Global| Apr 14 2015

Global| Apr 14 2015Rising European Output Struggles to Make Annual Gains

Summary

European Monetary Union (EMU) industrial production (excluding construction) rose a smart 1.1% in February, its strongest gain in eight months. Manufacturing output rose by 1.2%, its strongest gain in eight months as well. Still, [...]

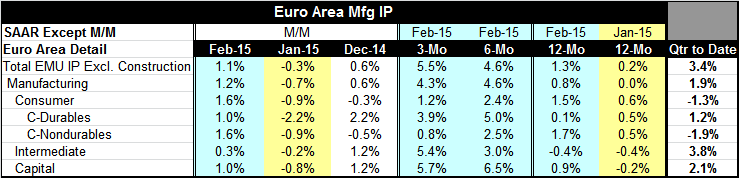

European Monetary Union (EMU) industrial production (excluding construction) rose a smart 1.1% in February, its strongest gain in eight months. Manufacturing output rose by 1.2%, its strongest gain in eight months as well. Still, year-over-year the main production sectors are marking time, with weak gains and little momentum (see chart).

European Monetary Union (EMU) industrial production (excluding construction) rose a smart 1.1% in February, its strongest gain in eight months. Manufacturing output rose by 1.2%, its strongest gain in eight months as well. Still, year-over-year the main production sectors are marking time, with weak gains and little momentum (see chart).

Since the global and European economies have been weak for some time, there is still a great deal of economic slack present. For that reason, the recent pattern of the industrial production rebound looks unbalanced. Production is being led by gains in intermediate goods and capital goods. But capital goods should not be in such strong demand early in the rebound cycle -at least not for a region as broad as the euro area. But that is what is happening over three months and six months. What should be leading is consumer demand and the output of consumer goods.

On a broader scale looking at one-year gains, the composition of the output rise makes more sense and follows this pattern. Consumer goods output is up by 1.5% year-on-year with durable consumer goods output gaining just 0.1%. Nondurable goods output is up by a stronger 1.7%. Capital goods output is trailing, rising by 0.9% with intermediate goods output shrinking on balance over 12 months.

The three-month and six-month growth rates across sectors are very different from the 12-month rates of growth. Clearly output has been improving on these two shorter horizons.

By country, of the 11 early reporters of manufacturing output, only three had month-to-month declines in output in February compared to seven with declines in January. However, over three and six months on each horizon, only two of these members have net declines in output compared to five with output declines over 12 months.

Both the growth rate of IP and the breadth of the output gains across EMU members are improving. While the output of consumer goods is leading over 12 months, it is not gaining momentum. Still, with the ECB's stimulus program in gear, it is very helpful to see the real sector posting growth. In an environment of growth, financial stimulus is much more likely to work. And of course European financial markets have helping buy pushing interest rates into negative territory on a broad front. For the moment, Europe has everything moving at least in the right direction. Can it sustain this and will it build momentum?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief