Global| Jun 03 2015

Global| Jun 03 2015Services Sector and Total EMU PMI Slip in May

Summary

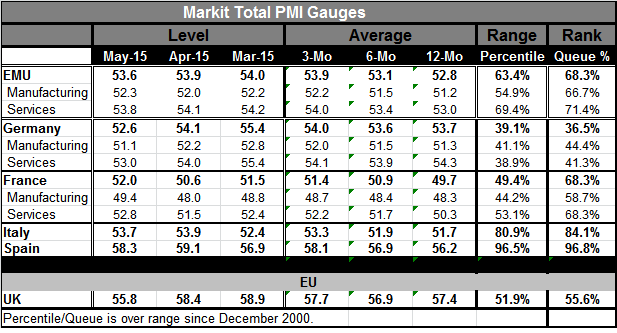

The May EMU finalized PMI fell to 53.6 from 53.9 in April. Germany, Italy and Spain lost momentum. Only France showed improvement of its total PMI in May. The EMU has a queue standing of its overall PMI gauge in the 68th percentile in [...]

The May EMU finalized PMI fell to 53.6 from 53.9 in April. Germany, Italy and Spain lost momentum. Only France showed improvement of its total PMI in May.

The May EMU finalized PMI fell to 53.6 from 53.9 in April. Germany, Italy and Spain lost momentum. Only France showed improvement of its total PMI in May.

The EMU has a queue standing of its overall PMI gauge in the 68th percentile in May, with France at the same level, Italy at its 84th percentile and Spain at its 96th percentile. Germany has lagging standing that is only in its 36th percentile. In terms of raw scores, Germany is only showing a higher overall PMI than France.

There are still many cross currents in the EMU as well as in the global economy. The EMU showed its lowest unemployment rate in April since March 2012. The unemployment rate fell to 11.1% from 11.2%. Still, this rate is in the top 25th percentile of all rates of unemployment since late 1998. While the EMU unemployment picture is improving, it is improving at a very slow pace and the differences within the community are not dissipating with any speed.

The OECD today cut its outlook for global growth. The Paris-based OECD cut the world growth forecast for this year to 3.1% from 3.6%. However, it says that it expects lower oil prices to ensure a gradual recovery, even if weak investment remains weak. This seems a bit Pollyannaish. It's a weaker outlook for an already weak economy. And risks still abound.

Economists are complacent about the outlook on the notion that it takes some sort of a shock to create a recession. Yet, the global economy continues to struggle and trade continues to be a battle among weak currencies as nations use foreign exchange weakness to try to get a bigger share of an ever disappointing global market. These forces continue to put growth at risk. No nation is really trying to create more growth; instead this is a zero sum game in which nations are using exchange rates to try to get a share of whatever growth they find overseas. There is no pump-priming. We have globally aging populations and global fiscal austerity with few exceptions (China now and then). The aging population is saving more instead of spending while governments are keeping the reins on fiscal spending. There is monetary stimulus, but it can't work amid such conditions of slack demand; instead, such monetary excess brings risk. After all, what sense is there in pumping up equity markets because interest costs are low if earnings can't be stimulated?

Europe is still juggling Greece. Europe finally has come together with a take-it-or-leave-it plan it is offering up to Greece this week. Greece has its own plan, but that is not likely to get any consideration. Greece has dropped its `nice-debtor' face and has said without a deal it will not pay the IMF at the week's end. That means this week is the key one. Most expect Greece to knuckle under and submit to the EU's plan even though that plan just kicks the can down the road.

We cannot help but look at Europe's PMI progress and bemoan its sluggishness. Most PMI gauges are above 50 and few have been much stronger. But the there is only weak momentum. The EMU, too, is relying on its weak exchange rate to pull it ahead. But when you see how poorly Germany, the most competitive country in the EMU, is doing with such a weak manufacturing sector PMI reading, you realize that there is not much demand out there to exploit even with the cheapest prices on the block. I fear that the growth situation for Europe and for the U.S. is more dangerous than policy makers appreciate.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief