Global| Mar 12 2015

Global| Mar 12 2015Surprise! Euro Area IP Falls

Summary

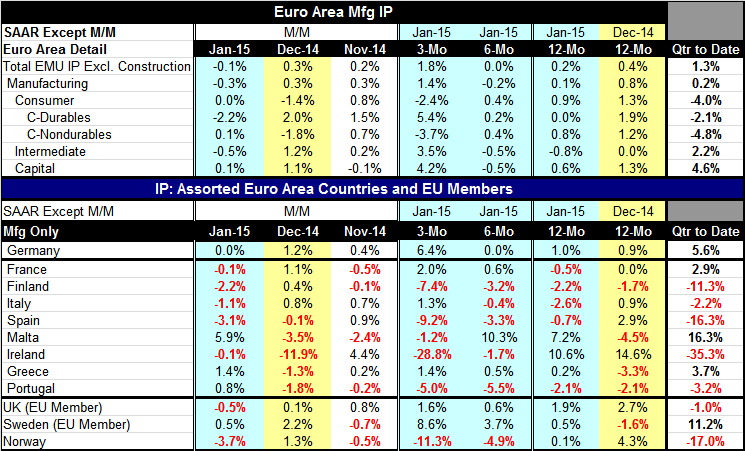

EMU industrial output fell in January by a thin 0.1%. Still, the drop was a surprise. Output in manufacturing fell by 0.3%. Overall output is up by 0.2% over the past year while manufacturing output is up by just 0.1% over the past [...]

EMU industrial output fell in January by a thin 0.1%. Still, the drop was a surprise. Output in manufacturing fell by 0.3%. Overall output is up by 0.2% over the past year while manufacturing output is up by just 0.1% over the past year.

EMU industrial output fell in January by a thin 0.1%. Still, the drop was a surprise. Output in manufacturing fell by 0.3%. Overall output is up by 0.2% over the past year while manufacturing output is up by just 0.1% over the past year.

Despite the unexpected weakness in January the trends for IP have not really soured. Over three months, output is advancing overall by just short of 2% and manufacturing growth is just short of 1.5%. While consumer goods output is falling over three months, the output of intermediate goods and of capital goods is growing at rates of 3.5% to 4.2%, both quite strong rates of growth.

The chart shows that year-over-year growth rates of the three main IP sectors have been on the decline. Year-over-year intermediate good output is actually shrinking. However, over three months, only consumer goods output is shrinking. Yet, over six months output is shrinking for intermediate goods and for capital goods and fast enough to drag overall output lower over six months.

However, the year-over-year trend and six-month weakness notwithstanding the more recent observations are more buoyant, yes even with this latest dip included. Taking the level of output in January as a growth rate over the centered Q4 level, we find overall output is still advancing at a 1.3% pace in Q1, held back by a decline in the output of consumer goods but boosted by solid-to-strong output growth in intermediate goods and in capital goods- two of three sectors.

However, the quarter-to-date output gain is not broadly supported by the country level data. On this horizon, we have output rising in Germany, France, Malta and Greece. That is, output is up in two of the largest countries and in two of the smaller countries. Output is shrinking in Italy, Spain, Portugal and elsewhere. Italy and Spain, of course, are the third and fourth largest EMU economies.

The upshot of this report and its various entrails is that the euro area remains mixed. While some economic reports have been a bit more buoyant, conditions are still on the ebb and flow. The ECB has just begun its QE operation and the announcement effect of this program on the exchange rate is well in gear. Even so Europe is still struggling and some places are doing better than others. We can see it in price data where Germany reported a 0.1% increase in its CPI on a year-over-year basis. But France, having a weaker economy, is still seeing its CPI fall by 0.3% year-over-year. Just because QE is in gear we should not expect the economic data in the euro area to harmonize any time soon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief