Global| Sep 26 2016

Global| Sep 26 2016Surprise Spurt in Germany's IFO: Should You Believe It?

Summary

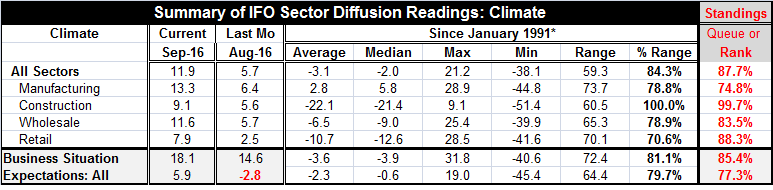

Germany's business expectations in the IFO survey 'flipped' from a reading of -2.8 in August to one of +5.9 in September. This sort of one-month spurt is rare. In fact, the change in the monthly IFO expectations index has been greater [...]

Germany's business expectations in the IFO survey 'flipped' from a reading of -2.8 in August to one of +5.9 in September. This sort of one-month spurt is rare. In fact, the change in the monthly IFO expectations index has been greater only two other times since 1991 over a period of 25 years.

Germany's business expectations in the IFO survey 'flipped' from a reading of -2.8 in August to one of +5.9 in September. This sort of one-month spurt is rare. In fact, the change in the monthly IFO expectations index has been greater only two other times since 1991 over a period of 25 years.

The IFO gain described

The combination of a high reading for the business situation and of improved optimism for the months ahead has been described by IFO President Clemens Fuest as the expectation of a 'golden autumn.'

The current index rose to a two-month high while the expectations index rose to its highest reading in over a year. These kinds of improvements are off the charts when compared to expectations.

However, the IFO survey has representational issues. It may be overstating the degree of strength in the German economy by not putting enough emphasis on the weakening services sector.

The IFO compared

Markit: The IFO reading strength defies a reading from last week on the Markit Indices that was decidedly downbeat. However, the IFO has eliminated its overarching services sector survey although it does still carry sector readings for retailing and wholesaling. In the Markit framework, the services sector was the weakest part of its PMI survey. Manufacturing in the Markit framework rose to an 88% high (on five years of data) while the service sector reading slipped to well below its five-year median to the bottom 14% of its five-year range. That, obviously, created a lot of drag for the Markit composite index.

ZEW: Separately the ZEW 'financial experts' saw for September a weaker current reading and an unchanged and relatively low-ranking expectations index. For the ZEW experts, the IFO reading also will come as a kind of a shock.

The IFO details

Details: The construction sector rose to its highest point since at least January of 1991. The manufacturing reading is stronger than its current level only about 25% of the time. Historic readings on that same timeline find that wholesaling is stronger less than 17% of the time and retailing is stronger only about than 12% of the time. Putting these all together, the all-sector index finds better conditions historically less than 13% of the time. That is impressive.

Relative standings: Despite the surge and the gushing interpretation by the IFO president, this month's data for expectations still only sit in the 77th percentile of their historic queue of data. It's a good, solid 'top 23 percentile' reading but not close to spectacular. The business situation per se is gauged at an 85th percentile standing, one that is better only 15% of the time. That certainly counts as quite strong.

Shock and context: The IFO reading is probably less stellar that it is unexpected. The Markit report did not tip this off and the ZEW financial experts did not see this coming. Of course, there is the 'problem' that the IFO is underrepresented in services where the Markit index was extremely weak. Against that background, we will want to see if these readings hold up next month, especially given the sharp monthly increase in expectations in September.

Some issues in evaluating the IFO signal

Germany still has elections pending about one year off. The EU is still trying to come to grips with Brexit. The EU is looking for its identity. Migrant issues continue to haunt Europe and Germany. Globally, trade and growth remain under pressure. Central banks have pulled so many rabbits out of their hats that they are down to the short hares. After going through a laundry list of factors, it is hard to see where German IFO optimism is springing from. Some characterize the IFO reading as an upper bound on where the German economy really lies. To me, it looks well above the upper bound. The IFO appears to have gone gushing off the tracks with the survey this month. And while it is the survey that directly samples industry members, as ZEW respondents are only financial experts trying to read the tea leaves from a distance, it is the sector weakness in the Markit indices that I find most persuasive. The IFO Index is lacking in its service sector presentation and weighting and that is where the economic weakness is concentrated. That deficiency has led the IFO to overstate the condition of the German economy in September. We will be watching incoming data for signs that economic bifurcation is stalking the German economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief