Global| Nov 05 2009

Global| Nov 05 2009Retail Sales Continue to Sag as Auto Registrations See Stimulus

Summary

Retail sales fell again in September in the e-Zone. Retail sales and vehicle registrations are on nearly opposite paths. Sales are still falling while vehicle registrations bolstered by an assortment of government programs have been [...]

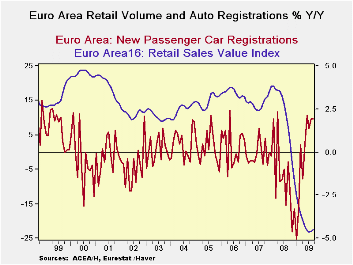

Retail sales fell again in September in the e-Zone. Retail

sales and vehicle registrations are on nearly opposite paths. Sales are

still falling while vehicle registrations bolstered by an assortment of

government programs have been spurred higher. All this stirs the pot of

controversy since in the EU Commission indices that describe the

various EMU sectors, consumer confidence and retailing tend to show the

highest relative scores. Based on the EU surveys it would seem that

consumer attitudes and retailing are leading EMU ahead, yet in terms of

the hard data on spending that matter most that does not seem to be

true.

Partly this divergence is a question of looking at levels of

Vs changes. The levels of satisfaction assessed for the consumer and

retailing sector surveys by the EU Commission are high relative to

other sectors (though still low in absolute terms). For MFG and even

services the relative levels of the indices compared to normal times

are extremely low, but theses sectors had fallen hard in recession and

are now rising, or rising strongly as is the case with MFG and despite

their low ratings they are boosting growth the most.

So far European recovery seems to have come on the back of the

industrial sector with rising output and orders but from an extremely

low level. But with the euro currency also rising in value Vs other

currencies, much of this demand seems to have been foreign-sourced thus

questioning how far Europe can go without participation from its own

consumers. The string of declines in retail sales raises that question

again. It may be that the auto incentive schemes have diverted some

spending from retail sales. But the European recovery cannot be based

simply on selling autos and exporting. We continue to look for life in

retailing to give optimism to the view of a sustained euro-recovery.

| Euro Area Retail Sales | ||||||

|---|---|---|---|---|---|---|

| M/M | SAAR | |||||

| Sep-09 | Aug-09 | Jul-09 | 3-Mo | 6-Mo | 12-Mo | |

| Zone Total Value | -0.3% | -0.2% | -0.2% | -3.0% | -3.3% | -4.6% |

| Food,Beverages,Tobacco | -0.1% | -0.1% | -0.2% | -1.8% | -2.1% | -2.1% |

| Registrations: | ||||||

| Motor Vehicle Registration | 6.7% | -6.8% | 0.2% | -1.5% | 33.3% | 9.7% |

| Nonfood Country detail: Volume | ||||||

| Germany Value | -0.5% | -1.8% | 1.5% | -3.4% | -3.9% | -4.0% |

| UK (EU) Volume | 0.0% | 0.1% | 0.3% | 1.4% | 3.3% | 2.4% |

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia. | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief