Global| Feb 13 2020

Global| Feb 13 2020The Euro Area Unemployment Rate Drops As Inflation Cruises

Summary

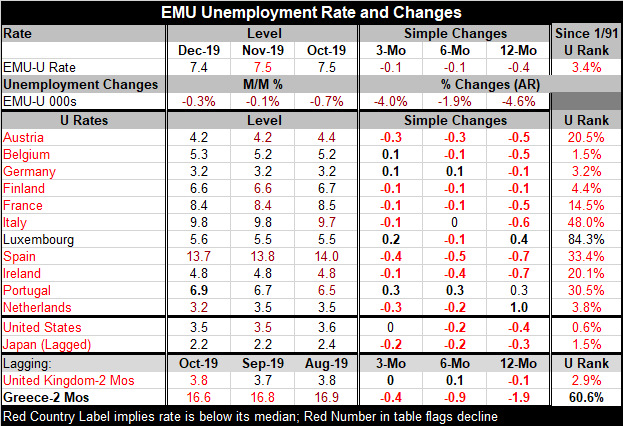

The euro area unemployment has been dropping and is now low by its own historic standard, but the unemployment rate varies considerably across the monetary union. The unemployment rate did tick lower in December as France logged a [...]

The euro area unemployment has been dropping and is now low by its own historic standard, but the unemployment rate varies considerably across the monetary union. The unemployment rate did tick lower in December as France logged a quarterly unemployment rate that was at a decade low.

The euro area unemployment has been dropping and is now low by its own historic standard, but the unemployment rate varies considerably across the monetary union. The unemployment rate did tick lower in December as France logged a quarterly unemployment rate that was at a decade low.

Time for a change?

The chart shows that there has really been no conflict between keeping inflation at target and getting unemployment low since about 2013. For a brief period, while still in the grip of recession and financial crisis, the inflation rate rose and the unemployment rate climbed relentlessly raising the specter of stagflation. But such episodes are not unusual in the wake of recessions and this one, too, proved fleeting. By 2012 the inflation rate was falling, next the unemployment rate peaked and began to fall. From 2013 onward, the EMU unemployment rate has continued to drop and inflation has largely been within and well within the limit sought by the European Central Bank. In fact, as the unemployment has fallen and stayed at what are now low levels, the HICP continues to show inflation at a low pace. And the policy discussion has really turned to asking if such low interest rates as the ones the ECB engineered are useful any more.

The policy complication- one objective

With the EMU-wide unemployment rate at 7.4% a rate that is lower than that only 3.4% of the time since 1991, there is not as much of strong push back against the notion of taking a look at raising rates. However, the impetus is from those in traditionally ‘hard-money' countries this is no ‘grass-roots' movement. Since the ECB has one directive to get inflation just below the 2% mark and since inflation has been well below the 2% mark, the ECB really has no policy reason to do this. The rational comes from those looking at the low structure of rates and arguing that that is unnatural and that low rates are introducing other distortions. They assert that despite low inflation now these low rates are sowing the seeds of trouble for down the road.

And unemployment is low-broadly low

Turning back to ‘the resistance' there is little of that since among the longest-standing members in the EMU (see the table to identify them) unemployment rates are below their medians on data back to 1991. Everywhere except Luxemburg, a financial center, and Greece, have below-median rates unemployment. The median unemployment rate across these countries has a standing of 20.2% which says that it is only lower than its current level 20.2% of the time - roughly one fifth of the time.

The policy complication

However, low unemployment is, there are always arguments to make it lower. As long as inflation is tame, these arguments are powerful; having unemployment higher than it ‘needs to be' has a cost of lost output that can never be recouped. So the unemployment and inflation situation in the EMU presents policy in a dilemma.

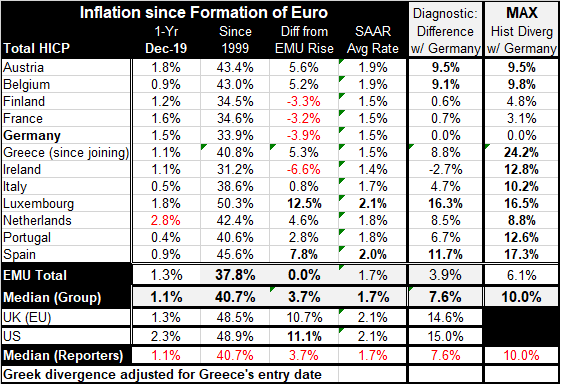

Inflation is and is broadly still well-behaved

If we look at inflation across countries, there is only one country as of December with a year-on-year rate above 2%; i.e., the Netherlands at 2.8%. And the Dutch are tied with the Germans for having the lowest rate of unemployment in the EMU. In Germany, the inflation rate is 1.5%, surpassed only by the Netherlands, Austria, Luxembourg and France. The average unemployment rate in these four countries is 4.8%; skip France and it is at 3.5%. The average percentile standing of those rates is at their 10.5 rank percentile about half the EMU median standing.

A second group consisting of Belgium, Finland, Greece, Ireland, Italy, Portugal and Spain have inflation rates at 1.2% or less. The unweighted average for this group is below 1%. These countries average unemployment rates of 8.3%, much higher than the 4.8% for the higher, but still low, inflation group. And the average unemployment rate standing for this group is at its 28th percentile, a percentile more than double that of the higher inflation group.

The question...

The question is: since inflation is still well below target, since oil prices have eased again, since there is a threat from the coronavirus, is there really any strong reason to act to prevent lower unemployment rates in countries where unemployment might still be reduced without any near-term impact on inflation?

Which is the real risk?

Or is it the case that the longer run fear of interest rates that are too low is the greater risk? Will ‘repositioning rates' at a higher level have a depressing impact on growth in the face of lingering and perhaps growing risks to global growth?

Lagarde's bargain

Christine Lagarde who took up the job to head the ECB did so promising the ‘Hard Money' countries she would take a good look at low and negative interest rates to see if they continue to do any good for growth. So this decision is going to fall squarely in her lap. At the time, she was being considered for the position; this may not have seemed like such a Faustian bargain. In the current environment, is it a bit more politically and economically charged.

The decision variables

Of course, the ECB does not make monetary policy decisions looking at the data I have just cited. It looks at EMU-wide weighted data that have had all links to national trends removed…but those data still exist and continue to tell the story I weave above about political divisiveness.

Can the ECB find a way? Should it?

In the U.S., the Federal Reserve ‘found a way' to raise rates even though it was persistently and chronically below its inflation target. The Fed overshot its sweet spot for rates and had to unwind some of the hikes last year. But the U.S. economy grew better than did Europe at least for a time and the Fed has been quick to act with special programs and lower rates when danger presented itself. That made the Fed's actions more effective and kept the Fed in the end away from the desperation of choosing negative rates.

Learning by doing

Europe acted more slowly in past because of German obstruction and challenges to the legality of what the ECB sought to do. By the time the ECB got the go-ahead, these policies were less effective. There is a lesson there too. One wonders if Europe has learned it?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief