Global| Sep 21 2020

Global| Sep 21 2020Sharp Recovery in Belgian Consumer Index That Remains Quite Weak

Summary

It has been the nature of this recession and of the public reaction and of the government tactics to fight the virus that economic indicators have been put through their paces in a way we have never before seen. We see that in the [...]

It has been the nature of this recession and of the public reaction and of the government tactics to fight the virus that economic indicators have been put through their paces in a way we have never before seen. We see that in the National Bank of Belgium consumer confidence index this month; it's an index that is scoring strong gains and yet remains a weak report.

It has been the nature of this recession and of the public reaction and of the government tactics to fight the virus that economic indicators have been put through their paces in a way we have never before seen. We see that in the National Bank of Belgium consumer confidence index this month; it's an index that is scoring strong gains and yet remains a weak report.

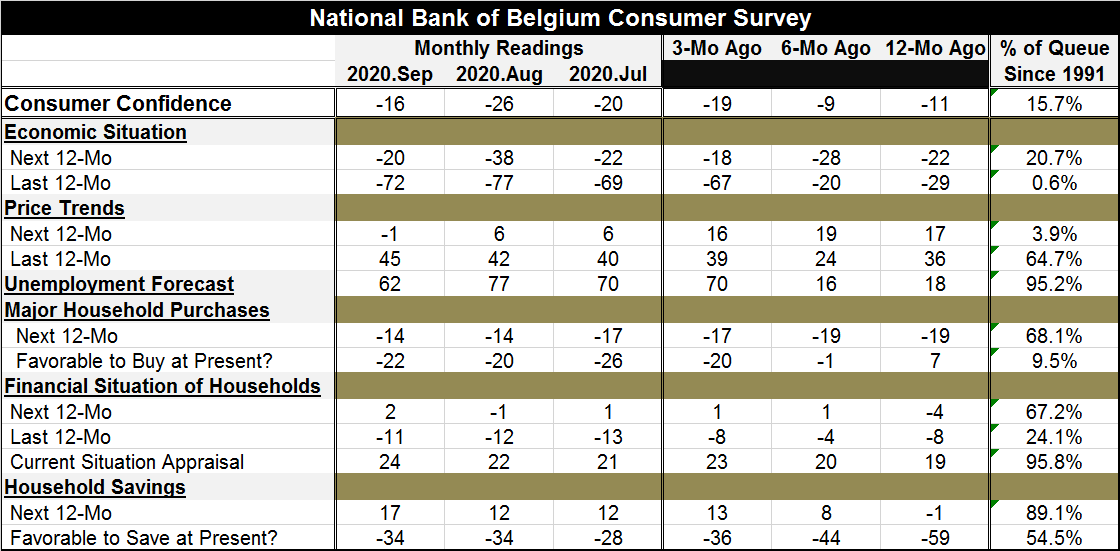

The National Bank of Belgium consumer confidence index is at its highest reading since March. It's the best reading since the coronavirus struck Europe; it jumped by ten points in September alone! Yet, it stands only at its 15.7 percentile- lower than its current value less than 16% of the time, historically back to 1991.

Survey respondents saw improvements in the economic situation for the next 12 months beginning in September. Yet, that September score has only a 20.7 percentile standing historically and still that is up significantly from the 0.6 percentile standing of the view looking back 12 months.

Price trend expected for the next 12 months weakened and the reading fell to the 3.9 percentile in its historic queue of responses. It compares to a looking-back percentile standing of 64.7% in price trends over the last 12 months.

The unemployment forecast saw an improvement as the index response dropped to 62 in September from 77 in August. But that still is a high reading in the top 5% of the queue of values historically. Consumers in Belgium are still worried about the prospect of unemployment.

Interestingly, the buying or spending environment is not considered very favorable with responses logging only a 9.5 percentile standing historically. But looking ahead, the next 12-month reading has a steady 68.1 percentile standing, a much more robust expectation.

The financial situation has a number of somewhat surprising scores. First of all, the three financial assessments (next 12 months, last 12 months and the current situation) have not changed much in recent months. The outlook for the next 12 months has a moderate 67.2 percentile standing. The assessment of the last 12 months has a much lower 24.1 percentile standing. And the assessment of the current financial situation of households gets a much higher 95.8 percentile standing. Apparently, government support programs are reassuring and sustaining people quite well for now, but there are more concerns as consumers look ahead. The saving environment is near its median at present (near a 50th percentile ranking) and it is expected to get better and to be much better over the next 12 months. Once again we see come favorable expectations.

Amid these responses, Europe is having a devil of a time with the virus again. The United Kingdom is under severe risk as warnings are being issued; infections in Spain remain high as well. Belgium is seeing its own outbreaks as infections rise to over 100,000 and it is seeing nearly 1,200 new cases per day. In Belgium, the trend for new infections is up by 62% over the most recent seven-day period (see here). While the National Bank of Belgium survey is weak, it also seems to be still somewhat upbeat. But with the virus spreading like this again, I wonder if this sort of view can persist. Fears of unemployment in Belgium already are high even though they have improved in the September survey.

The environment and outlook seem be in a quite challenging and fast-changing period.

European countries are expected to be imposing more restrictions very soon as the U.K., France, Italy, Germany and Spain have seen a stepped up spread of infection commentary (source here). Suddenly the U.S. seems to be in a very good place compared to Europe although the U.S. has parts of the country that are experiencing their own virus revivals. Make no mistake about it, the virus is still calling the tune for policy globally with few exceptions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief