Global| May 12 2009

Global| May 12 2009The UK Halts Its String Of MFG Output Declines

Summary

In the UK overall MFG output is flat in March. Despite the fall, the output of durable consumer goods is up in March and its trend shows a diminishing pace of decline. Consumer nondurable output is up for three months in a row and [...]

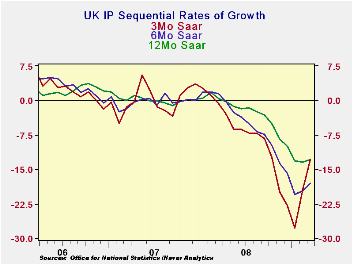

In the UK overall MFG output is flat in March. Despite the

fall, the output of durable consumer goods is up in March and its trend

shows a diminishing pace of decline. Consumer nondurable output is up

for three months in a row and sports an accelerating up-trend. For

intermediate goods the pace of decline is still fairly rapid and its

growth rate profile is more or less stuck at seriously negative rates

of growth. Capital goods remains as the most severely impacted sector

with decelerations in output growth still in place.

By detailed sector, food, drink and tobacco output is

accelerating and showing strong positive growth over three-months.

Textile and leather goods output has accelerated its decline over

three-months. Motor vehicles output is still dire with very strong

rates of negative growth. Mining activity has worsened over six months

then maintained that strong pace of decline. Overall utilities output

has been trimmed increasingly aggressively in recent months –a bad

overall sign.

While the UK does have some bright spots and the retail BRC

survey has produced a strong retail sales result for April, the UK

trends are still seriously troubled for industry. Signs of some

improvement in retailing and an increase in housing sentiment are

helpful since a consumer revival that stokes demand will lift output.

And while there are some encouraging signs from the consumer there is

little evidence so far that this is helping capital goods industries

much. The cessation of the drop in IP is good news. But the industrial

sector is caught between what seems to be some improvement by the

consumer amid still worsening conditions for capital goods. The nascent

improvement in the UK MFG PMI suggests that there may be some support

in the pipeline for the sector as a whole, however. Meanwhile the

up-turn in the three-month trend for IP itself also suggests that the

worst may be over. Industry remains seriously troubled, but this is

probably the beginning of a true turn for the UK economy.

| UK IP and MFG | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Mar 09 |

Feb 09 |

Mar 09 |

Feb 09 |

Mar 09 |

Feb 09 |

|||

| UK MFG | Mar 09 |

Feb 09 |

Jan 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q1- Date |

| MFG | 0.0% | -0.3% | -3.1% | -12.9% | -19.3% | -18.0% | -19.7% | -12.9% | -13.4% | -7.4% |

| Consumer | ||||||||||

| C-Durables | 0.7% | -0.6% | -4.8% | -17.6% | -30.8% | -26.4% | -27.0% | -19.4% | -21.5% | -7.9% |

| C-Non-durables | 0.8% | 0.8% | 0.5% | 9.2% | 3.4% | -0.6% | -4.2% | -3.0% | -4.4% | 9.8% |

| Intermediate | -1.1% | -1.3% | -3.7% | -21.8% | -23.7% | -23.4% | -21.1% | -14.7% | -14.0% | -17.7% |

| Capital | -1.5% | -1.4% | -5.1% | -27.9% | -29.5% | -26.0% | -25.3% | -17.7% | -16.5% | -22.6% |

| Memo: Detail | 1Mo% | 1Mo% | 1Mo% | 3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q1- Date |

| Food Drink&tobacco | 0.7% | 1.3% | 0.8% | 12.1% | 0.0% | -1.0% | -2.6% | -2.5% | -3.5% | 11.9% |

| Textile&Leather | -2.3% | -0.4% | -3.0% | -20.6% | -19.8% | -14.2% | -12.5% | -8.7% | -6.4% | -19.6% |

| Motor Vehicles & trailer | 5.0% | -4.8% | -18.5% | -55.8% | -64.9% | -58.9% | -64.8% | -42.8% | -46.1% | -29.4% |

| Mining and Quarry | -2.4% | -1.3% | -3.3% | -24.8% | -18.1% | -24.7% | -10.0% | -10.7% | -8.5% | -23.5% |

| Electricity, gas&H2O | -2.8% | -3.3% | -0.2% | -22.8% | -12.0% | -12.3% | -9.7% | -9.2% | -6.0% | -26.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief