Global| May 05 2009

Global| May 05 2009Sharp, Widespread, PPI Drop Puts ECB On The Spot For A Rate Cut

Summary

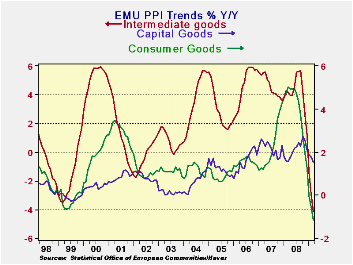

The PPI is not the ECB’s mandated inflation variable. The central bank prefers the broader consumer-based HICP. But the drop in the PPI excluding construction at -0.8% in March, at -10.5% over three months (saar), at -12.3% over 6 [...]

The PPI is not the ECB’s mandated inflation variable. The

central bank prefers the broader consumer-based HICP. But the drop in

the PPI excluding construction at -0.8% in March, at -10.5% over three

months (saar), at -12.3% over 6 months (saar) and at a minus three

percent over 12-months is nonetheless a compelling piece of evidence

for the ECB to confront. Capital goods inflation at +1.5% Yr/Yr is the

high inflation reading for the three main sectors. Consumer goods

prices are lower by 1.2% over 12-months and intermediate goods prices

are lower by 4.1% over 12-months. Europeans are not as worried about

deflation as policymakers in the US, yet they can’t deny these trends.

Inflation, its breadth and its trends all point to the nearly

complete absence of anything that could be called inflation. Indeed

there is growing evidence for those who want to worry about that

opposite concern: deflation. On top of that, the European economy is

very weak.

The controversial aspect of this is that Europe’s finance

ministers are not applying any new stimulus and the head of the

European Commission, Jean-Claude Junker, said that no policies except

those that are already approved should be implemented. That appears to

be an oblique warning from Junker to EU countries not to go off on

their own with any new programs of assistance. Even so Junker admits to

a growing unemployment crisis in Europe. Of course Europe has a more

extensive social safety network than the US. But as the EU Commission

and the OECD and the IMF have cuts forecasts the EU Commission has been

prepared to sit idle and wait for the results of its past stimulus

plans to play out. Moreover, the ECB has been content to let the Bank

of England and the Federal Reserve take the more aggressive monetary

policy actions.

So if there is a risk it is that Europe is getting behind the

curve and perhaps, along with that, a growing risk of deflation. The

continuing sharp drop in inflation – indeed, persisting negative rates

of inflation- hint at an ongoing economic unraveling. However, recent

economic data have suggested in several ways that the economic tailspin

had begun to enter a more controlled phase.

In Spain, programs to arrest sharply rising unemployment seem

to be having some impact. In Germany a car scrappage scheme seems to

have boosted car registrations. The EU PMI for manufacturing shows a

rise in that key sensitive cyclical index that suggests the pace of

economic unraveling its slowing and that signal is echoed across Main

EMU countries. So while Europe’s policies may tread a riskier path that

those in the US there is also some evidence of economic responsiveness

to the counter cyclical policies already implemented and of course

there is that cushier social safety net in Europe.

Nonetheless, this drop in the PPI is sharp, the largest drop

in 22 years. It is putting pressure on the ECB and is expected to

result in another rate cut from Europe’s central bank at its next

meeting. Reasons to oppose such a drop are increasingly scarce.

| E-Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| E-Area | Mar-09 | Feb-09 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Total x Construct | -0.8% | -0.6% | -10.5% | -12.3% | -3.0% | 5.7% |

| Capital Gds | -0.2% | 0.1% | -0.6% | 0.0% | 1.5% | 1.6% |

| Consumer Gds | -0.2% | -0.2% | -5.0% | -4.2% | -1.2% | 5.0% |

| Intermediate&Cap Gds | -0.9% | -1.0% | -14.1% | -13.8% | -4.1% | 4.2% |

| MFG | -0.9% | -0.5% | -8.8% | -13.6% | -5.1% | 5.8% |

| Germany | -0.7% | -0.7% | -10.2% | -6.4% | 1.0% | 3.2% |

| Gy ExEnergy | -0.5% | -0.5% | -5.9% | -5.7% | -1.4% | 2.4% |

| Italy | -0.8% | -0.8% | -10.1% | -14.5% | -4.5% | 6.6% |

| UK | -0.9% | 0.0% | 1.3% | -15.2% | 0.2% | 13.6% |

| E-zone Harmonized PPI ex construction | ||||||

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief