Global| Jul 02 2021

Global| Jul 02 2021The PPI Soars in the Euro Area... Does It Matter?

Summary

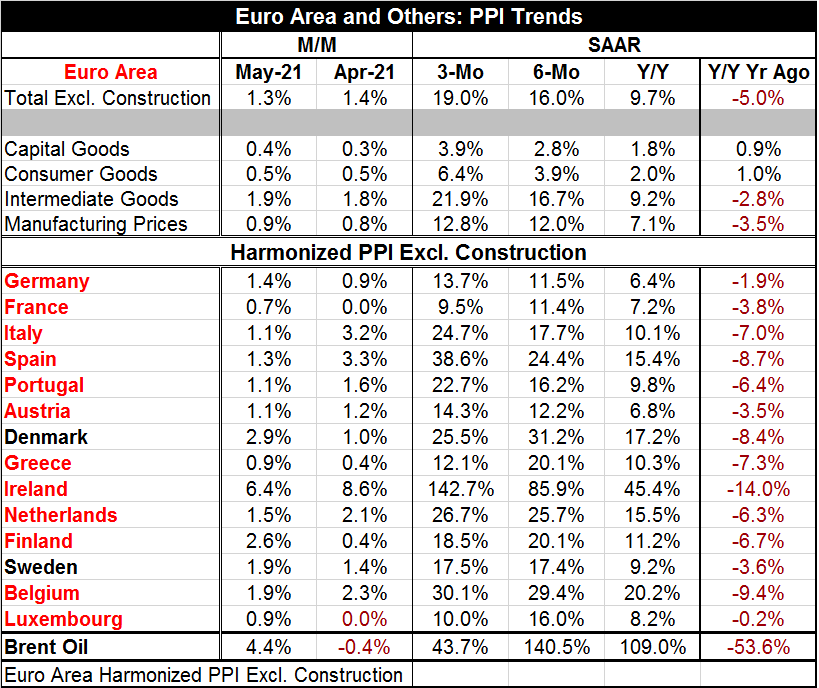

In the euro area, the PPI is making all sorts of noise and rising at a barn-burning pace: 9.7% over 12 months, a pace of 16% over six months and at 19% pace over three months. No rates are remotely in the target range of any central [...]

In the euro area, the PPI is making all sorts of noise and rising at a barn-burning pace: 9.7% over 12 months, a pace of 16% over six months and at 19% pace over three months. No rates are remotely in the target range of any central bank except possibly the Reichsbank after WWI (as if it had any target at all…).

In the euro area, the PPI is making all sorts of noise and rising at a barn-burning pace: 9.7% over 12 months, a pace of 16% over six months and at 19% pace over three months. No rates are remotely in the target range of any central bank except possibly the Reichsbank after WWI (as if it had any target at all…).

While the PPI is running wild and that is uncomfortable, the graph shows that it is much more variable than the HICP that the ECB actually does target. The PPI since 2010 has ranged from its current high year-on-year pace of nearly 10% to a low of -5%. Meanwhile the HIPC has varied from a small negative number (-0.4%) to a pace at about 3% so at the top rate the PPI was more than three times the HICP pace and at the bottom extreme the PPI fell by about 12 times more. Not surprisingly the R-Square correlation between the HICP and the PPI is low, only 0.002, headline-to-headline.

Partly what is going on is that oil prices are driving inflation in the PPI. Manufacturing prices in the PPI have a strong correlation with Brent at 0.81, or an R-Square of 0.66. The bulk of this is through its intermediate goods components but some also is through consumer goods at the producer level. But compare that correlation to the HICP-Brent relationship and the correlation drops to 0.66 and to an R-Square of 0.43. The connection to the HICP-core from Brent is actually tenuous with a correlation of 0.17 and an R-square of 0.03. We can conclude that if this is PPI inflation from oil prices we do not have much to fear from it.

These metrics give us good reason to believe that the PPI is having its goose cooked by oil. Brent prices rose by 4.4% in May and they are rising at a 43.7% annualized rate over three months, a 140.5% annualized rate over six months and by 109% over 12 months. Clearly oil has been pushing a lot of price increase though this system. Just as clearly some of that will get into the headline of the HICP and very little will get into the core rate (that also excludes alcohol and tobacco).

Still, in the aggregate the price hike is disturbing. In May, all countries are seeing a one-month gain in prices of 1% or more except Luxembourg, Greece and France. In April, there were four exceptions to that same rule. Over three months countries post double digit annualized gains everywhere but France. Eight of the increases over three months were at an annualized pace of 20% or more- and Sweden and Finland came close with gains well above a 15% pace. Over six months there also are annualized double-digit gains everywhere. The simple year-on-year increases show eight gains in double digits.

Of course, the year-on-year gain in Brent is 109% and that compares to a -53.6% dropping rate over the previous 12 months. Clearly prices are gyrating. The Covid crises crashed prices and now they are regaining and bulking back up. Oil, in particular, is building gains on the notion that there will be some short-term runaway demand pressures at the same time that alternative oil supplies such as fracking are being restrained by environmental concerns in the U.S.

By sector, we see a much more segmented view of inflation with capital goods prices at the PPI level up by just 1.8% over 12 months and consumer goods prices up by 2%. Intermediate goods prices are up by 9.2%; they are the big inflation transmitter. Meanwhile, manufacturing prices overall are up by 7.1% over 12 months.

Despite the white hot headline on the PPI, its extravagant recent growth rates, and the clear spread across all EMU members, this looks more like an oil and related commodity price shock than anything else. I would not say that the ECB is not worried about it, but even in the presence of all this pressure the HICP headline is just squeezing in under the ECB's mandated target after data revisions this month. There are voices of concern at the ECB. But Christine Lagarde still sees support for growth in the face of a lingering pandemic as job-one. ECB policy is not going to overreact to inflation. The question we seem to be asking more and more across various countries and central banks is the opposite one, however: will policy be too tolerant, of too much inflation, for too long? Policymakers say 'no.' Markets remain in a quandary and from time to time show their skepticism.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief