Global| Oct 09 2014

Global| Oct 09 2014The Other Shoes Fall; German Exports Buckle

Summary

In the game of baseball, there're three strikes and you're out. Fortunately, Germany plays football (soccer), not baseball. Germany has posted weak reports on industrial orders, industrial output and now for exports. This is a triple [...]

In the game of baseball, there're three strikes and you're out. Fortunately, Germany plays football (soccer), not baseball. Germany has posted weak reports on industrial orders, industrial output and now for exports. This is a triple play of bad news. However, the bad news is mitigated somewhat by the fact that the German summer holidays occurred this year in August, instead of July, contributing to and exacerbating the reported slowdown. You can see impact in the chart; exports that boomed in July had busted in August. Still, will have to see the post-holiday numbers to find out how bad the damage is.

In the game of baseball, there're three strikes and you're out. Fortunately, Germany plays football (soccer), not baseball. Germany has posted weak reports on industrial orders, industrial output and now for exports. This is a triple play of bad news. However, the bad news is mitigated somewhat by the fact that the German summer holidays occurred this year in August, instead of July, contributing to and exacerbating the reported slowdown. You can see impact in the chart; exports that boomed in July had busted in August. Still, will have to see the post-holiday numbers to find out how bad the damage is.

German exports to the European Union countries rose by 2%. But German exports to countries outside of Europe fell sharply by 4.7%. Economic sanctions on Russia are a two-edge sword.

German think tanks have also been revising their growth lower. German institutes are looking for growth of 1.3% this year from 1.2% next year, down from a profile of 1.9% for 2014 and 2% for 2015, previously. The IMF has also joined the party to cut its outlook.

Rather than succumbing to pressure us for stimulus both within Germany and from outside, German lawmakers are making it clear that their priority is to fully balance the budget. This also means that Germans are opposing ECB President Mario Draghi and his plan to purchase assets to stimulate the European economy. Germans simply refuse to drink the Kool-Aid, preferring to remain parched.

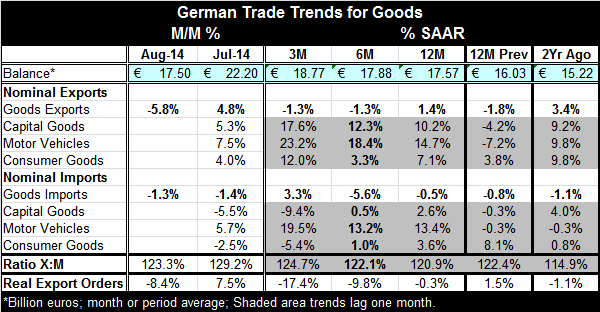

The trends in German exports are clear. In August, exports fell by 5.8% and imports fell by 1.3%. Exports are seeing sequentially weaker growth rates as they both fell by 1.3% at an annual rate over three months and six months, down from 1.4% over 12 months. The growth rates for imports are a little less clear. Despite declines in both August and July, three-month import growth rates are positive at 3.3%, up from -5.6% over six months and -0.5% over 12 months.

Trends for the commodity composition of trade lag by one month as those data are updated only through July. On that basis, there is clear export strength in July when exports boomed because the summer holiday did not occur in July and instead was put off to August. The three-month growth rates for capital goods surged to 17.6% over three months from 12% over six months and 10% over 12 months. Motor vehicle exports surged 23% over three months from 18% over six months and 14% over 12 months. Consumer goods exports boomed at 12% over three months, compared to 3% over six months and 7% over 12 months. The repositioning of a major holiday in Germany is major consequences for its economic numbers. We can see here both the evidence of the boom and of the bust. That leaves us a little bit more quizzical about where German trends are although the weakness in the important orders, output and export series are pronounced enough to suggest that this weakness is real and will linger beyond holiday period.

Imports do not show the same clear pattern of boom over three months with capital goods imports falling by 9.4% at an annual rate compared to gains of 0.5% over six months and 2.6% over 12 months. Motor vehicle imports stepped up to a 19% growth rate over three months from 13% over six months and 13% over 12 months. Consumer goods imports fell by 5.4% over three months after increases of 1% over six months and 3.6% over 12 months. Does this relative weakness in imports signal that German domestic demand has weakened even further?

The ratio of exports to imports falls to 123% in August compared 129% in July. That ratio compares to 120% 12 months ago. At the bottom of the table, for comparison, we show real export orders that busted 8.4% in August after a 7.5% boom in July. They seem to show the holiday effect too. But even with the monthly boom-bust evident, we see that export orders are falling at a 17% annual rate over three months and a 10% pace over six months and by 0.3% over 12 months.

The repositioning of the German holiday complicates our ability to make clear statements about German economic trends. However, the degree of weakness is severe. Since July was boosted by holidays that didn't exist and August was busted by holidays that were not expected to occur, the year-over-year figures should be more or less clear of the seasonal effects. And year-over-year we have exports up only 1.4%, imports down by 0.5% and real export orders off by 0.3%. That's not a definitive way to make the calculations, but it is suggestive. The German economy seems to be slipping on that slippery slope much to the horror of the rest of Europe. German institutes to see growth for the whole of the year, but not much of it, and little enough of it in the second half.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief