Global| May 05 2021

Global| May 05 2021The US Composite PMI Moves Higher As the Rest Mark Time

Summary

The composite PMI measures across an early-reporting group of 16 entities (15 countries and the euro area) show that most of these reporters are expanding and few of them are slowing. The average (unweighted) PMI for this group has [...]

The composite PMI measures across an early-reporting group of 16 entities (15 countries and the euro area) show that most of these reporters are expanding and few of them are slowing. The average (unweighted) PMI for this group has been creeping higher as the 12-month to six-month to three-month progressions indicate successively higher values for the PMI average. Similarly, the number of jurisdictions with composite PMIs below 50 has steadily withered and the number slowing has stabilized at only 2 to 3 over the past three and six months. For the group, the average PMI queue ranking is at its 60.9 the percentile standing; across reporters values generally are up from the 50% level that marks the historic median value for all ranked PMIs.

The composite PMI measures across an early-reporting group of 16 entities (15 countries and the euro area) show that most of these reporters are expanding and few of them are slowing. The average (unweighted) PMI for this group has been creeping higher as the 12-month to six-month to three-month progressions indicate successively higher values for the PMI average. Similarly, the number of jurisdictions with composite PMIs below 50 has steadily withered and the number slowing has stabilized at only 2 to 3 over the past three and six months. For the group, the average PMI queue ranking is at its 60.9 the percentile standing; across reporters values generally are up from the 50% level that marks the historic median value for all ranked PMIs.

Monthly

The monthly data are more volatile and this is reflected in there being more entries those months showing slowing month-to-month than there are over the broader periods in the table. The number of jurisdictions with diffusion readings below 50, however, continues on an improving trend. The simple reported average across these 16 entities is rising steadily monthly as well over the last three months. In April as well as in March, readings surpass the three-month average of 52.9. That is further evidence that the global expansion is establishing roots.

The table that looks at the historic high-low readings and that put the current month’s reading in a queue of historic data to ascertain this month’s historic standing lies below.

High-low percentiles

High-low percentiles

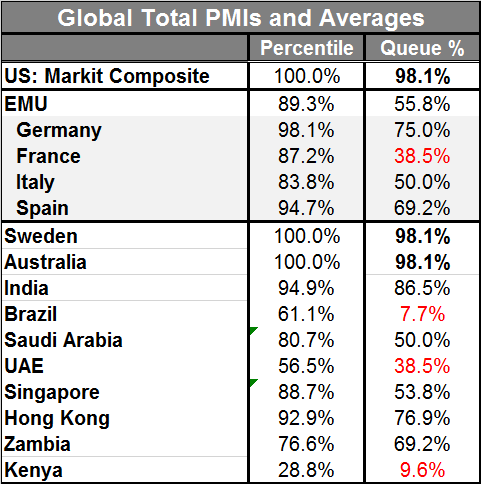

On data back to January 2017, the United States, Sweden and Australia are showing the highest composite readings they have seen on that timeline. Germany, Spain, India and Hong Kong also have extremely strong percentile readings in their top 10% on the same timeline. The EU, France, Italy and Saudi Arabia have top 20 percentile metrics in their respective high-low queues of data (Column: Percentile).

Queue standings: less forgiving

The queue standings (Queue %) show less strength in general. After the top-ranked U.S., Swedish and Australian readings, only India logs a top 20 percentile queue standing and we know the pressures India is under from the spreading virus. Germany and Hong Kong have standings in their respective top 30 queue percentiles.

Italy and Saudi Arabia are at a 50% standing which signals that they reside at their historic median values. France, the UAE, Kenya, and Brazil reside well below their respective medians.

Reconciliations

The percentile column reassures us that there is only one reading this month that lies below the middle of the high-low range since January 2017 (Kenya). The queue standing data are more demanding as they take account of all the observations from the period not just the current one, the highest and the lowest. As such the queue data standings are more powerful results. They show more diversity, less pure strength and more weakness than the percentile column. For example, the Brazil composite PMI lies at the 61% mark between the high and low observations; yet, it has been lower than its current value only 7.7% of the time. Clearly, in terms of stress, the Brazilian index has gotten much lower; however, it still rarely is lower that it is in April. France and the UAE show similar dissonance in the two metrics. Just remember that the two gauges measure different things.

Component weakness

Underneath the surface the composite gauges show much less strength in services and much more strength in the manufacturing sector as a rule. A number of countries do not report out separate manufacturing and services numbers. But for those that do, there are only a few super strong service regions (the U.S. is one of them) and there are four countries from this group with service sector standings in their bottom 30th percentile or weaker. These are: Brazil, Germany, the euro area and France. The composites collapse the service sector and manufacturing sector into a single reading, but we know that manufacturing is doing much better than services and yet we know that it is a bit of an illusion to mix them together since the service sector is the sector that creates the jobs- and without jobs national welfare can’t really improve much.

Conclusions

The composite readings mask some of the ongoing pain even in regions that seem to have quite solid ranking responses. This is a warning to be careful how you use and vet the PMI data. The real economy continues to struggle in some very important ways and the service sector will not right itself until the virus is quite substantially collared. Meanwhile, the virus is still in the process of showing us just how dangerous it can be as it rips through India. We are not sure, but we hope that the countries with highly inoculated populations have reached a point of some safety, where such backsliding is no longer possible. We hope further that the developing economies can follow in these footsteps directly. We know that all of this will take time and that we cannot predict or know about the virus’ mutations and prospects in the future. Still, there seems to be a will to open up and not to plan for the worst, but to lean on the progress afforded by the vaccines and to try to build on that as safely as possible. That should pave the way for much better growth ahead as long as the virus does not do something quite unexpected.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief