Global| Mar 20 2020

Global| Mar 20 2020The German PPI Backs Off After Spike

Summary

Germany's PPI had flared at the very start of the year but now just as suddenly as it rose it is backing off. The PPI that rose by 0.6% in January is now falling by 0.4% for an average increase of 0.1% over each of the last two [...]

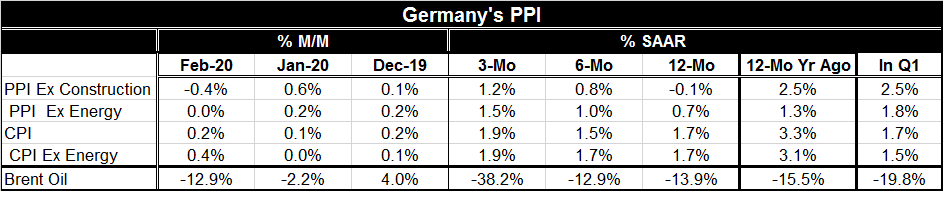

Germany's PPI had flared at the very start of the year but now just as suddenly as it rose it is backing off. The PPI that rose by 0.6% in January is now falling by 0.4% for an average increase of 0.1% over each of the last two months. Still, the charts read this as an inflation blister and the sequential growth rates pop up even though the headline PPI is still falling by 0.1% over 12 months. The PPI ex-energy is on an accelerating profile and it is up by 0.7% over 12 months. Like the headline PPI, the core average rise has been 0.1% per month over the last two months but arrived at differently with a 0.2% gain in January and a flat February. Oil prices, of course, are decaying.

Germany's PPI had flared at the very start of the year but now just as suddenly as it rose it is backing off. The PPI that rose by 0.6% in January is now falling by 0.4% for an average increase of 0.1% over each of the last two months. Still, the charts read this as an inflation blister and the sequential growth rates pop up even though the headline PPI is still falling by 0.1% over 12 months. The PPI ex-energy is on an accelerating profile and it is up by 0.7% over 12 months. Like the headline PPI, the core average rise has been 0.1% per month over the last two months but arrived at differently with a 0.2% gain in January and a flat February. Oil prices, of course, are decaying.

Inflation is still very tame and there is no reason to think that the recent pick up will endure or that the roll off will be temporary. With global oil prices so low and still confronted by global growth set to be weak and weakening for time inflation is hardly an issue. Nonetheless, we will track and it tabs on it – just in case... sleep well on that.

Outlook for Germany

The bigger picture here is not really about inflation that once again seems to be in the process of being put back inside the bottle. The real problem is the outlook for growth and here the DIW institute reported Thursday that Germany, the largest euro area economy, is set to shrink 0.1% in 2020. This prognosis is based on the assumption that Germany will normalize quickly from the crisis situation. However, it may not be so lucky. The IFO institute earlier had forecast the German economy would contact by 1.4% in 2020 but then to spring back with growth of 3.7% the next year. Both of these German research outfits see a solid-to-strong rebound after an economic disruption.

What about stocks?

What is most interesting is that while most economic outfits have the same sort of view on the crisis equity markets ae unwilling to price stocks that way. If you think of stock valuation as being 'all about earnings' then the outlook for earnings should drive valuation. And if a downturn is to be short, even if sharp, there should be a limited impact on share prices. Of course, to get to share prices from earnings, one goes through the P/E ratio which is more or less historically determined; P/Es are different in different sectors and also fluctuate with interest rates and other factors. With interest rates so low, we would expect at least an average P/E to be put on the earnings outlook. Unfortunately, here and now equity markets are so unsure of this disease process that they are unwilling to discount earnings far into the future at all. It is as though markets want to price stocks for this quarter's earnings or next and not beyond. And that sort of seizing up of expectations has left a real chasm between stock valuations and current economic projections.

Stocks should recover, but what about people?

Once confidence returns, we would expect his disconnect to go away. Markets may not go back to their bold valuations of the past, but they should at least put normal values in play. Until that happens, we are all left scratching our heads about economic disconnects. There is also the strangeness of seeing the global economy being shut down by a virus that gives you much the same symptoms as the common cold. It seems odd to try to shut the global economy for a virus that threatens lives in only a small portion of the population instead of trying to specifically protect that portion of the population that is really at risk; the already sick or impaired and the elderly. Italy's shocking numbers show 70% of the deaths are among the very old. The death rate for men is twice that for women. It has the second oldest national population in the world. No wonder it has been hit so hard.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief