Global| May 05 2017

Global| May 05 2017Spain's Industrial Output Stays on a Strong Growth Path

Summary

Today I feature Spain's industrial output. It is the Cinco de Mayo which is a Mexican, not a Spanish, holiday (lo siento mucho!-loosely translated that's 'sorry about that'). The holiday commemorates a Mexican victory over the French [...]

Today I feature Spain's industrial output. It is the Cinco de Mayo which is a Mexican, not a Spanish, holiday (lo siento mucho!-loosely translated that's 'sorry about that'). The holiday commemorates a Mexican victory over the French who outnumbered them (and who have elections scheduled this weekend). So there is a Cinco de Mayo connection buried here somewhere but perhaps not the one you expected. Still, it does call for music and a margarita! (some dance to remember some dance to forget- Hotel California).

Today I feature Spain's industrial output. It is the Cinco de Mayo which is a Mexican, not a Spanish, holiday (lo siento mucho!-loosely translated that's 'sorry about that'). The holiday commemorates a Mexican victory over the French who outnumbered them (and who have elections scheduled this weekend). So there is a Cinco de Mayo connection buried here somewhere but perhaps not the one you expected. Still, it does call for music and a margarita! (some dance to remember some dance to forget- Hotel California).

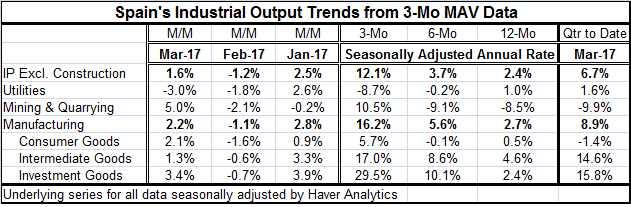

The table and the chart feature smoothed Spanish data based on underlying series that are seasonally adjusted by Haver Analytics. However, even the seasonally adjusted Spanish data are so volatile that I present all the results in the table and in the chart based on three-month moving averages. The 1.6% March gain is the gain in the trailing March three-month moving average compared to the trailing February three-month moving average and so on for all the other calculations in the table.

This MAV (moving average) presentation imparts a bit more stability to the data and to the picture which would otherwise take a very choppy character and shift wildly from month-to-month. Instead, we get the nice stable picture in the chart above that shows IP making small but solid and consistent gains in 2017.

Smoothed vs. unsmoothed data

Spain's seasonally adjusted but unsmoothed data (not shown here) show IP excluding construction gains at 4.4% in March after falling by 3.4% in February and rising by 4% in January. These are month-to-month figures that some countries would die to have as their 12-month change results (except for the declines, of course). In contrast, the smoothed data (in the table below) show a March gain of 1.6% following a 1.2% decline in February and a 2.5% gain in January. You get the same patterns but with less volatility (although that will not always be the case). The bigger deal is that smoothing also stabilizes the year-on-year trends which otherwise hop around a lot. The unsmoothed IP series has a standard deviation of 3.9% on its year-over-year percentage changes over the last 12 months. Compare this to a standard deviation of 1.5% for smoothed data. There is no comparison. So we will proceed to speak of the smoothed data and try to remove much of the volatility from the conversation.

Smoothed output trends

Smoothed IP less construction still shows powerful acceleration to a 12.1% annual rate over three months from a 3.7% pace over six months and a 2.4% pace over 12 months. Manufacturing shows a similar sequential acceleration. Intermediate goods and investment goods show sequential accelerations as well. The exception is consumer goods where output has a barebones 0.5% growth over 12 months that slips to a modest decline at a -0.1% pace over six months then accelerates to 5.7% gain over three months. Even though it not formally pattern of acceleration, it is still a clear trend to improvement with a very small sidestep along the way.

Quarter-to-date: smoothed pattern

With the first quarter now complete, the quarter-to-date shows a gain based on smoothed data at 6.7% pace with manufacturing up by a much stronger 8.9% pace. Both intermediate and investment goods explode at annualized quarterly gains at about a 15% pace while consumer goods output contracts at a 1.4% annual rate in the quarter.

Recovering is spreading but still with limitations

Spain is not being pulled into recovery by the consumer. The investment goods sector is leading. Yet, in the PMI framework the services sector is performing relatively better than manufacturing overall. And the upshot of that is the Spain's labor market has been improving dramatically although the unemployment rate is still in double digits at 18.2%. Among EMU members, Spain's unemployment rate has the second fastest drop over 12 months, falling by 2.1 percentage points which is only barely bested by neighbor Portugal where the 12-month change is -2.2 percentage points. Over two years, Spain's unemployment rate has fallen by 4.8 percentage points, compared to a drop of 3.4 percentage points by Portugal.

Progress despite divergence

Spain has seen a lot of progress. But it is a country with a structurally high unemployment rate. Despite its progress, it still has a long way to go. Germany, whose unemployment rate is at a post-unification low, has seen its unemployment rate fall by only 0.4 percentage points over 12 months and by 0.8 percentage points over 24 months. These sorts of divergences also bring tensions to euro area policymaking.

Assessing Spain's recovery position

Spain's trend line on its manufacturing PMI is nearly dead-flat from March 2015 onward despite some recent revival. The services trend for the same period is showing decay despite recent and stronger revival. Services in the last two months have their strongest reading since August 2015. Compared to the first half of 2014 and earlier, the Spanish manufacturing and services sectors are doing much better. But compared to the environment that has existed since Q1 2015, Spain seems to be more or less unchanged. Now that's nothing to turn your nose up at since Spain's unemployment rate has dropped sharply during this period, as we chronicled above. However, despite this progress, firm PMI gauges and the strong rise in industrial output, Spanish retail sales volume growth has returned to nearly nil after 27 months of very solid-to-strong gains. Over the last three months, Spain's retail sales volumes have increased year-over-year by less than 1% in each month. Recovery remains incomplete.

Ahead...

While Spain has logged a lot of progress and so has much of the euro area. At the end of the day, there are always one or two things missing from what it would take to make recovery a complete package. Just as Germany is skating on the edge of economic excess, so are many other EMU countries showing a good deal of progress but with still a long way to go. This divergence and its contrasting demands will continue to dominate the European policy discussion right along with the focus on Brexit and what it means. On the way out, everybody seems to want a piece of the U.K. Today George Junker bad-mouthed the use and need for the English language and presented his remarks in French. Spain is seeking the return of Gibraltar from the U.K. The U.K.'s spurning of the EU has opened a Pandora's Box of unexpected woe. And this process has not even really gotten started. The economic and political way ahead remains very confused for Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief