Global| Dec 12 2002

Global| Dec 12 2002Retail Sales Rose Moderately

by:Tom Moeller

|in:Economy in Brief

Summary

Retail sales rose last month in line with Consensus expectations for a 0.4% gain. October sales were revised up due to slightly stronger gains in auto and nonauto sales. Total retail sales were up at a 2.7% annual rate YTD through [...]

Retail sales rose last month in line with Consensus expectations for a 0.4% gain. October sales were revised up due to slightly stronger gains in auto and nonauto sales. Total retail sales were up at a 2.7% annual rate YTD through November.

Sales excluding motor vehicles and parts dealers rose quite a bit more than expectations for a 0.2% gain. Year to date nonauto retail sales were up at a 4.9% annual rate through November.

Furniture and home furnishing store sales rose 1.6% (3.4% YTD, AR) following strong results in the prior four months which were revised higher. The November gain reflected a huge 2.3% rise in furniture sales and a 0.9% rise in electronics and appliances sales.

Sales at general merchandise stores rose 0.3% adding to a 1.2% gain in October. Year to date sales were up at a 4.5% rate through November.

Apparel store sales fell a sharp 1.3% (1.1% AR, YTD) following a huge 5.5% gain in October.

Motor vehicle dealers' sales fell a slight 0.1%, the third monthly decline in a row. The decline may have reflected price discounting. Unit sales of light vehicles rose 3.8% last month to 16.04 mil.

Sales at gasoline service stations rose 0.4%.

| Nov | Oct | Y/Y | 2001 | 2000 | 1999 | |

|---|---|---|---|---|---|---|

| Retail Sales & Food Services | 0.4% | 0.1% | 2.1% | 3.9% | 6.7% | 8.4% |

| Excluding Autos | 0.5% | 0.8% | 5.0% | 3.4% | 7.3% | 7.4% |

by Tom Moeller December 12, 2002

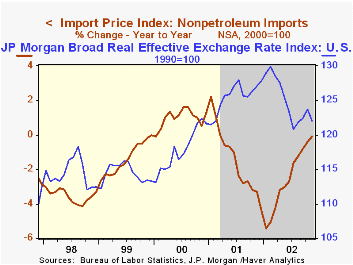

Prices for imported commodities fell much more than Consensus expectations for a 0.1% decline. October figures were little revised.

Petroleum import prices fell sharply and by the most since back to back double digit declines last Fall. Still, petroleum prices are up at a 51.6% rate since December. So far in December the price of Arab Light crude oil has run slightly higher than the $22.20/bbl averaged in November.

Nonpetroleum import prices rose slightly following the slight October drop (0.3% YTD, AR).

Prices of imported capital goods were unchanged following two down months. Nonauto consumer goods prices fell for the second month in three and imported motor vehicle prices also were down.

Export prices rose slightly (1.3% YTD, AR). Food prices rose strongly, reversing the prior month's steep drop. Other export prices either fell or were tame.

| Import/Export Prices (NSA) | Nov | Oct | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Import - All Commodities | -1.0% | 0.0% | 2.4% | -3.5% | 6.5% | 0.9% |

| Petroleum | -10.0% | 0.3% | 37.5% | -17.2% | 66.5% | 34.2% |

| Nonpetroleum | 0.1% | -0.1% | -0.1% | -1.5% | 1.0% | -1.4% |

| Export - All Commodities | 0.1% | -0.1% | 1.0% | -0.8% | 1.6% | -1.3% |

by Tom Moeller December 12, 2002

Initial claims for unemployment insurance surged more than expected last week. Aberrant seasonal adjustment factors were cited by the Labor Department as the reason for recent volatility.

The four-week moving average of initial claims rose to 387,250, down 10.9% y/y.

Continuing claims for unemployment insurance fell a sharp 4.8% w/w following a like decline the prior week.

The insured rate of unemployment fell to 2.6%, the lowest level since September 2001.

| Unemployment Insurance (000s) | 12/07/02 | 11/30/02 | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Initial Claims | 441.0 | 358.0 | 7.3% | 405.8 | 299.8 | 297.7 |

| Continuing Claims | -- | 3,284 | -10.2% | 3,021 | 2,114 | 2,186 |

by Tom Moeller December 12, 2002

The US current account deficit came in slightly below expectations last quarter, but remained near a record level. The deficit in 2Q was revised shallower.

The deficit in goods, services and income trade eased slightly but remained near the record. The deficit in goods and services trade deteriorated to a new record. The deficit in the income balance eased slightly.

Foreign ownership of assets in the US rose by $148.5B versus a gain of $204.3B in 2Q and a peak rate of $302.5B early last year. Direct investment into the US improved slightly last quarter but remained at a level not seen since the mid-1990s.

| US Int'l Balance of Payments | 3Q '02 | 2Q '02 | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Current Account Deficit | $127.0B | $127.6B | $91.3B | $393.4B | $410.3B | $292.9B |

| % of GDP | 4.8% | 4.9% | 3.6% | 3.8% | 4.5% | 3.5% |

| Deficit on Gds, Serv & Income | $113.8B | $114.6B | $79.0B | $343.9B | $356.9B | $244.1B |

| Exports | 2.5% | 4.8% | 1.1% | -9.6% | 13.6% | 4.7% |

| Imports | 1.6% | 8.3% | 9.8% | -8.4% | 18.9% | 10.4% |

| Unilateral Transfers Deficit | $13.2B | $13.0B | $12.4B | $49.5B | $53.4B | $48.8B |

by Tom Moeller December 12, 2002

The index of mortgage applications, compiled by the Mortgage Bankers Association, plunged last week. The decline reversed the run-up in early November and dropped total applications 35% below the early October high.

Mortgage applications to refinance collapsed, leaving them 45% below the early October high yet still up versus last year.

Mortgage applications for home purchase have remained relatively firm.. The recent contract rate on a conventional 30 year mortgage was 5.95%, up modestly from the low.

| MBA Mortgage Applications (3/16/90=100) | 12/06/02 | 11/01/02 | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|

| Total Market Index | 862.7 | 1,030.5 | 625.6 | 322.7 | 352.0 |

| Purchase | 358.8 | 369.5 | 304.9 | 302.7 | 275.8 |

| Refinancing | 3,793.8 | 4,875.1 | 2,491.0 | 438.8 | 795.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief