Global| Mar 05 2014

Global| Mar 05 2014Services Mostly Turn Higher in EMU

Summary

The services sector in the European Monetary Union improved in February, registering a diffusion value of 52.57, up from 51.57 in January. The 12-month average for the diffusion metric is 49.94. The euro area has progressed to a point [...]

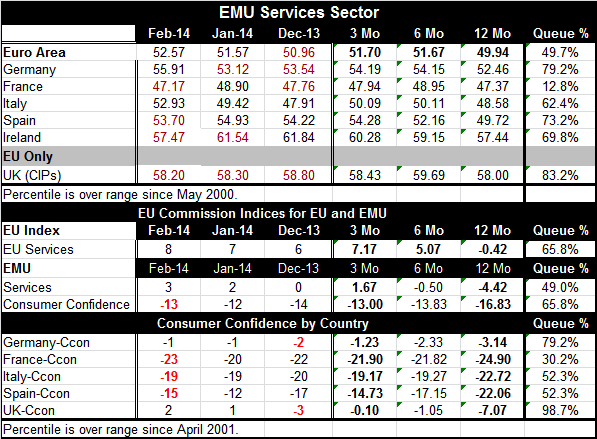

The services sector in the European Monetary Union improved in February, registering a diffusion value of 52.57, up from 51.57 in January. The 12-month average for the diffusion metric is 49.94. The euro area has progressed to a point where the services sector is advancing. However, when we take a look at this value and place it in its queue of historic values, it resides in the 49.7th percentile, which is just below the median. Although the euro area has shown an expansion, it has not yet reached the point of normalcy.let alone `recovery.'

The services sector in the European Monetary Union improved in February, registering a diffusion value of 52.57, up from 51.57 in January. The 12-month average for the diffusion metric is 49.94. The euro area has progressed to a point where the services sector is advancing. However, when we take a look at this value and place it in its queue of historic values, it resides in the 49.7th percentile, which is just below the median. Although the euro area has shown an expansion, it has not yet reached the point of normalcy.let alone `recovery.'

Germany also saw its services PMI improve in February, along with Italy. France, Spain, and Ireland saw slippage in their service sector readings in February. Ireland saw a sharp decline to 57.47 from 61.54. However, despite that drop, Ireland's reading still sits at about the 70th percentile of its historic queue. Spain, at 53.70, sits in the 73rd percentile of its historic queue. But France, having slipped to 47.17 from 48.90, now sits in the bottom 13th percentile of its historic queue, at an exceptionally weak reading. There continues to be a good deal of dispersion in the performance metrics for the EMU services sector.

The UK is not a member of the single currency union. It saw a very slight drop in its services PMI to 58.2 from 58.3. That's still represents a slight pick up from 58.0, its 12-months average. The UK measure sits in the 83rd percentile of its historic queue and is among one of the strongest services sectors in Europe.

Along with the services sectors, we show surveys of consumer confidence in a number of countries and continue to find that there is a great divide between Germany and other EMU members when it comes to the assessment of consumer sentiment. Germany's metric is near the top 20th percentile of its historic queue of data while France is in the bottom 30% and Italy and Spain are just above the 52nd percentile of their respective historic queues. In the UK, we find a strong showing for consumer confidence as its consumer sentiment gauge resides in the 98th percentile of its historic queue.

The services sector is showing improvement in Europe. Although the metric itself points to service sector growth, we have to remember that the services sector usually does grow and that its current value is actually below its median performance. For those looking for economic recovery, `recovery per se' is usually a period when growth exceeds its long-term average -and its long-run potential - for a spell. Europe is not there yet. There also are, as we saw, substantial differences among member countries in the performance of their respective services sectors. In addition, German consumer confidence is leagues ahead of confidence levels in fellow monetary union member countries although its level of confidence is exceeded by consumer confidence in the UK.

By comparison, the US nonmanufacturing sector (services plus construction) registered a small decline in February. Although its diffusion value is only slightly below the value for Europe, the queue standing for the US PMI is in the bottom 25th percentile of its historic queue. Services sectors around the world continue to lag which is a problem because services sectors tend to be the job creating sectors. Jobs simply are not being created with enough vigor in the US and Europe. Domestic demand continues to lag in most countries, while those same countries continue to put their hopes on export-led growth, which depends on domestic demand in other countries. There is an obvious inconsistency here.

There has been no sense of trying to manage and coordinate international growth. There has been no sense of trying to reduce the international imbalances where they seem to be the most entrenched. Europe has gone the route of addressing internal budget imbalances alone. That effort has produced some results, but also has had enormous side-effects on growth. There is a great deal of excitement about Europe finally turning the corner to growth, but perhaps we put too many eggs in that basket as Europe's growth continues to be measured and is rife with internal inconsistencies. Europe may have achieved growth, but it has not achieved recovery yet. Some think that, with the PMI indicators for Europe improving, some of the heat will be taken off of the European Central Bank. However, Europe is not exactly knocking them dead with its strength and the growth irregularities within the Community are still severe and threaten continuity. It is always it's the laggard countries within the Community that need the help - and some of them continue to lag badly.

For its part, the Federal Reserve has already taken several steps down the road of tapering, to reduce its accommodative stance. However, economic statistics, since the Fed began taking those steps, have become mixed and weaker. The question surrounding the US economy revolves around the weather which has been unseasonably cold, blustery and filled with storms. Is the recent US weakening, due to weather or due to a change in the economic climate? For the most part, there are unclear signs. The weather seems to have disrupted the economy to some extent. Yet, it's not uncommon for economists overestimate the impact of storms on the economy since when one part of economic activity is affected often another part of economic activity is stimulated. As a result of that, the deadweight loss from storms tends to be overestimated. I dwell on the US to some extent because Europe depends on US domestic demand to fire its export machine and it's unclear that the US is going to provide that kind of growth. China has publicly and purposely declared that it is trying to stimulate its domestic growth through the revival of domestic demand. Perhaps Europe should try to do the same thing; especially having Germany, the country with the largest current account surplus in the world, in it's very midst?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.