Global| Oct 23 2020

Global| Oct 23 2020The Virus Continues to Trump the Global Economy; PMIs Broadly Weaken or Tread Water Except in the U.S.

Summary

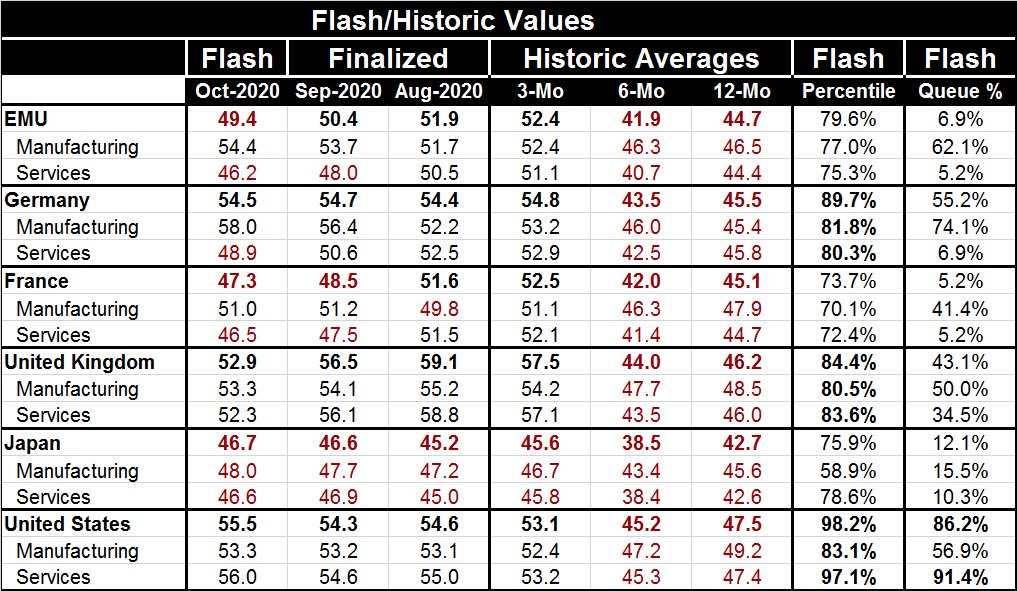

In October manufacturing generally gained a little ground while the services sectors generally eroded for the sample economic units in the table. The U.S. services sector was a major exception, however, as it move strongly higher. As [...]

In October manufacturing generally gained a little ground while the services sectors generally eroded for the sample economic units in the table. The U.S. services sector was a major exception, however, as it move strongly higher. As a result, the U.S. is the only reporter in the table to show a significant composite PMI improvement in October (Japan's composite improved by a single tick on the basis or a manufacturing gain and service sector deterioration.

In October manufacturing generally gained a little ground while the services sectors generally eroded for the sample economic units in the table. The U.S. services sector was a major exception, however, as it move strongly higher. As a result, the U.S. is the only reporter in the table to show a significant composite PMI improvement in October (Japan's composite improved by a single tick on the basis or a manufacturing gain and service sector deterioration.

Broad Weakness

All composite index queue rankings are below their midpoints (on data back to January 2016; that means they rank below 50%) except Germany (55.2%) and the U.S. (86.2%). The U.K. has the manufacturing sector at its median; Germany has manufacturing well above its median and the EMU has manufacturing above its median along with the U.S. Queue rankings for most sectors remain not just below their respective medians but also quite weak. Only Japan has both manufacturing and services sectors with extreme weakness on a ranking basis.

History

The historic average readings (three-month, six-month and 12-month) show that PMI averages over 12 months and six months are uniformly below 50 showing broad contraction for the composites as well as the sectors- for most; in addition, six-month values are below the 12-month values as economies were weakening on those times and have only recently rebounded. Over three months, however, the situation is quite different. This is the period of ongoing rebound from the virus and its first wave. All three-month averages are above 50 except in Japan where none are – although Japan does show numerical PMI improvement from six months to three months, it continues to contract.

The Second Wave

But now there is a second wave of infection spreading. And with that, all composite PMIs in the table are weaker in October than their preceding three-month average (July, August and September) except for Japan and the U.S. In fact, all the U.S. and Japan sector reading are higher in October than in the preceding three-month average while for the rest of the table every comparison shows weakening except for German manufacturing and manufacturing in the EMU (that is strongly aided by the German result).

Bifurcated Growth in Recent Months

For both Germany and EMU manufacturing has been steadily improving in the past two months while services have been weakening. Both France and the U.K. show weakening monthly trends for both manufacturing and services. Japan and the U.S. reveal mixed trends; however, in the end, showing more strength in October than in August.

The Virus Is King

This picture is heavily dominated by the resurgence of the virus. France and Belgium have been hit particularly hard. France has taken actions that will affect 46 million people. Paris and eight other cities will have curfews enforced. The Czech Republic has mandated another nationwide lockdown. Every European country has some new restriction in place except Sweden. Sweden is seeing a lesser rise in infections and has said it is keeping its options open for future action. In the U.S., infections are tending to hit the western states that for the most part were lightly affected by the first round.

Virus > Economics

Again and again and again, we find ourselves trying to do economic analysis and stopped short by the virus. Recoveries start to roll multipliers start to reinforce economic activity then somewhere the infection rate rises and it spreads and before long new invasive polices are put in place to stop the spread that also throttle economic activity. It's a global pattern – and not a good one.

The World as We Know It

Without a vaccine, this process will be nearly endless. Only Sweden may be close enough to reap some of the benefits of herd immunity. Everyplace else the overall infection rate has been kept so low by shutting down that too few people have gotten the virus to create a substantial buffer of immunity. This is the dark side of the shutdown strategy. It is not a cure. It is mitigation, but only with respect to time. If there is not a vaccine, then even with lockdowns the virus will spread despite best efforts to contain it. It will just spread more slowly and interrupt economic activity continually. No one really has come to grip with that except Donald Trump who is up for reelection and has seen his strong economy eviscerated by mitigation strategy then become the one blamed for simply being there. Just as Trump's timing may have been excellent in 2016, timing now seems to have become a huge liability- he is in the wrong place at the wrong time (the oval office in 2020!).

What's Next?

It is clear from the global scope of the virus that there is no magic formula for dealing with it. In an election year, we were never going to get and honest appraisal of the approach in a presidential debate. The captain goes own with his ship- that's the rule. But Europe with much of the compliance baked in the cake that the U.S. officials claim to have sought has not had an easy time controlling the spread. Some have done better than others (naturally), but the reasons for that are not clear and it is not as simple as ‘wear a mask.' The virus is a complicated thing that spreads easily and fortunately does not kill with a great lethality, but it is lethal enough to create an uncomfortably large death toll. Still, it's a virus that seeks out unhealthy people. One thing no one ever points it out how the death toll in the U.S. is higher probably because its citizens are a less healthy people than the Europeans. Americans are out of shape and obese with poor eating habits. The U.S. drug-intensive medical system has been good at keeping sick people alive, but the virus then seeks them out. It is not clear if a person with a severe preexisting condition can outsmart, outwait and out-isolate the virus to survive. Often vaccines do not work as well on people with compromised immune systems...so then what?

This second wave sweeping through Europe should be an eye opener since European infection rates are still low in the general population. How many more waves like this will the global economy have to endure until the virus runs out of steam as did Bird Flu, SARs and MERS? Or must we wait until there is an effective vaccine? How long? Are we really close to having one or not?

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief