Global| Nov 05 2008

Global| Nov 05 2008Services Sectors Tank in US and in Europe

Summary

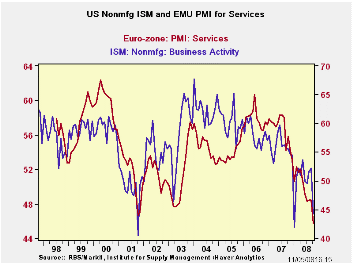

The chart serves as yet another reminder as to why it has been loopy for observers to have insisted that Europe and the US had become disconnected economically – the so-called de-coupling argument. The MFG sectors across countries are [...]

The chart serves as yet another reminder as to why it has been

loopy for observers to have insisted that Europe and the US had become

disconnected economically – the so-called de-coupling argument. The MFG

sectors across countries are always closely connected because they

trade goods and compete in the same markets for the same business. The

services sectors have a lower incidence of tradable services – much

lower than for goods. Still, the overall EMU and US economies have been

on such similar cycles that their two service sector indices, with very

few exceptions, have been on the same page.

The EMU in country level measures are mostly on their

respective lowest readings since May of 2000. The US measure is in its

bottom 13% of its range –also very weak. Germany’s measure is ‘only’ in

the bottom 28% of its range.

The drop in the EMU index in October is its largest m/m drop

since May 2000 when the comparisons start.

We can also see that consumer confidence is very low in most

of these same places. Since the service sector provides the bulk of the

jobs, this is an expected result.

However we can also use this report as a double check on the

MFG report which earlier was reported to have fallen so sharply. These

two sectors are showing the same sharp onset of weakness. That tends to

imbue the signal with a greater veracity than if the result came from

just one survey. The weak signal therefore seems to be the result of a

real weakness in the economy rather than from some quirk of the

calendar or a peculiarity of one survey.

| NTC Services Indices for EU/EMU | |||||||

|---|---|---|---|---|---|---|---|

| OCT-08 | SEP-08 | AUG-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 45.76 | 48.44 | 48.46 | 47.55 | 48.45 | 50.37 | 0.0% |

| Germany | 48.31 | 50.25 | 51.39 | 49.98 | 51.49 | 51.78 | 28.3% |

| France | 47.54 | 50.14 | 48.04 | 48.57 | 48.96 | 53.05 | 0.4% |

| Italy | 45.68 | 49.42 | 48.47 | 47.86 | 47.63 | 48.32 | 0.6% |

| Spain | 32.22 | 36.09 | 38.98 | 35.76 | 37.39 | 41.65 | 0.0% |

| Ireland | 36.05 | 40.80 | 39.82 | 38.89 | 40.65 | 45.31 | 0.0% |

| EU only | |||||||

| UK (CIPs) | 42.39 | 45.95 | 49.17 | 45.84 | 46.98 | 49.60 | 0.0% |

| US NONFMG ISM | 44.20 | 52.10 | 51.60 | 49.30 | 50.17 | 50.48 | 13.6% |

| EU Commission Indices for EU and EMU | |||||||

| EU Index | OCT-08 | SEP-08 | AUG-08 | 3Mo | 6Mo | 12Mo | Percentile |

| EU Services | -10 | -4 | -2 | -20.67 | -19.00 | -14.92 | 0.0% |

| EMU | OCT-08 | SEP-08 | AUG-08 | 3Mo | 6Mo | 12Mo | Percentile |

| Services | -6 | 0 | 1 | -1.67 | 2.17 | 5.79 | 0.0% |

| Cons Confidence | -24 | -19 | -19 | -20.67 | -19.00 | -1.11 | 0.0% |

| Consumer confidence by country | |||||||

| Germany-Consumer Confidence | -12 | -9 | -9 | -10.00 | -7.50 | -3.83 | 34.4% |

| France-Consumer Confidence | -32 | -24 | -23 | -26.33 | -23.83 | -18.58 | 0.0% |

| Ital-Consumer Confidence | -23 | -22 | -24 | -23.00 | -22.83 | -22.83 | 13.8% |

| Spain-Consumer Confidence | -44 | -39 | -37 | -40.00 | -38.00 | -29.08 | 0.0% |

| UK-Consumer Confidence | -27 | -23 | -24 | -24.67 | -22.50 | -15.25 | 0.0% |

| percentile is over range since May 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.