Global| Jun 21 2016

Global| Jun 21 2016Sharp Rebound in German ZEW Expectations; What Do ZEW Experts See that Janet Yellen and Her Merry Band of Fed [...]

Summary

Despite the unexpected and relatively sharp rise in June's German expectations, the June expectations index is still higher nearly half the time (43%, approximately). Current conditions in Germany are better only 17% of the time, [...]

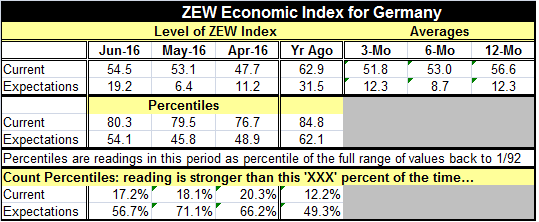

Despite the unexpected and relatively sharp rise in June's German expectations, the June expectations index is still higher nearly half the time (43%, approximately). Current conditions in Germany are better only 17% of the time, making the German assessment by the ZEW financial experts a relatively strong reading this month. Apparently the nagging fears about the economy have dissipated as the ZEW forward-looking (what else would it be?) expectation assessment is as high as it has been since August 2015. German expectations in this most recent episode peaked in March 2015 and began to erode, losing 10 points of index value in May 2015 and another 10 points in June then lopping off more than 10 points in August. So this month's recovery to a reading of 19.2 marks some sort of watershed revival. Paper hats everyone! Drum roll...and Ta-Da: the expectations index has move up more strongly than this only 14% of the time historically. Nice move Germany!

Despite the unexpected and relatively sharp rise in June's German expectations, the June expectations index is still higher nearly half the time (43%, approximately). Current conditions in Germany are better only 17% of the time, making the German assessment by the ZEW financial experts a relatively strong reading this month. Apparently the nagging fears about the economy have dissipated as the ZEW forward-looking (what else would it be?) expectation assessment is as high as it has been since August 2015. German expectations in this most recent episode peaked in March 2015 and began to erode, losing 10 points of index value in May 2015 and another 10 points in June then lopping off more than 10 points in August. So this month's recovery to a reading of 19.2 marks some sort of watershed revival. Paper hats everyone! Drum roll...and Ta-Da: the expectations index has move up more strongly than this only 14% of the time historically. Nice move Germany!

German current conditions are hardly changed month-to-month but are a touch firmer. The current index made a more substantial move to higher ground last month.

Compared to one year ago, both the current and future indices are lower each by considerable margins in terms of index points. But in terms of their relative percentile queue standings, the weakness is not so pronounced. The ZEW current index was higher only 12% of the time one year ago; that metric has slipped to 17% of the time in June. The expectations metric was higher 49% of the time one year ago; now that reading has slipped so that it has been higher about 57% of the time.

The investment ratings for both stocks and bonds are up this month. It's the best stocks reading since February of this year and the best bond rate since March. These are relatively minor improvements.

Consumption/trade, construction and info-tech continue to be three very high ranking sectors in terms of expected investment performance. While construction was rated a bit lower in June compared to May, the only other sectors getting a weaker reading month-to-month were banking and insurance (both of which had extremely low ranking to start), undoubtedly due to the impact of low or negative interest rates across the euro area. On balance, however, the ZEW experts see profits expectations overall are on the rise. On Dasher, on Dancer, on Claus, on Deiter, as optimism reigns in Germany.

Somewhat like Japan's 'Economy Watchers' Index

One interesting aspect of this report is that this is not a survey of actual conditions but the assessment of ZEW financial experts whose views are polled. The experts had been expected to downgrade their outlook instead of improve it with such a jolt. It strikes me that the news on the turnaround in the Brexit poll is simply too fresh to have impacted this survey so sharply. However, the cut-off date for the ZEW survey was 6/20/16 so it's possible that a critical mass of ZEW members may have held back and reacted to the freshest polls on Brexit for this survey, polls which have had a solid positive impact on markets this week. The ZEW index precedes the release of the IFO index which is a real sampling for industry-level activity. ZEW and the IFO generally move together.

ZEW President Achim Wambach Steffen said that the index was showing the confidence that financial market experts have in the German economy. President Steffen's description was also of challenging economic conditions amid weak global dynamics and uncertainty over the Brexit vote.

Meanwhile across the pond...

Interestingly, Fed Chair Janet Yellen will today in Washington before the Committee on Banking, Housing, and Urban Affairs. The Fed recently cut its expected rate-hike path and reduced slightly its outlook. While we can expect that Fed policy is geared mainly to the U.S. and that the ZEW financial experts are mainly focused on Germany, the divergence between what the ZEW experts are seeing and what the Fed is seeing is striking for two of the world's largest economies both of which are firmly plugged into the global economy. These economic assessments will bear watching.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief