelines. There is no way to replace the missing investment activity and no sense in trying to stimulate it since it is waiting for news on what to do next.

For now U.K. inflation is accelerating. The HICP measure shows inflation at 1% over 12 months rising to a 1.4% pace over six months and to a 1.8% pace over three months. Former Bank of England Monetary Policy Committee member Andrew Sentence has been in the news warning that there will be more to come. Despite the difficulty they are having in getting inflation going in the EMU, Sentence is certainly right. The U.K. has an independent monetary policy and has been looser recently to encourage growth and to blunt the trauma from the Brexit vote. In contrast, the ECB is running an easy policy but has less leverage and has relied more on asset purchases at this point and still has had trouble finding enough qualified assets to buy to increase its stimulus. The U.K. has acted quickly and strongly and the pound sterling has responded by falling creating this new inflation impulse- something that is lacking in the EMU. The ECB actions have been slow and less vigorous and have kept the euro weak, but the euro has not fallen with the same gusto that the pound has. The Brexit vote triggered something special.

The U.K. data already show steady acceleration in the HICP, the lagged HICP core, the RPI, the RPI-x, and the RPI-x seasonal food. Major components do not yet show steady accelerations, but that in fact is a trend that is imprinted on the most closely watched aggregations of the inflation measures. That phenomenon more or less confirms that this is real broad inflation instead of some shift in relative prices (as from oil) matriculating up to the headline from an impulse felt in one of the price components or just one sector.

As such the U.K. economy is a reminder that while inflation is dead in the EMU and dead in Japan it still is more than a theoretical possibility. While some places may have all but banged their heads against a wall to try to get inflation in gear, others may do much less and have inflation come visiting even when not beckoned. Conditions still can be generated to produce inflation and this has been and ongoing theme of the hawks in the U.S. who believe that the U.S. itself may be close to triggering its own inflation trip-wire. Global markets are on edge because of this fear. Thus, the U.K. may be a litmus test of the risk that could threaten the U.S. economy. Of course, one huge difference is that the dollar has been rising when the pound sterling has been plunging. So when you look for analogs don't forget to log the differences as well.

The U.K. is an important situation to keep an eye on. It is an important economy in its own right. It is important to both the the U.S. and to Europe in its own way. It is a very important U.S. strategic partner. The negotiations over Brexit will be crucial and will be path-breaking for all - the rest of Europe will be watching and not the least of which because the U.K. is not alone in having a population that is upset with the way the EU has dominated its member countries' domestic agendas. Of course, the BOE is in the hot seat over this, but the U.K. government is even more in the cross hairs should something go wrong. This is a great experiment in the making and one with very important real-world consequences. Enjoy, learn and beware.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief