Global| Jan 26 2015

Global| Jan 26 2015The Gathering Euro-Storm

Summary

The chart shows the steady march of the German Ifo indices even in the context of the business cycle and its aftermath. There was a large Ifo index drop in recession followed by recovery. There was a second down draft, much milder [...]

The chart shows the steady march of the German Ifo indices even in the context of the business cycle and its aftermath. There was a large Ifo index drop in recession followed by recovery. There was a second down draft, much milder than the first, then a milder recovery. In 2014 there was another setback and now the beginnings of another recovery. Time and the German economy march on cycles and all.

The chart shows the steady march of the German Ifo indices even in the context of the business cycle and its aftermath. There was a large Ifo index drop in recession followed by recovery. There was a second down draft, much milder than the first, then a milder recovery. In 2014 there was another setback and now the beginnings of another recovery. Time and the German economy march on cycles and all.

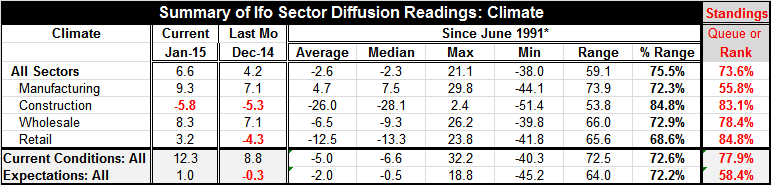

The Ifo story is told by the indices in the graphic and the diffusion measures in the table. Diffusion indices offer an earlier look at the German sectors. Here we find the pleasant news that all sectors, save construction, improved in January compared to December. Current conditions improved, expectations improved and all-sector climate improved. Queue percentile standings by sector range from a very moderate 55.8% standing for manufacturing to a strong 84.8 percentile standing in retailing. The current conditions index at the 77.9 percentile is quite solid while expectations are positive but at their 58.4 percentile, substantially subdued. Expectations have been lagging current conditions in each of the last two mini-cycles.

But Germany is only one country in the EMU and we cannot understand Germany's story without understanding the context of the euro area's condition. Here is where we begin to see troubles and where complications set in. There has also been learning which I believe has affected how members, especially Germany, view the evolving euro-arrangements.

Just last week the European Central Bank sorted out its plan for QE that was so long awaited. There were three main ingredients in this plan: (1) a relatively large QE program compared to expectations, (2) an objective-based program (get inflation heading back to target) that leaves it potentially open-ended, and (3) a shift in risk-bearing from the bond buying operations under QE to the local national central banks from the ECB.

This plan will have and already is having a profound impact on the euro area and Europe. Switzerland, not an EMU member, cut its euro ceiling policy without warning ahead of the ECB action. The Swiss franc moved sharply higher inflicting quite unexpected pain on market participants, even bankrupting some. Denmark, a country which, like the UK, owns a single currency get out of jail free card, continues to exercise that right and run a separate currency and central bank policy. Denmark cut rates twice last week once ahead of the ECB action and once afterward.

The part of the ECB plan that severed risk mutualization paved the way for this morning's fluff-off by markets of the Greek events. Syriza, the anti-bail out party, won a majority and has formed a coalition government that is anti-bailout. European markets hardly flinched. The euro fell then recovered. With risk mutualization ended the Greek plan has the gun pointed squarely at its own head. Greeks could choose to leave the euro area and that would create some chaos since there is no exit plan or procedure. But the ECB action has paved the way for a smoother exit should one occur. The ECB plan loosened euro ties; it did not strengthen them.

Increasingly we have seen Germany become abhorrent over the way things have gone in the EMU. Germany did not expect to see risks boomerang to it since it has been such a good citizen keeping its inflation down and controlling its fiscal deficits. But if you are joined at the hip as all are in the euro area, your brothers' drinking problems affect your liver.

Germany is reaping form the policy it sowed, but did not expect it to turn out this way. The upshot is that one cannot put German conditions on non-Germans and think the consequences will be the same as they would be in Germany. German policy pursued a hardline for all euro area members in the financial crisis after rejecting U.S. entreaties for stimulus. Germany and Europe sought refuge in austerity. And while there is no denying that austerity has brought fiscal progress to Europe, the lack of growth has brought pain and the pain of low growth has made the austerity progress extra-painful. On top of the fiscal hammer, ECB policy has been tighter than promised as the bank lost control of inflation on the downside. In addition, loan demand and money supply growth has reminded weak amid banking problems in Europe. Germany's insistence on EMU-wide austerity has been a significant factor pushing the euro area toward deflation. Germany has been in denial of that and has been against any special policy move every inch of the way- trying to fence off the ECB and protect its balance sheet. That explains why growth is now so weak in the euro area (think euro area excluding Germany), why the euro exchange rate is falling, yet why interest rates are so low- negative across broad bands of the euro area and why QE is being implemented in an environment that may be too hostile for it to do much good. All of this is the result of German engineering- financial engineering.

There has been no balance here. There has been no trade off. Monetary and fiscal policy did not work together. Each separately sought its own special austerity goal with very predictable results. To get a large enough QE plan, Mario Draghi had to give Germany a cessation of risk mutualization. That also has helped to isolate Greece and everyone one else.

What I see in all of this is Germany taking steps after having been surprised that after all its good behavior the end result was that the rest of Europe would find a way to raid Europe's last bastion of wealth and stability, the ECB piggy bank. Germany opposed this and had proposed substantial rules to keep anything like this from happening through the covenants that stablished the ECB. But the economic circumstances have become too dire. Germany would see that it would not be able to prevent the ECB from executing QE so it found a way to insulate it instead. And with that plan European monetary policy comes to resemble the Japanese lunch box that is also European fiscal policy - at least in terms of risk-sharing. Risk sharing at the ECB is gone.

My view is that Germany has had enough. Things have not turned out as it planned. It is ready to see countries bear their own risk and even leave the euro area if they can't keep up. Germany now appreciates the dangers of dragging weak members along and making accommodations for them to stay in the euro rea. The de-mutualization of debt risk leaves countries more at risk to their own QE implementation. The ECB will still direct how much each country is to do on a prorated basis. But my sense is that Germany now can see that bad polices among euro-members can have dire consequences for Germany. Good behavior is not an insulator. Germany is no longer interested in playing that game. Germany is ready for some, the ones that are not ready, to suck it up and exit. The new structure is in place.

This is a very new and serious phase for the euro area. Should Greece exit it would send a message to others about either putting up with the ravages of austerity to stay in or finding a way outside as a non-EMU member. In the financial crisis, Europe came together unprepared as it was for the divisive forces it met. But after seeing the costs and now seeing Greece back for more, I think Europe has entered a new, more dangerous, if more subtle phase of euro area risk. And just as Switzerland went from being 100% committed to one policy one day and changing it the next, I see the EMU as subject to some of these same risk shifts right now primarily over Greece.at least at first.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief