Global| Jan 15 2015

Global| Jan 15 2015Record Surplus in EMU as Euro Slides

Summary

Weak growth and a sharply falling currency have driven the EMU to its largest trade surplus on record. Clearly trade is not driving the currency but macroeconomic needs and the currency are driving trade results and deficits. The [...]

Weak growth and a sharply falling currency have driven the EMU to its largest trade surplus on record. Clearly trade is not driving the currency but macroeconomic needs and the currency are driving trade results and deficits. The currency movements have been making international imbalances worse as the EMU surplus, the largest on record is rising while a strengthening dollar is pushing U.S. trade deeper into deficit as the U.S. is losing the improving trend from domestic oil production that will eventually undermine its trade progress. Exchange rates are always a tale of at least two countries.

Weak growth and a sharply falling currency have driven the EMU to its largest trade surplus on record. Clearly trade is not driving the currency but macroeconomic needs and the currency are driving trade results and deficits. The currency movements have been making international imbalances worse as the EMU surplus, the largest on record is rising while a strengthening dollar is pushing U.S. trade deeper into deficit as the U.S. is losing the improving trend from domestic oil production that will eventually undermine its trade progress. Exchange rates are always a tale of at least two countries.

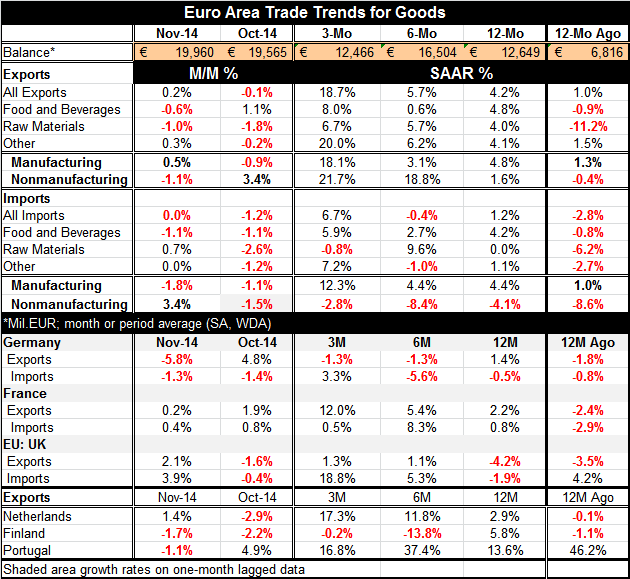

On the month, EMU exports are up a small 0.2% with imports flat. However, sequential growth rates tell a more powerful story of trend development. Exports accelerate from 4.2% over 12 months to growth of 5.7% over six months and 18.7% over three months. Meanwhile, imports remain comparatively tempered, rising by 1.2% over 12 months, falling at a -0.4% pace over six months and up at a 6.7% pace over three months.

EMU manufacturing export and import flows both show more or less steady acceleration with imports holding a slight edge on growth over most horizons. However, for non-manufactures, export growth expands to a very strong pace over six months and even stronger over three months. Meanwhile, for non-manufactures imports, flows are withering on all horizons.

With weak exports, Germany seems to be an exception in the euro area and Europe. German exports fall over three and six months; German imports fall over 12 and six months. However, France and the U.K. show accelerating exports. French imports are erratic, but U.K. imports are growing strongly and surpass export growth over each horizon. The Netherlands and Portugal each show strongly expanding exports. Finland's trade dependence with Russia is taking a severe toll as exports are lower on balance over six months and three months but still are higher year-over-year by 5.8%. Europe's trade flows are complex despite sharing the same currency (except the U.K. here).

On balance, the euro exchange rate is not acting as economic theorists thought by moving to equilibrate international accounts. Currency movements in Europe and in the U.S. are acting to worsen existing imbalances. Currency movements are being dictated instead by monetary policy and expected monetary policy moves. In Europe, that is also reinforced by the currency making up for macroeconomic deficiencies and providing stimulus to a region where fiscal policy is handcuffed. We have seen the same thing in Japan. In the U.S., expectations that the Fed will hike rates drive the dollar higher but that worsens the U.S. current account gap that has been in deficit for some 24 years in a row. Moreover, the U.S. does not exactly have growth to burn and the rising dollar is undermining the U.S. attempt at acceleration.

All of this points up how currency dynamics have become so different than expected. Macroeconomic forces, not external developments, govern currency rates. Since the U.S. is the center country in this system, rate moves always occur on the needs of its trade partners. The dollar rarely moves in a way to provide the U.S. economy what it needs. The EMU exchange rate is moving fast below parity marking a too-low euro. The rising trade surplus in the EMU is being exacerbated by extremely weak domestic demand. Even though European exports are hampered by weak global growth and stifled trade with Russia, exports perform so much better than imports, especially as oil prices collapse, European trade is setting new records for its surplus and getting the stimulus it refuses to provide internally. While that may work for Europe, it pushes growth-reducing deficits on the rest of the world, a so-called beggar-thy-neighbor policy. Europe's inability to make good policy is hurting the global economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief