Global| Sep 04 2015

Global| Sep 04 2015Suddenly German Order Trends Do Not Look So Good

Summary

German orders fell sharply by 1.4% in July, backtracking on most of the gain made in June. The June gain was made on the back of strong foreign orders; similarly, the July drop is on the back of an outsized drop in foreign orders. [...]

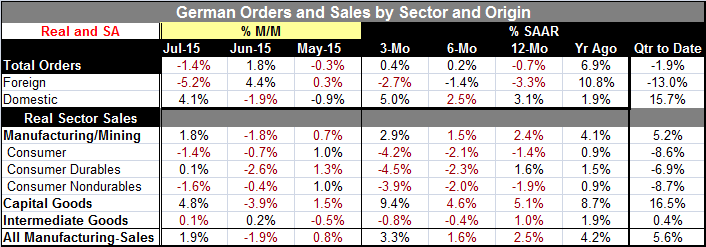

German orders fell sharply by 1.4% in July, backtracking on most of the gain made in June. The June gain was made on the back of strong foreign orders; similarly, the July drop is on the back of an outsized drop in foreign orders. Foreign orders fell by 5.2% in July after spiking up by 4.4% in June.

German orders fell sharply by 1.4% in July, backtracking on most of the gain made in June. The June gain was made on the back of strong foreign orders; similarly, the July drop is on the back of an outsized drop in foreign orders. Foreign orders fell by 5.2% in July after spiking up by 4.4% in June.

The good news in July is the sizable 4.1% gain in domestic orders. This gain follows a 1.9% drop in June and a three-month string of declines. Both domestic and foreign orders have been extremely volatile. However, domestic order volatility has been rising steadily from a low in early 2012. Volatility makes it harder to identify trend.

Sales trends show that consumer goods sales are getting progressively weaker. Capital goods sales are picking up momentum. Intermediate goods sales are weakening.

In late 2014 it looked like German foreign orders were withering, but in 2015 they spiked higher. Now with the unwinding of the July gain, the trend for foreign orders is unclear.

Domestic orders were volatile and weak in 2014. But now in 2015 they show signs of making consistent year-over-year gains.

Within Germany the retailing sector has emerged as one of the relatively strongest sectors bolstered by strong consumer confidence. This may be help to revive domestic factory orders except that so far consumer goods sales do not show it. German consumer goods factory sales are weakening, not strengthening. Internationally Germany has had to deal with weak global growth, sanctions on Russia, and weakness within the euro area itself. Even with the ongoing weakness in the euro exchange rate, German foreign orders are failing to make consistent gains. Order growth is clearly weaker than it was in 2013. With the volatility, it is hard to say exactly what strength will be like in 2015 even though the year is better than half way through.

The recent PMI data from Markit showed a surge in German manufacturing and services in August. It is possible that conditions are starting to ramp up after an extended period of weakness and repeated adjustments to various shocks. But it is still a weak growth environment. It would not be surprising for German industry to find that its best customers are Germans. The EMU has yet to see what will come of the Greek elections and to deal with it. And now there is a growing problem with migrants seeking a place of refuge and a new home. The UN has admonished the EU to take in 200,000 of these. In Germany, Angel Merkel's popularity has been eroding because of her handling of the migrant crisis.

It has been a difficult year for Europe as it struggled with Greece. Although German data continue to reveal it as the solid economy of Europe, Germany too has been underperforming at least by its own usual standards. Now the global turbulence stemming from uncertainty about China adds to the uncertainty about the actions of Federal Reserve in the U.S. The prospects for growth in developing economies have been unseated, given the highly uncertain outlook for oil and commodity prices that their economics depend upon. I would like to say that the worst is behind us as far as uncertainty is concerned. But I don't think I can make a strong case for that statement.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief