Global| Aug 21 2019

Global| Aug 21 2019Spain's Trade Deficit Shrinks As Global Growth Sputters

Summary

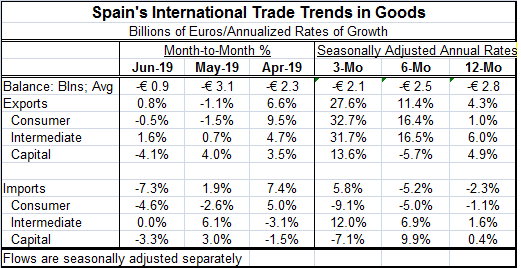

Spain's trade deficit on goods transactions fell into a smaller deficit in June at -0.9 billion euros compared to -3.1 billion euros in June. Exports have had a pick-up in recent months while imports have languished and advanced at a [...]

Spain's trade deficit on goods transactions fell into a smaller deficit in June at -0.9 billion euros compared to -3.1 billion euros in June. Exports have had a pick-up in recent months while imports have languished and advanced at a slower pace. However, in broad trends both export and imports are heading on downtrends and Spanish industry is in a declining phase for activity as well, like the rest of Europe.

Spain's trade deficit on goods transactions fell into a smaller deficit in June at -0.9 billion euros compared to -3.1 billion euros in June. Exports have had a pick-up in recent months while imports have languished and advanced at a slower pace. However, in broad trends both export and imports are heading on downtrends and Spanish industry is in a declining phase for activity as well, like the rest of Europe.

Retail sales in Spain have held up relatively better than other domestic measures, but Spanish GDP led by manufacturing continues to point to a slowdown. These are the trends that ultimately dictate what is happening with imports.

On the export front, Spain exports into the same global economy as everyone else. And that economy increasingly is troubled. But Spain's exports do not carry the economy. Tourism is Spain's largest industry and that sector also depends on the state of the global economy. Since Spain tends to attract a lot of visitors from the U.K., what happens on Brexit could be very important to the Spanish tourist industry.

Spain's consumer goods exports are up by only 1% over 12 months. Imports of consumer goods are down by 1.1% over 12 months. Spain's exports are growing based largely on the expansion of intermediate goods and capital goods shipments. On the import side, intermediate and capital goods imports are anemic with capital goods imports up by less than 1% over 12 months. It's a global phenomenon that capital investment is simply drying up and slowing down.

There are clouds on the horizon. A gathering storm for the economy, perhaps. The tell-tale signs for the U.S. show an inverted yield curve that has very accurately foretold recession, but that curve is now thought to be distorted and wrong. No one wants to believe the signals (I am an exception). Also in the U.S., the President and his advisors have, out of one side of their mouths, decried the possibility of recession. And out of the other side, they are whispering about some new temporary tax cut to boost the economy …the same one that has no recession risk?

The Germans just sold an original issue zero coupon negative yielding 30-year security. Really! I'm not making it up. I can understand short-term rates at a discount to zero temporarily, but I do not for a moment fathom how long-term paper can be negative yielding. Who really believes that this makes sense? Are we going to see persistent protracted long-term deflation? How can a 30-year Bund have a negative yield and that make sense? Is the euro economy in such bad shape or have some deluded individual investors simply lost their minds?

Spain's trend picture is not that dire as to explain the sort of things that we see going on in financial markets from Frankfurt to London to New York to Tokyo. Something is very distorted out there. Maybe that impact is yet to come to Spanish trade flows. Certainly, central bankers are carrying too much of the burden of keeping the global economy aloft. But in the midst of the very low inflation times, we have the Germans rejecting the needs of the moment all by running a budget surplus. We have Maastricht rules constraining debt-financed stimulus in Europe generally. And not surprisingly, as a counterpoint, we have MMT (Modern Monetary Theory) telling us to spend freely, and to use debt. Debt is good if it is used well. Well, which is it? Is it good or is it bad?

In time policy, will go one way or the other and we may find out in the great experiment of life. But for now, globally economies are slowing. Trade flows are slowing. The hatches are being battened down; investment is drying up. It will surprise me if this process does not terminate in a recession because that is the only logical consequence of these actions unless trade negotiators come to their senses quite quickly and provide an unexpected jolt. And while that could happen without notice, it does not seem likely.

All that explains the lurch to zero and negative rates and also the fact that, even in the U.S. where the Fed fuds rate is above 2% all the treasury paper for on-the-run securities have a yield below the Fed fund's rate... even after a rate cut. In fact, after the Fed's rate cut, the yield curve became more broadly inverted. Clearly, the Fed has not yet gotten the message. When it does, it will undoubtedly be too late. The ECB and the BOJ have much less ammunition to expend than the Fed. Mark Carney has put a limit on his arsenal saying that negative rates are not right for the U.K. We have lots of limitations and no one with any flexibility saying that they will do whatever it takes.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief