Global| Jun 06 2013

Global| Jun 06 2013Run of Good News Ends as German Orders Back-Track

Summary

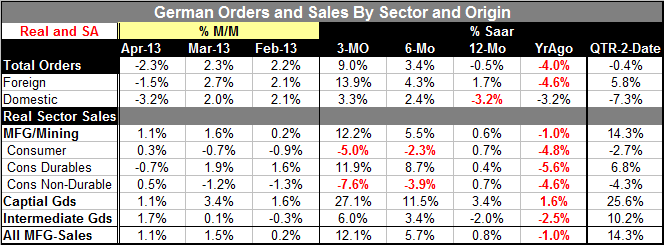

There was a 2.3% drop in real German orders in April compared to March. The drop wiped-out the March gain. And while that does take the glow off of some of the recent data that has been suggesting improvement or lesser downdraft in [...]

There was a 2.3% drop in real German orders in April compared to March. The drop wiped-out the March gain. And while that does take the glow off of some of the recent data that has been suggesting improvement or lesser downdraft in the Eurozone, the chart for German orders shows clearly that both domestic and foreign orders have been very gradually, very slowly, but very steadily, crawling their way back to zero in terms of their year-over-year growth.

There was a 2.3% drop in real German orders in April compared to March. The drop wiped-out the March gain. And while that does take the glow off of some of the recent data that has been suggesting improvement or lesser downdraft in the Eurozone, the chart for German orders shows clearly that both domestic and foreign orders have been very gradually, very slowly, but very steadily, crawling their way back to zero in terms of their year-over-year growth.

Trends for German orders are still showing improving sequential growth rates. Over three months the annual rate of growth is 9% better than 3.4% over six months which in turn is better than a decline of 0.5% over 12 months. The trend for foreign orders similarly shows annualized growth of 13.9% over three months better than 4.3% over six months and better than 1.7% over 12 months. Domestic orders are showing improving growth rate trends with a 3.3% annual rate over three months, a 2.4% annual rate over six months Vs a decline of 3.2% over 12 months. In addition, of course, the twelve-month growth rates across the board are better than the year ago twelve-month growth rates

Despite my negative headline for this report that's a lot of good news that's in train. But for the quarter to date trends are much less positive. Of course, we are only one month into the new quarter. Taking the April level of orders as an annual growth rate compared to the first quarter base, total orders are falling at a 0.4% annual rate. Foreign orders are still increasing at a 5.8% annual rate, while German domestic orders are falling at a 7.3% annual rate- all for 2013-Q2 over Q1.

Real sector sales for mining and manufacturing or just for manufacturing alone are also showing progressive increases in their rates of growth. Manufacturing sales are growing at 12.1% at an annual rate over three months, by 5.7% over six months, and by 0.8% over 12 months. For this series even the quarter to date growth rate is robust at 14.3%. But, of course, this is the coincident indicator of sales; it's the leading indicator, 'orders' in which we find some weakness.

Euro Flooding

While it hasn't gotten into any figures yet, flooding of central Europe looks like it's going to be a pretty major event that will be affecting economic data. Germans are currently holding their breath over Dresden which is the city most recently threatened by rising water levels. Countries that have appealed to the EU for emergency assistance from its special fund have been told that the fund is depleted and there is no money for flood assistance. Apparently the man-made disasters in the Eurozone have absorbed all of the resources Europe has to offer and when Mother Nature has come knocking there is nobody home to offer any help.

Beyond flooding...

This is just another example of why countries need to get their house is in order. Weather has become much more volatile and more damaging and challenging to all economies and jurisdictions. In addition, debt problems around the world from the national to the municipal level to the corporate level to the individual level affecting real business and deferred obligations (like pensions and other promised future benefits to retirees) seem to be lurking around every corner. Countries/firms/local jurisdictions that don't deal with their current needs are going to find these sorts of problems when they arise to be even more difficult to deal with.

While there seems to be a level of affluence that has been reached in the developed nations in which a spirit of benevolence has become more widespread, as political leaders and individuals have sought to improve the mix of benefits and services conferred to citizens the harsh truth is that most countries are in a position of having already promised too much. They are in need to pull back on these promises rather than to extend them. The combination of productivity, technological advance, and the spread of productive capital resources to the world's lowest wage countries are creating stiff competition that effectively reduces the ability of higher income countries to sustain what have been their historic growth rates - and therefore tax revenues. In addition, demographic trends are leaving fewer people to work and to pay into the tax coffers that are the source of the lucre that supports these benefits.

Both Western European countries and the United States need to pay closer attention to what they can afford. Various natural disasters from the odd hurricanes or storms that have buffeted New York City, to a proliferation of highly destructive hurricanes in Oklahoma, to extraordinary ongoing flooding and otherwise wet weather in Europe are all symptoms of changing weather patterns that are wreaking havoc on our economy and for which someone will have to pay. (...and I don't mean to ignore earthquakes and Tsunami's like the one that devastated Japan.) In addition to that there are the ongoing fiscal deficits that take a toll on public finances. And as a result of that there's a need to reduce debt. And for those reasons it's difficult if not impossible to extend benefits. Yet the financial crisis has spawned an economic recession which has produced an anemic global recovery and lingering economic problems all of which make an agenda extending benefits even more difficult. We know that there are still problems from the financial crisis that are lurking partially hidden in the balance sheets of financial institutions in various ways. Should we ignore them, and then act surprised they appear?

The sputtering growth in Europe and in particular the new setback for Germany, Europe's most competitive economy, is an opportunity for us to pause and to reassess the decisions we are making and to reassess policy in general. Heated up geopolitical hotspots simply remind us of how hard it is to get cost savings to fuel political agendas back home. These events cause us to rethink what kind of peace dividend we will have while the ongoing weak growth continues to postpone the day when we can get our national finances back to normal. Will it ever come? And lingering high unemployment rates or unemployment rates that are reduced for special reasons that are believed to be temporary cannot reassure us as they continue to make strong demands on various national treasuries.

I think that many of us - and in fact many more of us each day - are looking at the global economy, and at the damage from the financial crisis, and at our current circumstances, wanting to make things better, but lacking any real solutions. Central banks have gone way out of their way and have done all that they can and maybe more than they should. There is no agreement on what fiscal policy should do. It's pretty clear that fiscal policy has gone off the tracks in the past but there is an ongoing debate about whether it plays a role in getting us back on the track or whether the best that it can do is to be contained so that it doesn't get out of control again. Left to its own devices capitalism has created a lot of dislocation and is worsening the distribution of income. And that's not a good thing for economic growth or for political stability. And that's something we need to think hard about and to fix. Is this a new Schumpeterian wave of creative destruction or just destruction?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief