Global| Sep 11 2015

Global| Sep 11 2015Shifting French Trade Trends in Uncertain Times

Summary

France's current account slipped into deficit as its deficit on goods trade moved into deeper deficit. Export growth has been exceeding import growth for some time but only over the last nine months have exports got higher enough to [...]

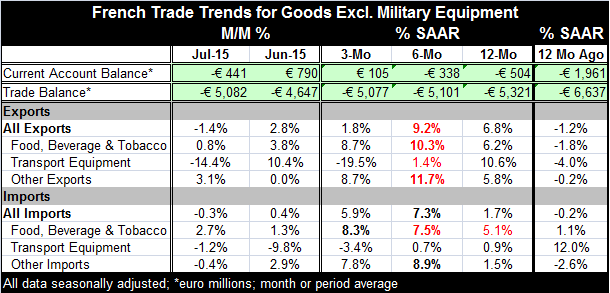

France's current account slipped into deficit as its deficit on goods trade moved into deeper deficit. Export growth has been exceeding import growth for some time but only over the last nine months have exports got higher enough to reduce persistently the French trade and current account deficits. Over 12 months, exports are up by 6.8% while imports are up by only 1.7%.

France's current account slipped into deficit as its deficit on goods trade moved into deeper deficit. Export growth has been exceeding import growth for some time but only over the last nine months have exports got higher enough to reduce persistently the French trade and current account deficits. Over 12 months, exports are up by 6.8% while imports are up by only 1.7%.

But within the last year those trends have been shifting. Import growth has substantially caught up with export growth over six months, and over three months imports are growing much faster than exports.

On the export side, there has been substantial slippage in French auto exports. While they are up 10.6% y/y, they are also contracting at a 19.5% annualized pace over three months. French imports also show weakness in transportation equipment but show countervailing strength in food and beverages as well as from other imports.

Rising exports are sign of French competitiveness. But rising imports are a sign of revived domestic demand. Competitiveness plays on both sides, of course. But the sudden strength of the rising import flow is certainly the result of better domestic demand in France. Global growth has been weak, so we characterize the persisting strength in French exports are stemming from competitiveness, an effect that works though slowly over time. However, we have seen that even Germany, the most competitive economy in Europe, has had a hard time getting export growth up in this environment.

The big thing for Europe is bracing for its the Greek election. After that, attention will swing to the impact of migrants on Europe. Some already are busily handicapping the impact. Few think the net result will be good. European leaders have set out some really low-ball numbers as to the cost of this relief effort. And that cost will be important since Europe is operating under Maastricht budget rules. There is a huge humanitarian crisis. It will have a significant economic impact. But right now no one is willing to face up to that fact.

Europe's economic recovery has been slow. A bad election result in Greece could upset the recovery. Similarly, the budgetary stress of the migrant problem could adversely impact Europe unless it offers special dispensation to countries whose budgetary spending rises because of providing migrant aid. It is too soon to get complacent about the strength of the recovery in Europe. Significant risks still stalk the European economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief