Global| Feb 03 2015

Global| Feb 03 2015Stand By Your Deflation: D-E-F-L-A-T-I-O-N

Summary

Denial is not a viable option with which to fight deflation. I'm not saying that the euro area has a deflation problem, but of the 60 evaluations at the country level for monthly and sequential growth rates, only SIX are positive [...]

Denial is not a viable option with which to fight deflation. I'm not saying that the euro area has a deflation problem, but of the 60 evaluations at the country level for monthly and sequential growth rates, only SIX are positive values. And FOUR of those are for the year-over-year calculation from ONE-YEAR-AGO. So I report, you decide.

Denial is not a viable option with which to fight deflation. I'm not saying that the euro area has a deflation problem, but of the 60 evaluations at the country level for monthly and sequential growth rates, only SIX are positive values. And FOUR of those are for the year-over-year calculation from ONE-YEAR-AGO. So I report, you decide.

To gauge deflation we typically would like to look at a broader price measure that contains the services sector was well. And energy is having an outsized impact on inflation results especially in the PPI space. But there is no denying what is happening to prices. And at the consumer level, group of countries is seeing year-over-year declines too. And that process is just starting.

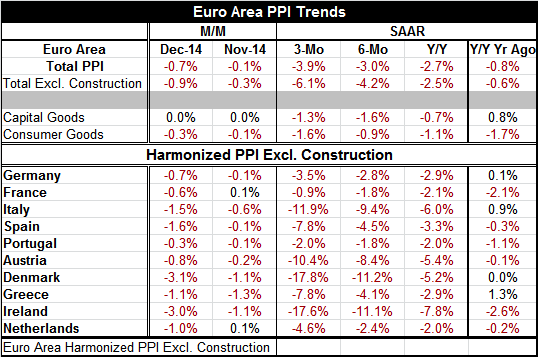

Over three months, the annual rate of price drops ranges from -17.8% in Denmark and -17.6% in Ireland to -0.9% in France and -2% in Portugal.

Over six months, annualized rate declines range from -11.2% in Denmark and -11.1% in Ireland to rates of -1.8% in France and in Portugal.

Over 12 months, prices are lower by 7.8% in Ireland and by 6% in Italy. Prices are lower by 2% in Portugal and in the Netherlands.

There is a large gap between the various inflation rates among EMU members. This is the enduring problems of a one-size-fits-none monetary policy. But inflation's accelerating drop is a reality in eight of 11 countries in the table as well as for the euro area as a whole- that does give them some commonality for policy.

Capital goods prices have been somewhat more insulated from price drops partly because oil is not a direct output (or as key an input) of this sector. Although oil-drilling equipment would be rather directly affecting, as well as the making of pipes for pipelines, for example, capital goods prices are still falling on all horizons but are not steadily decelerating (by a slight margin). Consumer goods are not in a steady state deceleration either owing to a drop over six months that is slightly less than the drop over 12 months. Still, over three months, prices are falling at a faster pace than over either six months or 12 months. And over 12 months, consumer prices are down and they are down on that basis 12 months ago- net lower over 24 months. That is also true pf PPI prices in France, Spain, Portugal, Austria, Ireland and the Netherlands. That's 24 months of PPI deflation.

Fixing Deflation: Any way you slice there is a lot of PPI weakness in the EMU. How do you deal with this problem in practice? Typically, a central bank would either target a drop in interest rates or a speed up in money growth or a nation would adopt some other pro-growth policy to push GDP higher and close the GDP gap to hike prices. Central banks might also use communication policies to signal that they intend to get act to get prices rising again. In the EMU region, Mario Draghi already has thrown down the gauntlet, promising to do `whatever it takes.' That sounds impressive, but his tool kit is mostly empty so he has pulled the arrow out of his quiver, one called QE. Unfortunately, markets can see all that, and the words ring mostly hollow as a result.

The Harm of Deflation: Price drops distort the spend/save behavior of participants because they help to lower interest rates the bridge between current and future consumption/spending. When prices are falling, there can be a tendency to slow spending since things are always getting cheaper. When there is inflation, the incentive is the opposite to buy now before prices get higher. The dynamics of the economy are different in different inflation regimes and `how different' depends on how much people buy-into or extrapolate the trend du dour.

Meet Fred Deutsche Flintstone: The basis PPI in the EMU is falling at a 3.9% pace at an annual rate over three months and by 2.7% year-over-year. Dropping energy prices are driving these results but so is economic weakness. In such an environment, it will be harder for the ECB to stimulate buying with a monetary regime based on QE. Based on the PPI, even the negative real interest rates in the euro area are positive in real terms! And interest rate moves are doing all sort of crazy things. Today, the Germany 10-year yield fell below the Japanese 10-year yield for the first time EVER- I think that includes prehistoric times.

No Two Deflations Are the Same: Markets have rarely seen such uniform price weakness in this region. The financial crisis spread of deflation was worse for a period of about nine months. There was another episode in 2008 when the breadth of deflation in the PPI rivaled this period's. But we don't yet know how long this is going to go on; while the drop in the price level is not as bad as in the recession, it is more extended. Overall prices dropped much more severely in the financial crisis for the EMU as a whole. And the breadth of that decline across this set of countries was at 100% for eight consecutive months. At that time, the financial crisis was doing the job and it was a terrible experience coupled with economic implosion and financial meltdown. In contrast, now, falling oil prices comingle with some weak-but not devastating economic circumstances- that might make the deflation less problematic since most will be looking for the drop in oil prices to abate and -depending how far it goes- perhaps to reverse to some extent.

But to admit that deflation has been worse is not to defeat it. One problem this time around is that all the best fiscal and monetary moves have been exhausted. While the deflation is not as voracious and while it has a special focal point, authorities are less able to fight it off. It's like a second forest fire with the water gone from the fire truck.

QE's Best Channels Are Clogged: It may be that the most potent weapon will be QE at least in its impact through the exchange rate if not on asset prices. Zero inflation - or outright deflation- will hurt corporate earnings, but it will make competition from the bond market nonexistent. A weaker euro FX rate will stimulate corporate output and help to put some juice back into prices while stimulating corporate sales. But that channel remains clogged the downbeat global environment. Supply is still in excess and demand is still only crawling ahead.

Debt the San Quentin of Monetary Policy: In many places fiscal policy is still in a neutral or contractionary phase. Debt levels and leverage both private and public are high and let's remember that deflation LOWERS the optimal level of debt. While people keep reducing debt levels- and they are lower relative to income- the lower inflation is, the lower that consumers will want that debt ratio: it is a moving target and one that makes deflation a tougher trap to escape.

Spanky and Our Gang: the Dead-End Policy: On balance, deflation is a huge issue and problem for Europe as well as in the United States. Banking sector issues in Europe along with the dominance of universal banks in Europe make its dilemma worse. The ECB with one hand is preaching and beckoning for stimulus and QE while spanking the banks to raise more capital with the other - so much for on one hand and on the other. Europe has not just a policy dilemma but confusion and weapon depletion. Looking at the PPI may exaggerate the state of deflation in Europe. But that view does isolate and focus on the view from the corporate side. CPI/HIPC deflation is still a force to reckon with and it is just getting going. And oil prices are not on a trend rise yet so, as bad as they are, deflation's trends are destined to get worse before they get better. It is not a pretty picture. Markets do yet seem to grasp how difficult this is going to be. I judge them as under-reacting. Let me just add that when the U.S. used QE it started earlier and implemented host of supporting programs to try to make QE more effective. Europe does not have that option and it started QE with rates so low and banking problems severe enough that the ECB has the red light and the green on at the same time clearly impeding progress if not helping to introduce chaos.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief