Global| Nov 29 2013

Global| Nov 29 2013Spain Shows Europe Is Headed for Its 'Put Up or Shut Up' Moment

Summary

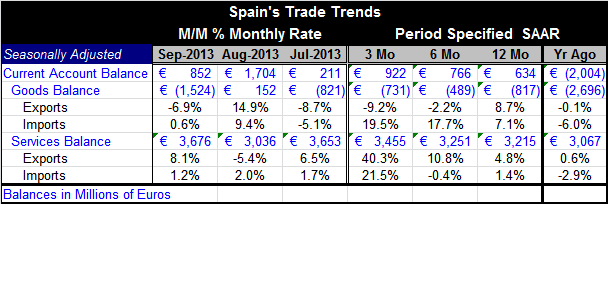

Spain's current account surplus fell back sharply in September, perhaps signally that the end is coming for Spain's current account surpluses. Monthly export growth in September is unwinding about half of the surge in August. But the [...]

Spain's current account surplus fell back sharply in September, perhaps signally that the end is coming for Spain's current account surpluses. Monthly export growth in September is unwinding about half of the surge in August. But the August export surge was only a rebound from a very sharp drop in July. Over three months exports are still falling at 9.2% annual rate. Spain's data are often quite volatile, but the trends are still telling. and they are turning.

Spain's current account surplus fell back sharply in September, perhaps signally that the end is coming for Spain's current account surpluses. Monthly export growth in September is unwinding about half of the surge in August. But the August export surge was only a rebound from a very sharp drop in July. Over three months exports are still falling at 9.2% annual rate. Spain's data are often quite volatile, but the trends are still telling. and they are turning.

Spain's imports are `somewhat' better-behaved as they rose by 0.6% in September after rising by 9.4% in August and dropping by 5.1% in July. Imports are still very volatile even if they are not as raw as exports. Over three months imports are up at a 19% annual rate.

Over 12 months Spain's export growth exceeds import growth 8.7% to 7.1%. Hence the current account deficit has shrunk. But over three months and six months, imports are surging ahead much faster than exports and a deficit reduction deal-breaker.

Over three months and six months Spain's exports are contracting. Over three months and six months imports are expanding at annual rates of growth near to 20%. For Spain the worm has turned. Its external accounts are not improving anymore. They are deteriorating; and with that there will be a great deal of arguing about what the period of austerity really accomplished for Spain.

During the period of austerity, Spain's imports were held down and have mostly contracted since late 2011 (annual growth rates). Exports exhibit mostly positive growth rates (though erratic ones) since early 2012. These two factors led to a correction in Spain's current account deficit which turned to surplus. Spain's current account has been in surplus for 9 of the last 11 months. This month the surplus is still in place, but it has eroded. Given the differences in export and import growth rates over the last half year, Spain is about to enter a period in which its surplus will erode and turn to deficit. That will generate some fireworks in the euro zone as other Southern European nations follow in step.

Trouble Ahead

This is going to be a difficult period for the euro zone as it realizes that austerity is a flow-policy in terms of its effects. That means that many of the alleged `benefits' that were realized during the period of austerity are there only when austerity is in force and when austerity is abolished the economy goes back to its old ways. In this case current account deficits will re-appear. It will be clear that all austerity did was to depress domestic demand and spur productivity.

To find that austerity was not an investment project and that most of the benefit from austerity came from suspending trends that will now go back in force instead of shifting those trends will come as a sharp slap in the face or a blow to the gut for those who have suffered personally in the name of a national investment in the future - an investment that simply will never payoff.

Perhaps in some sectors austerity will have more of lasting impact- perhaps government. But much of the austerity progress on trade was simply because of depriving people of income through higher taxes to reduce the budget deficit and because of slower growth in income so they could not consume as much and would not import as much. In taking the foot off the patient's throat, we will see that he goes back to the old way of breathing.

The Germans will be particularly disgruntled with the failure of their austerity policy. But any policy to fix the problems in the countries of Southern Europe will require more structural efforts and not simply macroeconomic squeezing. Macro-squeezing is not only ineffective but it produces hugely dangerous side effects in terms of political repercussions. We have seen this most starkly in Greece.

Whether Europe will be able to overcome these problems will be the question for the future. The euro zone managed to stay together despite the huge pressures of the financial crisis and its aftermath. But with austerity discredited (except perhaps in Germany- and possibly in the UK) what will be `Plan B' for euro zone?

As austerity countries emerge from their recession/crisis/austerity-induced stupors and begin to grow, domestic demand will heat up. Since not much has been done to close the competitiveness gap with Germany, imports again will surge. A further problem is that the euro itself is relatively strong meaning that only `the most competitive countries in EMU' will be relatively competitive in trade with the rest of the world. Within EMU competiveness differential are locked in for now and can change only slowly or more rapidly with draconian methods as austerity has taught us. So exports from the euro zone's most needy countries will be hit the hardest. And all this will happen at a time that domestic demand (imports!) will be advancing, especially in the countries of Southern Europe where there is so much catch-up to do.

The chart on PPP shows that the euro is well above is calculated parity (at 100) by over 20%. The weighted `real SYNTHETIC effective euro' is above its average value since 1980 by over 20%. This is a `purchasing power parity' (PPP) argument. We apply it over a broad period (before and after euro formation) to a core of euro members using the argument that the market gets the exchange rate `right' over the long term. That means that the average (100 on this chart) is a measure of `parity.' This is `real' concept (`real' means exchange rate adjusted and `effective' refers to the weight applied to bilateral exchange rates that are set by trade relevance). Applying it to values `before' and `after' the euro formation period should not make much difference. If the introduction of euro has created some great euro-synergy, this procedure might not work- but I think few would hold that such a thing has happened. Many may have hoped for it. But they are mostly likely disappointed by now or are incurable optimists.

The chart on PPP shows that the euro is well above is calculated parity (at 100) by over 20%. The weighted `real SYNTHETIC effective euro' is above its average value since 1980 by over 20%. This is a `purchasing power parity' (PPP) argument. We apply it over a broad period (before and after euro formation) to a core of euro members using the argument that the market gets the exchange rate `right' over the long term. That means that the average (100 on this chart) is a measure of `parity.' This is `real' concept (`real' means exchange rate adjusted and `effective' refers to the weight applied to bilateral exchange rates that are set by trade relevance). Applying it to values `before' and `after' the euro formation period should not make much difference. If the introduction of euro has created some great euro-synergy, this procedure might not work- but I think few would hold that such a thing has happened. Many may have hoped for it. But they are mostly likely disappointed by now or are incurable optimists.

Inside the PPP dilemma

Since the introduction of the euro, Greece's CPI (HICP) is up by almost 18% points more than Germany's. For Spain the comparison shows an excessive prices rise of nearly 17% in comparison with Germany. In comparison with the EMU metric for CPI prices (HICP) Germany's price rise since euro zone formation is nearly 6% lower, while Greece is about 12% higher and Spain 10% higher. Only Finland, France, Germany and Ireland have prices rising by less than the EMU weighted-average. So for them competitiveness is better than what is shown in the EMU PPP chart. For the rest of EMU -all the austerity countries especially - their competiveness vis-a-vis the rest the world is even at a greater disadvantage than the 22.5% shown in the PPP chart. Spain's disadvantage is on the order of 32.5%; by comparison Germany's is only 16.8%.

These metrics have `made some progress because of austerity.' Germany's inflation gap in EMU used to be even greater, but progress has made under austerity by deflation. That can't persist. The question now is how much domestic demand will overshoot in the former austerity countries as growth picks-up. What will happen to local inflation vis-a-vis the EMU metric and Germany's outcome, with Germany as the most competitive country in the region?

What to watch in EMU

These are the things to watch: trade performance and inflation differentials. If these metrics show persisting divergence or if divergence on these metrics worsens, then Europe's integration potential will be eroding. Europe must get its fundamentals in line or provide a fiscal transfer system to enable divergences to endure. Failing in those efforts, it would have to split up. In frank terms, we can call it put up or shut up. Europe is headed for its `put up or shut up' moment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief