Global| Oct 07 2020

Global| Oct 07 2020Surprise Drop in German IP; MFG PMI Outruns IP Itself

Summary

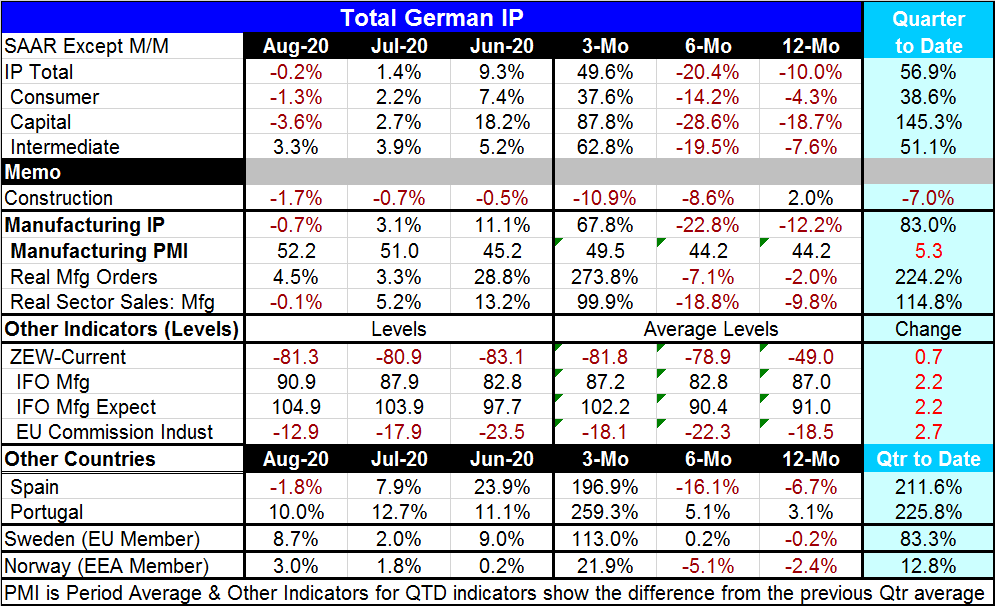

German manufacturing is stumbling according to the August industrial production report and that is very different from the PMI survey from Markit that says output is advancing nicely. According to Markit, manufacturing diffusion is [...]

German manufacturing is stumbling according to the August industrial production report and that is very different from the PMI survey from Markit that says output is advancing nicely.

According to Markit, manufacturing diffusion is higher by 4.2 points than it was in February the last month before the virus began to seriously disrupt Germany and Europe. But compared to its February level, manufacturing output is lower than its February level by 12.1%. This is a serious disconnect of difference.

However, not everything disconnects...

The IP report remains closely tied to the data on real sector sales (presented yesterday along with the German orders data; see here). So what we seem to have is a difference between count-'em-up old-style accounting reports and the diffusion data that are so popular, sensitive and timely but less accurate.

Diffusion data measure the breadth of a trend not its strength. Strength can also be thought of as breadth weighted by size- two measures of size. One of them measuring the size of the monthly change (such as percentage change- not just toting it as 'up' or 'down') the second relates to the relative importance of that gain: how big of a gain for how important of a company? What the diffusion data lack are the two 'size' weights and that loss can be significant. So what is happening is either more small firms doing well and larger firms doing worse or there are a lot of very small increases in activity that boost 'diffusion' a lot more than they boost output. Unfortunately, we just can't tell exactly what it is. But breadth is not strength even though the two concepts are correlated.

What we are seeing is either relatively broad based but small increases that are probably being offset by some substantial weakness at some larger firms accounting for why overall output gains are still so weak. We know that some sectors of the economy are still shut down or partly impaired.

The German data show that even diffusion surveys of current activity are still weak. The IFO manufacturing gauge, for example, rose to 90.9 in August from 87.9 in July, but it is still 1.8 points below its February level. But the IFO expectations gauge for manufacturing also rose to 104.9 in August from 103.9 in July and it is some 11 points above its February level. Surveys that have forward-looking components are much stronger than IP and real sales gauges that are only about what is selling or being produced here and now, not about expectations.

In manufacturing in August, only intermediate goods output expanded. Consumer goods and capital goods output both contracted. All sectors show output declines over 12 months and six months with large annualized again in place over three months The only exception to this is the construction sector that saw output fall for three months in a row, has an output gain over 12 months but slows steadily from 12-months to six-months to three-months.

Output is also jumping out of its own skin in the quarter-to-date in each sector except construction.

Several other early-reporting European countries have issued IP data for August. Spain alone shows an August drop while Portugal, Sweden and Norway log monthly increases. Portugal and Sweden show gradually increasing output from 12 months to six months with an explosion of output over three months. Norway and Spain show declines in output over 12 months with a worsening decline over six months then an explosion in output over three months. All four countries show sharp gains in output in the unfolding quarter-to-date but only Norway reports out a more normal-sized number (but still strong number) without output up at a 12% annualized rate.

On balance, all of Europe got the virus and everyone's data seem to reflect the same sorts of patterns for recovery after accounting for some clear idiosyncrasies by nation. However, the past has been determined but policy toward the virus and so will the future. Just yesterday WHO warned about another spread of the virus impacting the global economy. Countries are handing this reflux or second wave with limited shutdowns instead of across the board shutdowns. Those shutdowns will be adversely impacting growth as well just not as dramatically.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief